The Blended Retirement System reduced the military pension from 50% to 40% of High-3 base pay at 20 years of service. For a senior NCO, the gap is roughly $660 per month for life. For a lieutenant colonel, it’s $1,150 per month.

The government added TSP matching to offset the reduction. Whether it actually does depends entirely on what you do with your TSP.

This article covers the dollar cost of the Blended Retirement System by rank, what the matching is actually worth, and the shift that most service members under BRS have never been told about directly: your Thrift Savings Plan is no longer a supplemental retirement account. It’s a structural one.

What the Blended Retirement System Actually Changed

BRS took effect January 1, 2018. Every service member entering after that date is automatically enrolled. Service members already serving had a one-time opt-in window. The system is now the default for the majority of the force.

Here is what changed.

Under the legacy High-3 system, a service member who completed 20 years earned a pension equal to 50% of the average of their highest 36 months of base pay. The multiplier was 2.5% per year. Each additional year added 2.5% more.

Under BRS, the multiplier dropped to 2.0% per year. At 20 years, that means 40% of High-3 instead of 50%.

The difference is 10 percentage points of your base pay. Every month. For the rest of your life.

When I came in, the pension was the plan. TSP was an afterthought, and plenty of Marines never touched it. You could build a full career without thinking about investment returns because half your base pay showed up every month the day after you retired. The government carried the retirement risk. You carried the mission.

BRS shifted a meaningful portion of that risk to you. The pension is still there. It’s smaller. And the gap between the old system and the new one compounds into real money over a retirement that can easily span 35 years or more.

The enrollment briefing covered how to sign up. It did not cover what the change costs.

What BRS changed:

- Pension multiplier: 2.5% per year (legacy) to 2.0% per year (BRS)

- At 20 years: 50% of High-3 (legacy) to 40% of High-3 (BRS)

- Gap: 10% of your High-3 base pay, every month, for life

- TSP matching added to partially offset the reduction

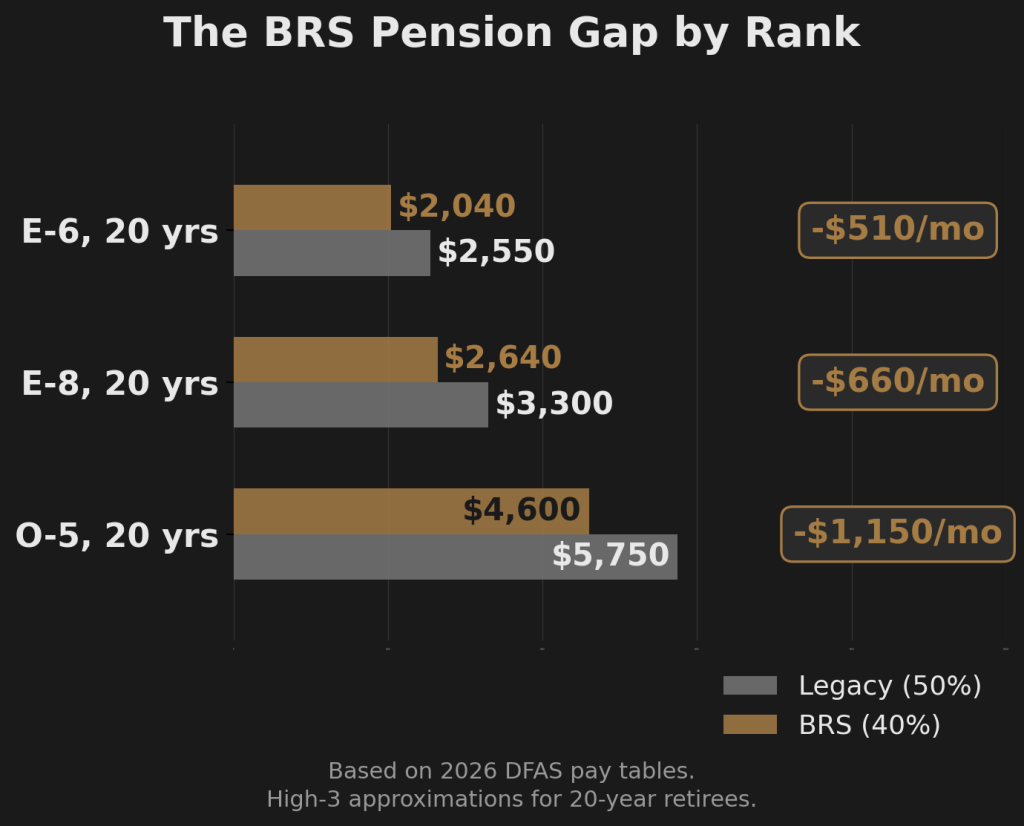

The Dollar Cost

The Blended Retirement System pension gap is straightforward arithmetic. It equals 10% of your High-3 average base pay, paid monthly, for the duration of your retirement.

An E-8 retiring at 20 years in 2026 has a High-3 average base pay of approximately $6,600 per month. Under the legacy system, their pension would be $3,300 per month. Under BRS, it’s $2,640. The gap: $660 every month. That’s $7,920 per year. Over a 35-year retirement, roughly $277,000 that the old system would have guaranteed.

An O-5 at 20 years, with a High-3 average of approximately $11,500 per month, faces a pension gap of $1,150 per month. That’s $13,800 per year and approximately $483,000 over 35 years.

Both lose six figures over the course of a normal retirement. And these numbers don’t include COLA adjustments, which compound the gap further every year.

| Rank | Approx. High-3 | Legacy (50%) | BRS (40%) | Monthly Gap | Annual Gap | 35-Year Total |

|---|---|---|---|---|---|---|

| E-6, 20 yrs | $5,100 | $2,550 | $2,040 | $510 | $6,120 | $214,000 |

| E-8, 20 yrs | $6,600 | $3,300 | $2,640 | $660 | $7,920 | $277,000 |

| O-5, 20 yrs | $11,500 | $5,750 | $4,600 | $1,150 | $13,800 | $483,000 |

Based on 2026 base pay tables (DFAS). High-3 figures are approximations using the last 36 months of base pay at representative time-in-service points. 35-year retirement reflects a 20-year retiree reaching average life expectancy per SSA actuarial data. Actual amounts vary by promotion timing, time in service, and annual pay adjustments. COLA increases the absolute dollar gap over time.

The formula works for every rank. Multiply your High-3 average base pay by 10%. That’s your monthly pension gap under BRS.

This is not a complaint about the Blended Retirement System. It is the system. The math is the math. What was missing, for most service members, was anyone explaining what these numbers actually mean for their retirement.

What the Government Gave You Instead

BRS did not simply cut the pension and walk away. It introduced TSP matching.

Under BRS, the Department of Defense contributes to your Thrift Savings Plan in two ways.

Automatic 1% contribution. DoD deposits 1% of your base pay into your TSP regardless of whether you contribute anything. No action required on your part.

Matching up to 4%. When you contribute to your TSP, the government matches up to 4% of your base pay. Dollar for dollar on the first 3% of your contribution, then 50 cents on the dollar for the next 2%.

At full match, the government puts 5% of your base pay into your TSP every pay period.

For an E-5 earning about $4,100 per month, that’s roughly $205 per month in government contributions. Over a 20-year career with investment growth, that matching alone can add up to $100,000 or more, depending on returns.

One detail that almost nobody explains clearly: matching contributions always go into your Traditional TSP balance, even if every dollar of your personal contributions goes to Roth. Every BRS service member making Roth contributions has a split account whether they intended one or not. That wrinkle matters when it comes time to think about account structure.

The trade BRS made is direct. Less guaranteed pension. More investment responsibility. The matching gives you the raw material. What you do with it determines whether the pension gap closes or stays open.

BRS matching breakdown:

- 1% automatic DoD contribution (no action required)

- Dollar-for-dollar match on the first 3% you contribute

- 50 cents on the dollar for the next 2% you contribute

- Maximum government contribution: 5% of your base pay

- All matching deposits go to your Traditional balance, even on Roth contributions

You’re an Investor Now

Under the legacy system, your TSP was supplemental. A service member who never logged into their TSP account once still retired with 50% of base pay and a stable financial floor. The pension did the heavy lifting.

Under BRS, your TSP is structural. It carries the weight that the reduced pension no longer does.

That pension gap from the table above? Your TSP investment returns are what fills it, or what leaves it open.

This is the shift that most BRS briefings skipped entirely. The enrollment session covered which funds exist, how to log in, and how to set a contribution percentage. It did not cover what happens when the market drops 40% and your account balance falls by six figures. It did not address the difference between being in a particular allocation and understanding why you’re there.

I’ve watched E-3s set this up in their first year and get it right from the start. I’ve watched E-7s realize at year 16 that they never changed the default allocation from the day they enrolled. Both are under BRS. Both carry the same pension gap. One has 16 years of compounding working for them. The other has 16 years of compounding working against them.

If you’re in your first term, this is the part that matters most: every year your TSP sits in the wrong place, compounding works in the wrong direction. You can’t get that time back. But you also have more of it than anyone else in the formation. Time is the single most valuable asset in investing, and you have more of it right now than you ever will again.

If you’ve been in for a decade and haven’t looked at this closely, the math is still on your side. You have fewer years of compounding ahead, but enough to close a meaningful portion of the gap if you use them with intention.

The pension gap is real. Your TSP is the only tool that fills it. And right now, that tool is sitting in your account doing whatever your current allocation tells it to do.

Are You Doing It Right?

If your TSP carries the responsibility that the pension no longer does, there is a question most service members under BRS have never been asked directly.

Are you doing it right?

The question is not whether you enrolled or whether you contribute enough to capture the match. Those are entry-level moves. The real question is whether your current TSP allocation was chosen based on your actual timeline, your actual risk tolerance, and an honest assessment of how you’d respond if your balance dropped by a third.

Behavioral finance researchers have studied how people respond to exactly this kind of shift for decades. When retirement responsibility transfers from an institution to an individual, people don’t respond randomly. They fall into documented patterns.

Four of them show up in military TSP accounts constantly.

Status quo bias. The default allocation feels safe because it’s the default. Not because you assessed your options and chose it. Because it was already selected when you logged in. Samuelson and Zeckhauser’s research (1988) showed this is one of the most persistent biases in decision-making: when an option is pre-selected, people keep it at dramatically higher rates than they would ever choose it fresh.

Overconfidence. Going all-in on a growth allocation based on something you read online or heard from a buddy, without calculating what a 55% drawdown actually looks like on your balance. Barber and Odean’s research (2000) showed that overconfident investors consistently trade more and earn less. The confidence isn’t the problem. The gap between confidence and understanding is.

Automation bias. Selecting a lifecycle fund or a set-and-forget split because it feels like a system is handling it. It is a system. But it’s a system that rebalances within a drawdown, not one that steps aside during one. That distinction matters, and most people never examine it.

Loss aversion. The instinct to move to capital preservation after a drop, then chase the growth allocation on the way back up. Kahneman and Tversky’s prospect theory (1979) showed that losses feel significantly more painful than equivalent gains feel good. That asymmetry drives most reactive TSP decisions: sell after the pain, buy after the relief, arrive one step behind the market in both directions.

Most service members under BRS fall into one of these patterns. Not because they chose poorly. Because nobody asked them to choose at all. They fell into it.

Your pattern determines how you respond when the market drops, when your balance shrinks, when the headlines get loud. It determines whether you hold or sell, whether you wait or chase, whether your TSP closes the pension gap or widens it.

Which one are you?

The four TSP allocation patterns, what each one costs, and the gap they all share.

Get the Full blueprint

The Firewatch Blueprint walks through the pension gap math, all four default patterns, and the full three-strategy framework. Everything in this article, plus the complete picture.

About the Author

Joshua Breaux

Retired U.S. Marine

Financial Management Analyst

BS & MBA in Analytics

His family runs on the same systems he teaches here.

This content is educational and does not constitute personalized financial advice. Millionaire Veteran is not affiliated with the Thrift Savings Plan, FRTIB, or the U.S. Government. Past performance does not guarantee future results.