Money arrives. Money leaves. The gap between those two events is invisible.

Nobody blew the paycheck on a single bad purchase. The truck payment, the Starbucks habit, the Amazon orders. Those are easy to point at. The real drain is the hundred things that feel small individually and devastating collectively. Groceries, gas, school lunch money, a birthday present, new socks because the old ones have holes. None of it feels like overspending. All of it adds up to a checking account that hits zero before the next deposit.

This is the most common financial experience in the military. It does not discriminate by rank, branch, or family size. It happens to the service member three months into their first enlistment and the one fifteen years in with three kids and a mortgage. The paycheck amounts are different. The confusion is the same.

The Disappearing Paycheck

The deposit hits. The number looks right. Within a week, a third of it is gone and you cannot reconstruct where.

For someone early in their career, it might be $1,800 that evaporated before the 15th on nothing memorable. No concert tickets. No expensive dinner. Just gas, food, a phone case, a haircut, lunch off base three times, and a subscription that auto-renewed. Each one felt like nothing. Together they consumed half the paycheck.

For a family running a full household, it might be $5,200 that vanished into groceries, school fees, gas for two cars, diapers, a broken washing machine repair, and sports registration for the oldest. None of it optional. None of it excessive. All of it invisible until the balance dropped.

Both versions end the same way. Someone looks at the checking account, sees a number lower than expected, and asks the same question: where did it go?

The answer is almost never one thing. It is the accumulation of obligations that have no single line item large enough to notice but a combined weight that drains the account. The problem is not any individual purchase. The problem is that nothing in the system shows you the accumulation in real time.

Why One Account Lies to You

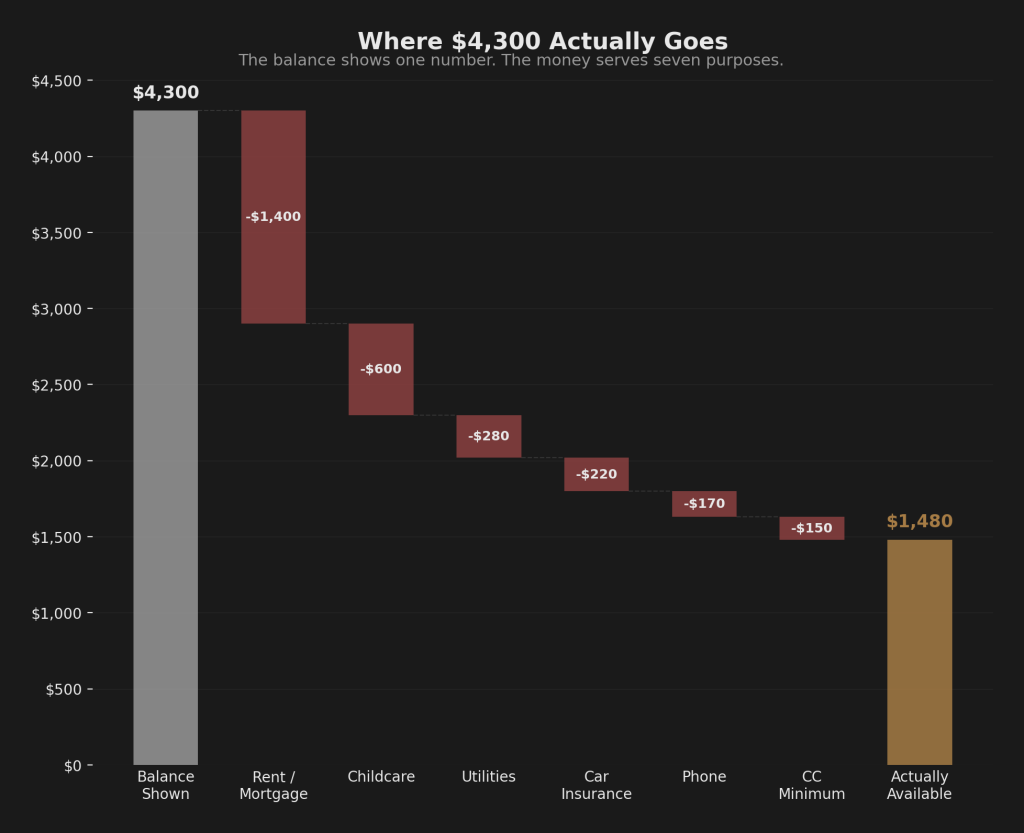

Open your banking app. Look at the checking account balance. Say it is $4,300.

What does that number actually mean?

Rent or mortgage payment drafts in three days: $1,400. Car insurance autopays next week: $220. Phone bill on the 22nd: $170. Childcare is due Friday: $600. Utilities run about $280. The credit card minimum autopays on the 28th: $150.

After subtracting what is already committed, the real available number is around $1,480. For everything else. Groceries, gas, household supplies, the unexpected, and whatever passes for breathing room.

But the app shows $4,300. That number includes money that already has a destination. It belongs to the landlord, the insurance company, the childcare provider, the power company. It has not left the account yet, but it is spoken for. The balance shows one number for money that serves twelve purposes.

This is where unplanned spending takes hold. The $200 pair of boots looks affordable against $4,300. Against $1,480 it becomes a different decision. Against the $900 that is actually discretionary after groceries and gas, it becomes a very different decision. But none of those numbers are visible in a single checking account. You would have to calculate them, every time, from memory.

Every unplanned purchase gets weighed against the wrong number. And every partner in a relationship sees a different version of that wrong number.

The Couple’s Version

One partner looks at the balance. The other keeps a mental list of what is due.

“We have $4,300 in the account.”

“No, we have $1,480 after everything that drafts this month.”

Both are right about different numbers. Neither can prove it without sitting down and running the subtraction together. That conversation usually happens after a purchase one partner thought was fine and the other knew was tight. It ends with one person saying “I will just handle the money myself.” Which means one partner absorbs the cognitive load and the other disengages. Neither outcome is a system.

When two incomes flow into the household, the problem scales. Two deposits, two sets of allowances, sometimes two different pay schedules. More money coming in does not mean more clarity. It means more sources feeding into the same pile with more invisible commitments. The balance is larger. The gap between what it shows and what is actually available is proportionally larger.

The core issue is not communication. Plenty of couples who communicate well about money still have this problem. One checking account cannot show two people what is available for each purpose at a glance. The information does not exist in a format that prevents the argument.

The Household Reality

Running a military household is a financial operation. Income flows in and the complexity of the household consumes it.

Groceries for a family of four run $800 to $1,200 per month depending on where you are stationed. Childcare in some areas costs more than rent. Three kids means school supplies in August, sports registration in September, winter coats in November, and unexpected expenses that arrive on their own schedule. Each expense is reasonable. The total never stops.

BAH covers housing. BAS covers food for the service member. Neither is designed to scale with family size. The allowances are flat. The actual cost of feeding and sheltering a family is not.

A PCS every two to three years resets the financial picture entirely. New BAH rate. New rental deposit. New childcare provider with a different payment schedule. Temporary lodging expenses. The moving allowance covers some of it, not all of it, and the reimbursement timeline does not match when the bills hit. Every move requires recalibrating the numbers.

During deployments, the spouse managing the household carries the full financial and cognitive load. Every bill, every decision, every unexpected expense. A system that requires constant manual attention does not survive this. A system that runs on structure does.

The Credit Card Layer

Everything above is bad enough on its own. The checking account lies, the obligations are invisible, and the gap between paydays feels impossible to bridge.

For some families, credit cards are filling that gap. When the checking account runs low before the 15th, a credit card covers groceries for the last three days. When an unexpected expense hits mid-month, a card absorbs it because the checking balance cannot. When the holidays arrive and there is no money set aside, a card makes Christmas happen.

None of this is reckless. It is a rational response to a visibility problem. If you cannot see what is actually available, you cannot plan for the gap. The credit card becomes the bridge between what the checking account shows and what the checking account can actually cover.

But credit cards compound the problem they solve. The $400 in groceries that went on the card last month is now a minimum payment this month. That minimum payment is one more invisible obligation sitting inside the checking account balance, making the real available number even smaller, making the next gap wider, making the next credit card charge more likely.

If credit cards are part of the picture, every problem described in this article has an additional layer of pressure underneath it. If they are not, the visibility problem alone is enough to warrant a different approach. Either way, the solution starts in the same place: structure.

What Most People Try

Apps, spreadsheets, mental math, or nothing. Some military families have cycled through all four. Some have never tried any of them.

Apps and spreadsheets require sustained tracking. Log every transaction, categorize it, review at the end of the month. That works until a field exercise eats a week, a TDY disrupts the routine, or a PCS makes every number in the spreadsheet wrong. The tool does not survive the interruption, and military life is one interruption after another.

Mental math requires no tool but produces no accuracy. A running estimate in your head works for about ten days per pay period. By the second week, three or four unplanned expenses have landed and the estimate is off by hundreds. You do not know this until the balance drops below where it should be.

Nothing is more common than most people admit. Do not look at the numbers. Do not check the balance. As long as nothing bounces, assume it is fine. This is especially common when both partners assume the other one is watching.

All four responses share the same flaw: none of them create real-time visibility into what is available by purpose. Part 2 breaks down these patterns in detail and what each one reveals about the structure that is missing.

The Real Problem

Money needs to be separated by purpose before it is spent. When each purpose has its own account, the balance IS the answer. The groceries account has $340. That is what is available for groceries. No app interpreting your transactions after the fact. No mental math. Just a number that is current because the bank updates it, not because you remembered to log something.

Your grandparents knew this. Cash envelopes worked for exactly this reason. Money went into physical envelopes labeled “rent,” “groceries,” “gas.” When the envelope was empty, that category was done. Nobody tracked transactions. The physical separation was the system.

The digital version applies the same principle with separate checking accounts and debit cards. Money arrives, gets distributed by purpose, and each balance tells you what is available in real time. It scales from one person to a household of six.

The setup takes real effort. Building the account structure, deciding the allocations, learning the routing. And the system is not passive once it is running. Allocations need tweaking as reality reveals where the estimates were off. A monthly check keeps everything calibrated. But the trade is worth every hour. The question changes from “can I afford this?” which requires calculation, memory, and judgment, to “does this account have the money?” which requires checking a balance. That second question works when you are tired, busy, stressed, or just do not want to think about money today.

The low-grade financial stress that sits in the background of every purchase, every conversation, every paycheck that felt like it was not enough. That goes quiet. The income did not change. The visibility did. No more wondering what is committed. No more arguments about what the balance really means. No more guilt about spending money that was actually available to spend.

That is the trade. Real effort up front, ongoing calibration, and in return something most military families have never experienced: knowing exactly where they stand without doing math.

The Question That Changes Everything

Most people who arrive at this article are looking for an answer to “where does my money go.” That is the right question to ask. It is the wrong question to keep asking.

The better question: can you tell what is available for groceries this week by looking at one account balance? One number, in one account, that tells the truth because the money was separated by purpose before you spent it.

If the answer is no, the problem is that money is sitting in one pile with no structure to show what each dollar is for.

The question is not where your money went. It is which pattern you have fallen into, and what that pattern reveals about the structure you are missing.

Next in the Series

This is Part 1 of the Spend Less series. Part 2: The Four Cash Flow Personalities shows you the four patterns military families fall into and why all four are responses to the same structural problem.

Join the Community

Millionaire Veteran is a free community where military families learn the Azimuth Framework: Spend Less, Earn More, Invest Smarter. In that order. The Compass Method is the cash flow system inside the Spend Less domain. The full implementation, built on your real numbers with a personal AI advisor, lives inside the community.

Structure replaces guesswork.

About the Author

Joshua Breaux

Retired U.S. Marine

Financial Management Analyst

BS & MBA in Analytics

His family runs on the same systems he teaches here.

This content is educational and does not constitute personalized financial advice. Millionaire Veteran is not affiliated with the Thrift Savings Plan, FRTIB, or the U.S. Government. Past performance does not guarantee future results.