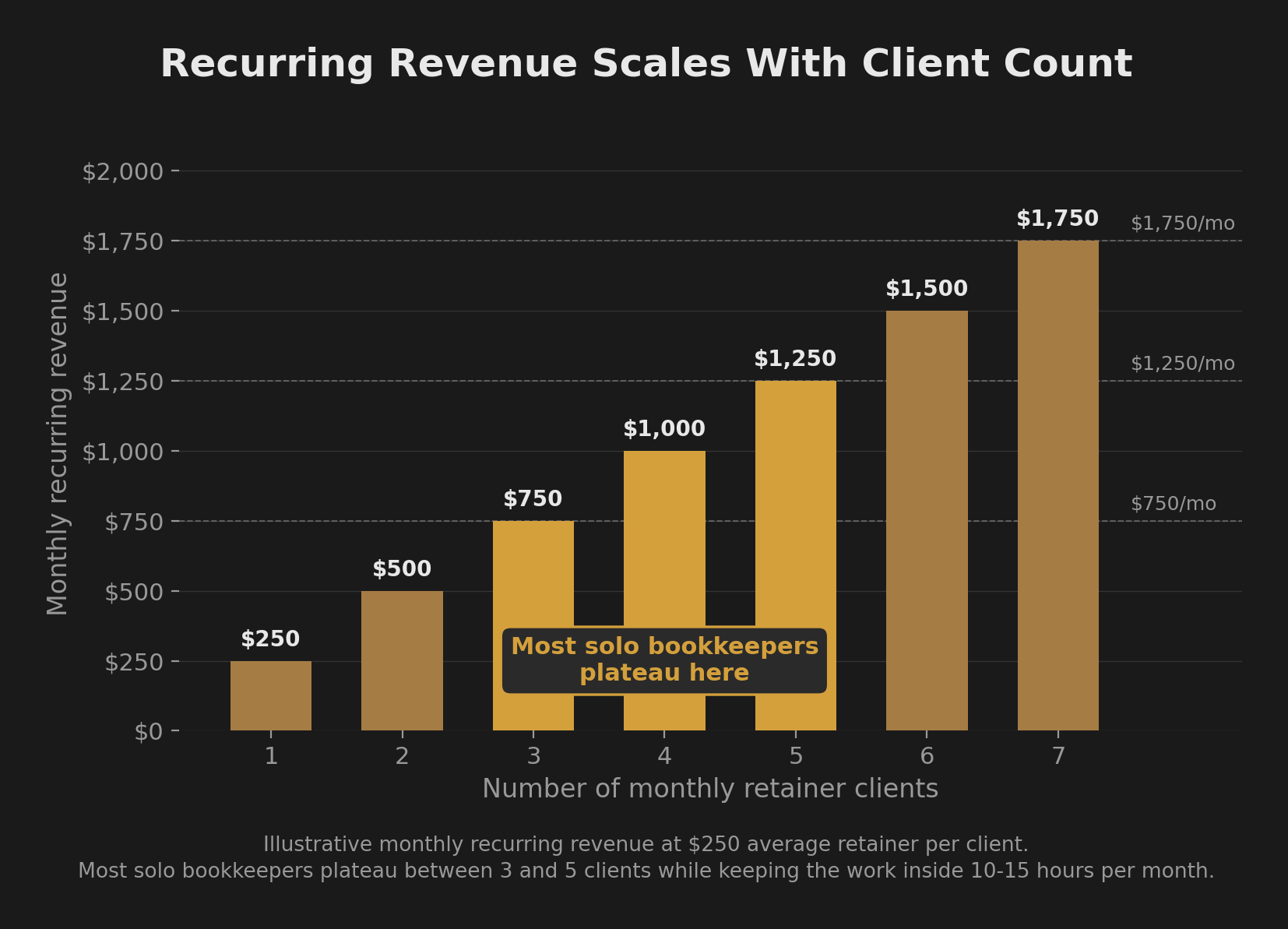

Three small-business clients at $250 a month each puts $750 a month into your household, recurring, every month, with the same clients paying again the next month. Five clients at the same rate is $1,250 a month. Seven is $1,750. The clients do not reset. The retainers do not disappear. The work compounds with the number of clients you serve, not with how many hours you put in.

That is what a bookkeeping side hustle actually looks like at the operational level. It is not a launch or a campaign. A short list of small businesses paying a monthly retainer because somebody has to keep their books clean and they do not want it to be them.

This article shows the real shape of that work and what it pays. The recurring revenue math up front. The actual monthly tasks, so you know what you are signing up for. The reason the work being unglamorous is what makes it hold. A realistic path from zero knowledge to a first paying client. The tiered progression that exists past the entry point, because the $250 basic retainer is the starting line, not the ceiling. And the broader framework that makes bookkeeping one of three doors into the same outcome rather than a single trick.

I run this exact function at BetterQuality Consulting, the bookkeeping and consulting practice I built and operate as a household income stream that funds the rest of my work. The numbers and the rhythm below come from running it, not from a course I bought.

The Recurring Revenue Math

A typical small business pays $250 to $500 a month for basic monthly bookkeeping. That covers categorizing transactions, reconciling accounts, and producing a profit and loss statement plus a balance sheet at month-end. The retainer grows with the depth of service. Businesses that need payroll oversight, more detailed reporting, sales-tax filings, or light financial analysis typically pay $500 to $1,000 or more a month for the same bookkeeper and the same client relationship with more layered work in the scope. The progression past the basic retainer is covered in a dedicated section below.

The keyword in that paragraph is the same word that defines the whole model: monthly. The same client pays again next month. And the month after. And the month after that. Three clients at a $250 average is $750 a month of monthly recurring revenue (MRR) the first month, $1,500 across two months, $9,000 across the year. Five clients is $15,000 a year on the same average. Seven is $21,000 a year.

Compare the structure to a gig income of the same hourly. A $750 income gap closed by DoorDash delivery requires roughly thirty deliveries a month, every month, in perpetuity, because the second the deliveries stop the income stops. Three bookkeeping clients at the same revenue level requires somewhere around fifteen to twenty hours of work per month total, because the work per client is small once the chart of accounts and the bank feeds are set up. The hourly rate is comparable. The structure is not. One income stops the day you stop showing up. The other keeps depositing while you sleep, provided the work was done correctly when you did show up.

The math gem to sit with is this. Client revenue scales with client count, not with hours worked. Each new client adds a fixed amount of monthly recurring revenue and a small fixed amount of monthly work. The income curve is steeper than the hours curve.

What the Work Actually Is

At the basic tier, five tasks, repeated monthly, per client.

Categorize transactions. The client’s bank feed pulls into QuickBooks Online automatically. You assign each transaction to the appropriate chart-of-accounts category. Most are repeat patterns that the software learns over time, so the volume drops as the months pass. New vendors and one-off charges get categorized by hand.

Reconcile the bank accounts. At month-end, match the bank statement to the QuickBooks balance. Track down any discrepancies. Usually there are none. Sometimes there is a missing transaction or a duplicate entry. You fix it.

Produce monthly financials. Run the profit and loss statement and the balance sheet. Sometimes a cash flow statement. Save them to the client’s shared folder. Send a short note pointing out anything worth their attention.

Answer questions, both directions. Questions flow your way and the client’s way. You email the client to clarify charges you cannot categorize on your own: “Was this $480 vendor payment for inventory or office supplies?” The client emails you with the strategic version: “Can I afford this hire from the cash flow we are running?” or “I need a P&L for a bank loan application, can you pull one?” Data questions flow your direction. Decision questions flow theirs.

Close the month. Lock the books for that period so nobody (including the client) accidentally edits historical numbers. Set up next month.

That is the basic tier. No tax preparation, no CPA work, no formal financial advice, no business consulting. If the client needs taxes done, you refer them to a CPA. If they need formal financial planning, that is a different professional. Your function at this level is bookkeeping: records accurate, categories clean, financials produced on schedule. As the relationship deepens and your skills layer up, expanded services and light advisory often get added on top. That is what the tier section below walks through. At the entry level, the five tasks above are the entire job. Year-end is the busy stretch because of CPA hand-offs and 1099 prep, but the rest of the year is steady. The work is methodical, repeatable, and quiet. Most months pass without an emergency. That is what makes it sustainable as a side income next to a primary job.

Why Boring Is the Feature

Most side hustles sold online are exciting because excitement sells courses. Excitement is also the failure mode. The work that actually pays the bills is rarely exciting. It is recurring, reliable, and structurally unspectacular. Bookkeeping sits at the deep end of the unspectacular pool.

Boring is the feature.

Three reasons the unglamorous nature of the work is the thing that makes the income hold:

The work has to get done. Every small business needs clean books. Every owner who runs a small business hates doing the books. The function does not go away when the economy tightens, because the IRS does not care what the economy is doing. Your role exists because the alternative for the client is doing the books themselves, which they will not.

Switching bookkeepers is friction. Once you have the chart of accounts dialed in and the client’s vendor patterns learned, you are cheaper for the client to keep than to replace. The replacement bookkeeper has to relearn what you already know. Most clients do not bother unless something goes badly wrong.

Bookkeeping is high-trust. Clients give you bank feed access. They give you receipts. They give you the financial picture they often will not even show their spouse. That trust takes months to build and they do not want to rebuild it with somebody new.

The implication of those three together: client acquisition is the hard part of this income model. Client retention is mostly automatic if the work is clean and the deliverables are on time. That is the inverse of most side hustles, where you have to keep selling to keep eating. Here, you sell once per client and then the revenue arrives on a schedule until the client closes the business or sells it.

The Path From Zero to First Client

The realistic learning and acquisition path runs through five steps.

Learn the software. QuickBooks Online is the dominant tool for small-business bookkeeping in the United States. Intuit runs a free certification program called QuickBooks ProAdvisor. The full study path and the exam cost nothing, and a focused learner can complete the ProAdvisor certification with structured evening study. That credential is recognized by clients and gets you into the Intuit directory for free.

Practice on your own books. Set up QuickBooks Online for any side gig or household financial tracking you already do. Categorize thirty days of real transactions. Reconcile the month to a real bank statement. Build the muscle on data you already understand. The first time you reconcile a real account end-to-end you stop feeling like a student and start feeling like a bookkeeper.

First client through your existing network. Most first clients come from people who already know you and run a small business. Identify three small business owners in your professional or community network. Offer to do their monthly bookkeeping at a starter rate for the first three months in exchange for a testimonial. Use the starting-from-zero approach for the full first-client path.

Price the first client correctly. $150 a month for the first three months, then $250 a month at the same scope, is a defensible starter. Or charge $250 from the first month if confidence is there. Do not undersell. Clients who pay $50 a month treat you like a $50-a-month vendor and waste your time with low-value back-and-forth. Clients who pay $250 a month respect the function and the relationship.

Second and third clients through referrals. Once the first client is happy with the deliverables, ask for referrals to other small business owners. Bookkeeping is a word-of-mouth function. Owners talk to other owners about who keeps their books. A clean reputation moves through small-business networks fast.

Three to five basic-tier clients is the typical sustainable solo plateau. That range closes a meaningful household income gap, fits inside ten to fifteen hours of monthly work, and stays manageable without giving up evenings or weekends. The plateau shifts as service depth grows. That is covered next.

How the Retainer Grows With You

The basic tier is not the end of the road. Same client, deeper service, higher retainer. The progression is gradual and entirely optional. Most readers will land somewhere along it and stay there because the work-to-revenue ratio sits in a good place at every tier. The point is that the path past the entry exists and that it is honest, not aspirational.

Tier 1, basic bookkeeping ($250 to $500 per client, per month). This is the entry path the article has been describing. Categorization, reconciliation, monthly profit and loss statement, balance sheet. QuickBooks ProAdvisor certification is enough to start. Three to five clients fits inside ten to fifteen hours of monthly work. Most new solo bookkeepers spend the first year here while the skills consolidate and the workflow becomes second nature.

Tier 2, expanded service lines ($500 to $1,000+ per client, per month). As you learn payroll processing, more detailed reporting, sales-tax filings, and light financial analysis, the retainer per existing client grows. You have not necessarily added more clients. You have added depth to the relationship. The same five clients can move from $1,500 of monthly recurring revenue at the basic tier to $3,000 or more once the service mix expands. The skills that unlock Tier 2 take a year or two of doing the work to acquire honestly.

Tier 3, advisory and reporting ($1,000 to $2,500+ per client, per month). At this layer, you are the financial sounding board. The client comes to you before making decisions, not just at month-end to look at numbers. Hours per client typically drop because the relationship carries the value, not the volume of transactions you process. This tier usually requires several years of bookkeeping experience and often pairs with additional credentials, such as Enrolled Agent or specialized industry knowledge.

Tier 4, the firm model. If the path continues, the high-value advisory work stays yours while the basic categorization gets contracted to other bookkeepers you have trained. The labor stops being all yours, the revenue picture changes structurally, and the function becomes a small firm rather than a side income. Most readers will not get here, and that is fine. The function works at Tiers 1 through 3 without needing to scale into a firm. Tier 4 is the runway, not the destination.

The honest takeaway: most readers will land at Tier 1 or Tier 2 and stay there because that is where the work-to-revenue ratio sits best for a side income alongside a primary job. The runway exists. You do not have to walk all of it for the function to be worth running. The skill stack is the asset, and the asset compounds.

Why This Function Holds Up When Life Changes

Most side hustles are tied to a place or a schedule. Bookkeeping is not. The structural features of the work make it survive the things that disrupt other income streams.

The work is location-independent by default. In 2026, virtually every small-business client expects their bookkeeper to operate remotely. The bank feed, the accounting software, and the client communication all live online. A move to a new city does not reset the client list. That includes a PCS move; the client list follows because the client never needed to know your duty station in the first place.

Pauses are tolerable with planning. A bookkeeper who arranges backup coverage with another bookkeeper, or who batch-prepares known periods in advance, can take real time away from the function without losing the client. The recurring structure absorbs short gaps in a way that gig work and product launches do not. Gig income stops the day you stop working. Bookkeeping income pauses and resumes.

The function is hours-controllable. You decide how many clients you accept. The work per client is bounded and predictable. There is no inbound rush, no campaign cycle, no algorithm change that doubles your workload overnight. The volume scales with a decision you make, not with a force outside your control.

The BetterQuality Consulting client base survived the move out of active service, the launch of two adjacent businesses, and the slow rebuild that those launches required. A small handful of clients on monthly retainers produces a steady five-figure annual revenue stream from the function alone, and the cost structure is almost nothing: a software subscription, a laptop, and the time to do the work cleanly. The recurring monthly retainers paid the household bills while the other businesses were finding their footing. Boring revenue is the floor under everything else, and the floor matters more than the ceiling when other parts of the income picture are moving around.

The Function, Not Just the Side Hustle

Bookkeeping is one of the Three Business Functions every small business needs: Marketing, Technology, and Accounting. The function this article walks through is the Accounting function. The broader EM-P4 model, Learn It, Use It, Sell It, frames any of the three functions as the same kind of path. You learn the function well enough to use it on your own work. You use it long enough to build proof. Then you sell it as a service to small businesses that need it and do not want to do it themselves.

The same logic that makes bookkeeping work, the recurring retainer, the location independence, the high client stickiness, applies to social media management, website maintenance, payroll oversight, and a half-dozen other function-level services. The Accounting function happens to be the one I run. The framework is bigger than the specific function. The reader who finds bookkeeping fits their wiring should run with it. The reader who is allergic to spreadsheets should still get the framework and pick a different one of the three functions to pursue.

The shape of the income stays the same across all three: monthly retainer, small fixed work per client, revenue that scales with client count and with service depth over time. Reader who fits the personality picks bookkeeping. Reader who would rather make things than tally them picks Marketing. Reader who would rather solve technical puzzles picks Technology. Same income shape, three different daily textures, one shared framework underneath.

Build Your Recurring Revenue Stack

Millionaire Veteran is a free community where military families build income on two timelines: the Cash Injection Playbook for fast cash now, and the Learn It, Use It, Sell It framework for the recurring retainer income this article walked through. The Compass Method routes every new dollar, fast or recurring, to the right purpose instead of lifestyle creep. The full implementation, built on your real numbers with a personal AI advisor, lives inside the community.

About the Author

Joshua Breaux

Retired U.S. Marine

Financial Management Analyst

BS & MBA in Analytics

His family runs on the same systems he teaches here.

This content is educational and does not constitute personalized financial advice. Millionaire Veteran is not affiliated with the Thrift Savings Plan, FRTIB, or the U.S. Government. Past performance does not guarantee future results.