Part 1 showed the problem: money disappears into a single checking account and nobody can see what is actually available for each purpose. This article is about what people do in response to that problem.

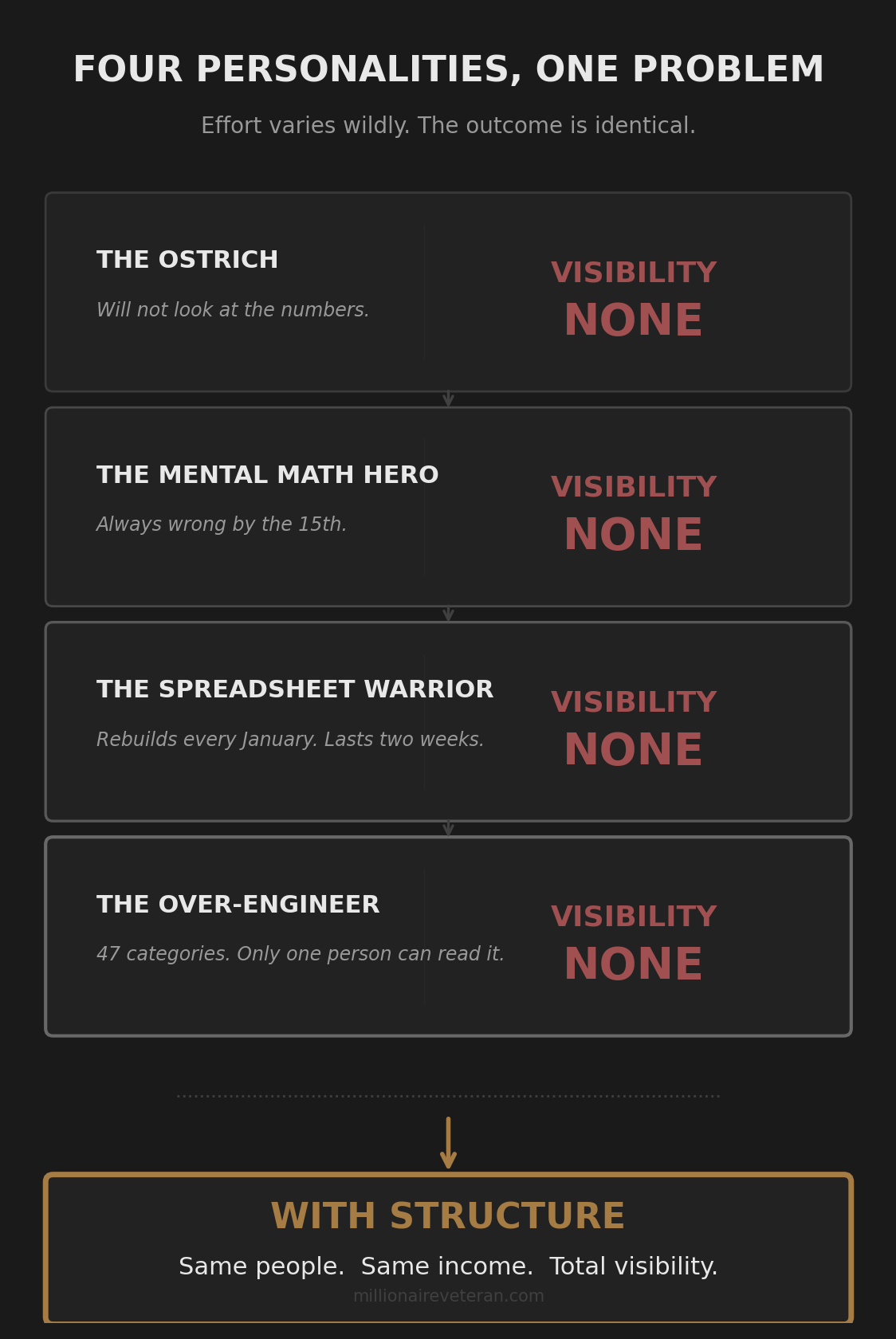

If you are trying to stop living paycheck to paycheck, the first step is not a budget. It is recognizing which pattern you are stuck in. Every military family handles money differently. But when you strip away the specifics, the approaches collapse into four patterns. Four ways of coping with the same structural gap. You will recognize yourself in one of them. Some of you will recognize yourself in two or three, depending on the year or who in the household is managing the money.

The point is to see the pattern, understand why it exists, and recognize that all four lead to the same place.

The Ostrich

Does not look at the numbers. Will not look at the numbers. The banking app exists on the phone somewhere but opening it produces a physical reaction somewhere between dread and nausea.

The Ostrich has one checking account. Everything goes in, everything comes out, and the balance is whatever it is. Payday feels like relief. The week before payday feels like holding your breath. The cycle repeats every two weeks.

The Ostrich label sounds like laziness. It rarely is. Most Ostriches tried to engage with their finances at some point, found it overwhelming or painful, and learned that not looking hurts less than looking and not knowing what to do about what you see. The avoidance is a coping mechanism.

In households with two incomes, the Ostrich pattern frequently shows up as silent delegation. Both partners assume the other one is handling it. Neither confirms. The money comes in, the bills get paid on autopay, and as long as nothing bounces, nobody asks questions. This works until it stops working. When it stops, it stops all at once, and the conversation that follows is the worst financial conversation a couple can have: “I thought you were watching this.”

If credit cards are part of the Ostrich pattern, they serve as the invisible safety net. The card covers the gap the Ostrich does not want to see. The minimum payment autopays from the checking account, further obscuring the real number, and the balance grows without anyone acknowledging it. The Ostrich knows, somewhere, that the card balance is climbing. Looking at it is the thing they cannot do.

One balance per purpose. No interpretation required. That is the only thing that gets the Ostrich to open the app.

The Spreadsheet Warrior

Has tried everything. Every app, every template, every system that promised to make the money make sense. Downloaded YNAB, tried EveryDollar, built a Google Sheets template from a YouTube tutorial, switched to Mint before it shut down, tried Copilot, and currently has two half-finished spreadsheets saved to their desktop.

The Spreadsheet Warrior is genuinely motivated. They sit down on the 1st or the 15th, set up categories, enter income, allocate amounts, and feel in control for about two weeks. Then a TDY trip throws off the grocery numbers. A field exercise means eating at the DFAC for a week, which saves money but makes the spending categories meaningless. A PCS throws the entire spreadsheet away because every number changed.

The Warrior rebuilds. Every January, sometimes every quarter. New year, new spreadsheet, new commitment. The pattern repeats because the tool requires sustained manual attention, and military life does not allow for sustained manual attention to a financial spreadsheet.

The cruelest part is that the Warrior does more work than anyone else and gets the same result as the Ostrich. Different effort, same outcome. The spreadsheet shows what was planned. The checking account shows what actually happened. Those two numbers diverge by week two, and the gap between them is where the stress lives.

If credit cards are part of the Warrior’s pattern, they appear as a category that never reconciles. The card spending gets logged, but the balance carries month to month. The spreadsheet shows $200 allocated to credit card payment. The statement shows $3,800 owed. The spreadsheet is technically correct about the payment. It says nothing about the debt.

The discipline was never the problem. The tools were wasting it. A system that survives a PCS, a TDY, and a deployment without rebuilding from scratch is what the Warrior’s effort deserves.

The Mental Math Hero

No app. No spreadsheet. No system at all. Just a running estimate that feels roughly accurate most of the time.

“I think we have about $800 left until payday.”

The Mental Math Hero operates on approximation. They know roughly what the rent costs, roughly what they spent at the commissary last week. The numbers are close enough to feel like a system. They are never close enough to actually be one.

This works for about ten days per pay period. The first few days after payday, the balance is high enough that the estimate does not matter. The last few days before payday, the balance is low enough that the Hero switches to survival mode: no unnecessary spending, check the account before every purchase, hope nothing unexpected hits.

The middle is where the Hero loses. An unexpected car repair. A kid’s field trip fee. A vet bill. Each one is small enough to absorb individually, but the Hero’s mental ledger does not subtract fast enough. By the time three or four unplanned expenses have landed, the running estimate is off by $200 to $400. The Hero does not know this until the balance drops below where it should be and the math stops adding up.

The Hero pattern is the hardest one to recognize in yourself because it feels like it is working. You are paying attention to money. You are making calculations. You are being responsible. The fact that the calculations are wrong by the second week of every pay period does not register as a system failure. It registers as a bad week. Then another bad week. Then a pattern you cannot name.

For couples, the Hero creates a specific conflict. One partner runs the mental ledger. The other spends based on the checking account balance. Two people, two different numbers in their heads, no shared source of truth.

If credit cards fill the gap for the Hero, they show up at the end of the pay period when the mental math came up short. The card covers the last three days of groceries or the tank of gas that the estimate said was fine but the balance said was not. The charges are small enough to rationalize individually. Twenty here, forty there. But they accumulate across months into a balance that the Hero never planned for because the mental ledger never accounted for the pattern. The Hero swears it will not happen next month. It happens next month.

Better mental math is not the answer. The right number needs to be visible without any calculation at all.

The Over-Engineer

Forty-seven categories. Color-coded tabs. A spreadsheet so detailed it tracks individual subscription amounts by renewal date, with conditional formatting that turns cells red when a category exceeds its monthly allocation by more than 10%.

The Over-Engineer is often the partner in a household who took over the finances because someone had to, and they responded by building the most detailed tracking system they could design. Every dollar accounted for. Every category monitored. Every deviation flagged.

The problem is not that the system is wrong. The problem is that maintaining it consumes thirty to sixty minutes per week. Categorizing transactions, reconciling accounts, updating projections, investigating discrepancies. The Over-Engineer knows where every dollar went last month. They can produce a report. They cannot, in three seconds, tell you what is available for groceries this week without consulting the spreadsheet.

The Over-Engineer’s system is fragile because it depends entirely on one person. When that person deploys, gets sick, goes TDY, or burns out from maintaining a financial tracking system on top of a military career and a family, the system collapses. The other partner cannot operate it. The categories are intuitive only to the person who built them.

The Over-Engineer has also created an invisible power imbalance. One partner controls all financial information. The other partner has to ask permission to understand their own money. “Can we afford this?” The Over-Engineer never intended to create a power imbalance. But a system that requires expertise to interpret produces one whether anyone meant it to.

If credit cards exist in the Over-Engineer’s system, they are tracked meticulously but the debt persists. The spreadsheet knows exactly what was charged and when. The minimum payment is categorized. The interest is calculated. The balance remains. The Over-Engineer has full visibility into the debt and no mechanism to eliminate it faster because the system tracks what happened, it does not direct what happens next.

The Over-Engineer does not need more categories. They need fewer. A system where both partners can see every purpose-specific balance in seconds, without expertise, without asking the other person for a status report. The Over-Engineer’s discipline is real. The system should free it for something more productive than categorizing last month’s spending.

The Pattern Beneath All Four

The Ostrich avoids the problem. The Warrior tracks the problem. The Hero estimates the problem. The Over-Engineer over-manages the problem. Four approaches. Same result.

What all four share: no real-time visibility into what is actually available for each purpose.

The Ostrich lacks it because they will not look. The Warrior lacks it because the spreadsheet is always behind reality. The Hero lacks it because mental math cannot hold all the variables. The Over-Engineer lacks it because 47 categories on a spreadsheet still require interpretation to answer a simple question.

Discipline is not what is missing. The Warrior and the Over-Engineer have more financial discipline than most people. Engagement is not what is missing. The Hero pays attention constantly, just without a reliable tool. Even the Ostrich is not lacking awareness. They know there is a problem. They are avoiding the pain of seeing it without being able to fix it.

What is missing is structure. A system where money is separated by purpose before it is spent, and each balance tells the truth without tracking, without calculation, and without asking someone else to interpret a spreadsheet.

Your grandparents understood this. Cash went into envelopes labeled rent, groceries, gas. When the envelope was empty, that category was done. Nobody tracked transactions. The physical separation was the system. The digital version applies the same principle with separate accounts and debit cards. Money arrives, gets distributed by purpose, and each balance tells you what is available in real time.

When the groceries account has $340, the Ostrich can look without dread because there is nothing to interpret. The Warrior does not need to rebuild a spreadsheet because the balance is already current. The Hero does not need to estimate because the number is exact. The Over-Engineer does not need 47 categories because a handful of accounts replaced all of them.

The question is not which personality you are. The question is what a cash flow system actually does and why it works when budgets, apps, spreadsheets, and mental math do not.

What that structure looks like, how the mechanics work, and why it holds through a PCS, a deployment, and a household with two incomes is the next article.

Next in the Series

Now you know which pattern you are in. Part 3: What a Cash Flow System Actually Does explains the mechanics: how money gets distributed, why account balances replace tracking, and what changes when the structure is in place.

Join the Community

Millionaire Veteran is a free community where military families learn the Azimuth Framework: Spend Less, Earn More, Invest Smarter. In that order. The Compass Method is the cash flow system inside the Spend Less domain. The full implementation, built on your real numbers with a personal AI advisor, lives inside the community.

The pattern is not the problem. The missing structure is.

About the Author

Joshua Breaux

Retired U.S. Marine

Financial Management Analyst

BS & MBA in Analytics

His family runs on the same systems he teaches here.

This content is educational and does not constitute personalized financial advice. Millionaire Veteran is not affiliated with the Thrift Savings Plan, FRTIB, or the U.S. Government. Past performance does not guarantee future results.