The TSP match under the Blended Retirement System is the single highest guaranteed return available to any service member. Contribute 5% of your basic pay, and the government puts in 5%. That is a 100% return on your first 3% and a 50% return on the next 2%. No market investment, no savings account, no side hustle can guarantee that.

Most service members know TSP matching military benefits exist. Fewer know the exact formula, what counts as eligible pay, or what it costs them every month they contribute below 5%.

This is the full breakdown.

How TSP Matching Works Under BRS

Two pieces. The automatic contribution and the match. They work differently.

The automatic 1%. The Department of Defense contributes 1% of your basic pay to your TSP whether you contribute anything or not. If you never log into myPay, never set a contribution percentage, never think about TSP at all, that 1% still goes in. It started on day one of your service.

The match. This is the part that requires your participation. When you contribute your own money, the government matches it. Two tiers:

- Your first 3%: matched dollar-for-dollar (100% match)

- Your next 2% (from 3% to 5%): matched fifty cents on the dollar (50% match)

At 5% member contribution, the government puts in a total of 5%: the automatic 1%, plus 3% from the full match on your first 3%, plus 1% from the partial match on your next 2%.

You put in 5%. The government puts in 5%. Your TSP receives 10% of your basic pay every pay period.

Below 5%, you are leaving part of that match unclaimed. It does not roll over. It does not accumulate. It is gone.

The Match Formula in Detail

The table below shows exactly what happens at each contribution level.

| Your Contribution | Automatic (1%) | Match | Total Government | Total to TSP |

|---|---|---|---|---|

| 0% | 1% | 0% | 1% | 1% |

| 1% | 1% | 1% | 2% | 3% |

| 2% | 1% | 2% | 3% | 5% |

| 3% | 1% | 3% | 4% | 7% |

| 4% | 1% | 3.5% | 4.5% | 8.5% |

| 5% | 1% | 4% | 5% | 10% |

| 6%+ | 1% | 4% | 5% | 11%+ |

The match caps at 5% member contribution. Contributing 6%, 10%, or 15% does not increase the government’s contribution beyond 5%. Those additional contributions still go into your TSP and still compound, but the match is fully captured at 5%.

The column that matters: Total to TSP. At 5%, your TSP receives 10% of basic pay per pay period. At 3%, it receives 7%. The difference between contributing 3% and 5% is not 2%. It is 3% when you include the match you are missing.

What Counts as Basic Pay

TSP matching is calculated on basic pay only. This is a common point of confusion because basic pay is not the same as total military compensation.

Included in the match calculation:

- Basic pay (the number on your LES under “Base Pay”)

Not included in the match calculation:

- BAH (Basic Allowance for Housing)

- BAS (Basic Allowance for Subsistence)

- Special pay (flight pay, hazardous duty pay, etc.)

- Incentive pay

- Bonuses

When you set your TSP contribution percentage in myPay, that percentage applies to your basic pay. An E-4 with 4 years of service has a basic pay of approximately $3,659 per month (2026 pay tables). At 5%, that is roughly $183 per month from the member and $183 per month from the government. Not from total pay. From basic pay.

Some service members see their total LES deposit and assume 5% of that is going to TSP. It is not. The percentage is applied to basic pay only. If you want to contribute more total dollars, you increase the percentage beyond 5%. The match is captured at 5%, but additional contributions still build your balance.

Special and incentive pay can be elected for TSP contributions, but this requires a separate election. It is not automatic. Check your myPay settings if you receive special pay and want it included.

The Vesting Schedule

Not all government contributions are yours immediately.

Your own contributions: Always 100% yours. From day one. If you separate after six months, every dollar you contributed comes with you.

Matching contributions: Also immediately vested. The match the government puts in based on your contributions is yours from the first deposit.

The automatic 1%: This one has a vesting schedule. You must complete two years of service for the automatic contributions to vest. If you separate before two years, the automatic 1% contributions are forfeited. Your own contributions and the match stay.

After two years, everything is fully vested. The automatic 1%, the match, and your own contributions are all yours regardless of when you separate.

For most service members, this is a non-issue. The initial enlistment is four to six years. By the time you are making TSP decisions, the vesting period has passed. But if you are considering a short enlistment or an early separation, know that the automatic 1% is the only piece at risk, and only within the first two years.

Roth vs. Traditional: Where Does the Match Go?

Your contributions can go to Roth TSP, Traditional TSP, or a split of both. That is your choice in myPay.

The government match always goes to Traditional TSP. Always. Regardless of your election.

If you contribute 100% Roth, your 5% goes into the Roth balance and the government’s 5% goes into the Traditional balance. You will have both a Roth and a Traditional TSP balance even if you never elected Traditional contributions. This is by law, not a setting you can change.

Why does this matter? Two reasons.

First, your TSP balance is not all one type. When you look at your total TSP balance, part of it is Roth (tax-free at withdrawal) and part of it is Traditional (taxed at withdrawal). The split depends on how long you have been contributing Roth and how much the match has accumulated on the Traditional side.

Second, if you are making Roth vs. Traditional decisions for your own contributions, the match being Traditional is additional context. Your overall TSP tax exposure is a blend, not purely one or the other.

The full Roth vs. Traditional decision framework is a bigger topic than matching mechanics. What matters here: know that the match goes Traditional and factor that into your understanding of your TSP balance.

The Dollar Cost of Not Contributing Enough

The match is math. So is the cost of missing it.

An E-4 at 4 years, basic pay approximately $3,659/month.

At 5% contribution: $183/month from the member. $183/month from the government (automatic + match). Total to TSP: $366/month.

At 3% contribution: $110/month from the member. $146/month from the government (automatic + partial match). Total to TSP: $256/month.

At 0% contribution: $0 from the member. $37/month from the government (automatic 1% only). Total to TSP: $37/month.

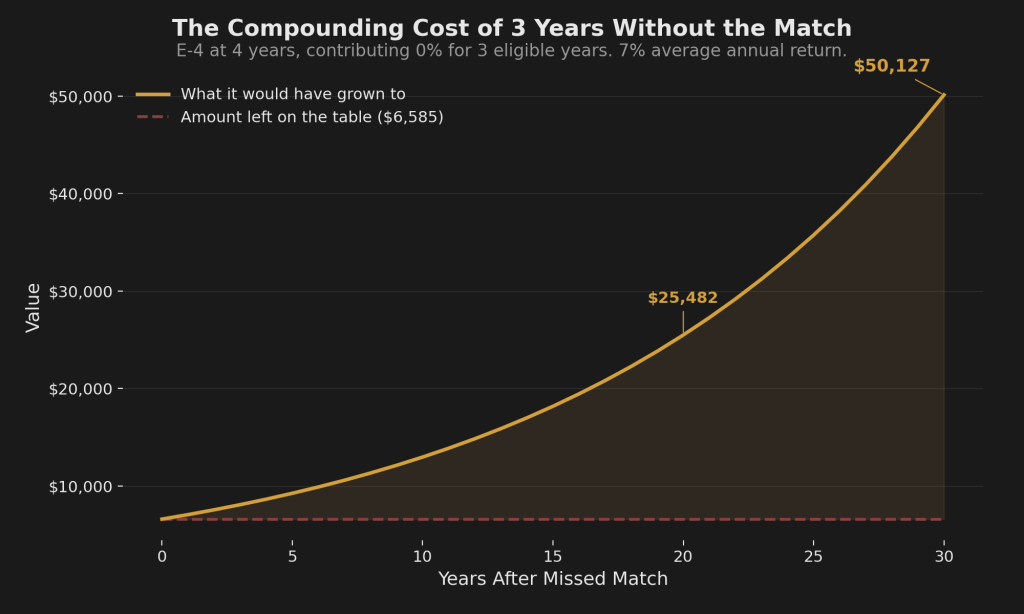

The difference between 5% and 0% is $329 per month going into TSP. Over three years of missed matching (which begins at year three of service for the match, year one for the automatic), a service member contributing 0% leaves approximately $6,585 in match money on the table. Before compounding.

Run that $6,585 forward at an average annual return of 7% for 20 years. It grows to approximately $25,500. For 30 years: approximately $50,100. That is the compounding cost of three years of inaction. Not three years of bad decisions. Three years of not logging into myPay and setting a number.

The gap between 3% and 5% is smaller but it compounds the same way. At 3%, you capture most of the match but leave roughly $37/month unclaimed. Over a 20-year career, that unclaimed $37/month, compounded at 7%, grows to approximately $19,000.

These are not scare tactics. They are the math of what the match produces when it has time to compound, and what it costs when it does not.

What Happens at Separation

When you leave the military, your TSP account does not close. The balance stays. The investments continue to grow or decline based on your fund allocation. The government stops contributing, but the money already in the account is yours (assuming vesting requirements are met).

You have three options:

Leave it in TSP. The account stays open. You can continue to manage your allocation. TSP has some of the lowest expense ratios available anywhere. Many veterans keep their TSP balance in place for exactly this reason.

Roll it to an IRA. Transfer the balance to an IRA at any brokerage. This gives you broader investment options beyond the TSP fund lineup. If you have both Roth and Traditional TSP balances (and you will if you contributed Roth while receiving the match), these are separate rollover transactions. The Roth balance goes to a Roth IRA. The Traditional balance goes to a Traditional IRA. Work with your receiving institution to make sure both are handled correctly.

Roll it to a new employer’s 401(k). If your civilian employer offers a 401(k), you can transfer your TSP balance there. This consolidates your retirement accounts under one plan.

You do not have to decide immediately. There is no deadline to move TSP funds after separation. Take the time to understand your options.

The match does not disappear at separation. Every dollar the government contributed (past the vesting period) stays in your account and continues to compound. A service member who contributed 5% for 20 years and then separates still has every match dollar working for them.

The Match Is Step One

Capturing the full TSP match is the single highest-return action on the entire Azimuth Roadmap. No other financial move you make as a service member produces a guaranteed 100% return.

And it is not enough.

Under BRS, the military pension dropped from 50% of base pay to 40%. The TSP match was part of the trade. The government gave you the match to offset part of that pension gap. At 5% member contribution with 5% government contribution, 10% of basic pay flows into TSP per pay period. For most military families, 10% of basic pay does not close the gap between a 40% pension and a financially independent retirement.

The match handles the guaranteed money. The BRS pension gap is the structural problem above it. What that gap costs in real dollars by rank over a 30-year retirement is where the bigger picture starts.

The match is where you start. It is not where the math ends.

Get the Full Framework

The Firewatch Blueprint shows the full BRS pension gap by rank, what 10% to TSP actually produces over a career, and how your allocation pattern affects what that match becomes over time. The match gets the money in. The pattern determines what it becomes.

About the Author

Joshua Breaux

Retired U.S. Marine

Financial Management Analyst

BS & MBA in Analytics

His family runs on the same systems he teaches here.

This content is educational and does not constitute personalized financial advice. Millionaire Veteran is not affiliated with the Thrift Savings Plan, FRTIB, or the U.S. Government. Past performance does not guarantee future results.