Part 3 explained the mechanics of cash flow management: separation by purpose, distribution by percentages, balances as truth. This article names the system and shows you what it looks like when it is running.

The Compass Method is a cash flow management system. Six accounts. A manual distribution ritual on every payday. Labeled debit cards. Optional precision accounts for larger households. A monthly calibration check that keeps the whole thing honest.

The blog shows you the architecture. The full implementation, built on your real numbers with a personal AI advisor, lives inside the Millionaire Veteran community.

The Six Compass Accounts

Six accounts. Four checking, two savings. The structure never changes regardless of income, debt, or stage of life. Only the amounts flowing to each account change.

Income (IN). All income lands here. Every DFAS deposit, every allowance, every bonus, every side income. This is a pass-through account. On payday, you distribute from here to the other five. After distribution, Income is at zero. Every dollar has been assigned a destination. No legacy autopays or spending should be attached to this account. It exists only to receive and distribute.

Essentials (ES). The must-pay obligations. The test: if I stopped paying this, would something break? Break means eviction, repossession, shutoff, collections, or legal consequence. If the answer is yes, it belongs in Essentials. Rent or mortgage, car payment, insurance premiums, utilities, minimum debt payments, childcare. Autopay runs from this account for everything that has a fixed due date and a fixed or estimable amount.

Lifestyle (LS). Discretionary spending. Eating out, entertainment, personal purchases, hobbies, coffee. When this account is empty, discretionary spending stops until the next payday. That is the system working, not the system failing. The balance refills on payday and the cycle starts again.

Debt/Invest (DI). Milestone funding. During debt payoff, this account holds the extra payments above minimums that are attacking the debt. Once the debt is cleared, the same account shifts to investment funding. The member renames it from DI.Debt to DI.Invest when the transition happens. Same account, new mission. That rename is a milestone moment. No debit card on this account. Money leaves only through intentional transfers.

Emergency (EM). The reserve. A savings account. Untouched unless something genuinely breaks: a car repair that cannot wait, a vet bill, an urgent flight home. When emergency funds are needed, transfer to Essentials and pay from there. Accessing this money should require a conscious decision, not a card swipe. The Emergency account has a target balance and gets funded steadily until it reaches that target.

Planned (PL). The account that makes the good stuff possible. Vacation, holiday gifts, a down payment on the next vehicle, the family trip you have been putting off. When Planned is active, small amounts accumulate every pay period so the money is already there when it is time. When it unlocks and how much flows to it depends on where you are in the system. The AI advisor inside the community sorts that out with your real numbers.

Why six? Fewer than six forces categories to share accounts, which recreates the pooled-balance problem from Part 1. Six is the foundation where every major spending purpose has its own balance and its own truth. Some households add precision accounts within these six categories as they get comfortable with the system, but the six core accounts are where everyone starts.

The Payday Ritual

Every recurring income deposit triggers the Payday Ritual. Money lands in Income. You distribute it to the other five accounts based on your allocation percentages. Income hits zero. Every dollar distributed.

The Payday Ritual is manual. That is by design. The act of distributing your income on payday builds the behavioral connection between earning and allocating. Automating the transfers removes the one moment where you actively engage with where your money is going. The ritual takes 15 to 20 minutes the first time. Under five minutes once the percentages are established and the rhythm is familiar.

The allocation percentages stay the same across all deposits. If you are paid biweekly, each paycheck triggers the same percentages. If BAH deposits on a separate schedule, it triggers its own distribution using the same percentages. The dollar amounts differ because the deposit sizes differ, but the percentages are constant.

Two months per year, biweekly pay produces a third paycheck. That is bonus income. Run the same distribution or direct it toward the active milestone. The family decides.

Point Accounts

The six Compass Accounts work on their own. Point Accounts are the next level of clarity when you want it.

Here is the problem they solve. Essentials covers rent, utilities, insurance, groceries, gas, and every other must-pay obligation. That is a lot of purposes sharing one balance. When the Essentials account shows $1,400 and rent drafts in three days for $1,200, the groceries money is technically in there but it is hiding behind the rent. You are back to mentally subtracting, which is the exact problem the system was supposed to fix.

Point Accounts split that single balance into pieces that each tell their own truth. The bills that autopay on a schedule go to one account. The groceries and gas you control week to week go to another with its own card. When that card’s account says $290, that is what is left for groceries. No subtraction. No guessing which part of the balance is spoken for.

The same idea works for Lifestyle. Fixed subscriptions go to one account. Discretionary spending goes to another. For couples, each partner gets their own personal spending account with their own card and their own balance. No check-ins. No “can I buy this?” conversations. A shared account covers the things you do together. Each person sees their own number and makes their own decisions.

This was the single best financial move I made in my own household. When my wife and I split Lifestyle into personal accounts, the clarity and autonomy it created changed everything. She spends her money. I spend mine. Neither of us has to explain a purchase or ask permission. The shared account covers what we do together. We have avoided more arguments with this one structural decision than with any conversation about money we have ever had.

That is what Point Accounts do. They take the six core accounts and zoom in where a single balance is still too broad to give a clear answer. The full setup, including the naming system and exactly how to configure them at your bank, lives inside the free community. You get the full playbook with nothing withheld.

The Allocation Decision

This is the hardest part. Harder than opening accounts, harder than learning the ritual.

Essentials are calculated first. Add up every must-pay obligation: rent, car, insurance, utilities, minimums, childcare. That number is fixed. It gets funded before anything else.

The remaining pool is everything that is left after Essentials (both fixed and variable) and any fixed Lifestyle commitments (subscriptions). This remaining pool splits across discretionary Lifestyle, Debt/Invest, Emergency, and Planned. It must total to zero. Every dollar gets a destination.

The Compass Method follows one rule here: decide what goes to the active milestone BEFORE deciding what goes to discretionary Lifestyle. Emergency gets funded until the buffer target is reached. Debt/Invest gets funded based on the active milestone (the current goal in the sequenced financial plan). Planned gets a fixed amount based on upcoming irregular expenses divided across pay periods. Lifestyle gets what remains.

That last part is deliberate. If Lifestyle feels too small after funding milestones, the signal is that obligations are consuming too much of the income, or that income needs to grow. The Lifestyle number is honest.

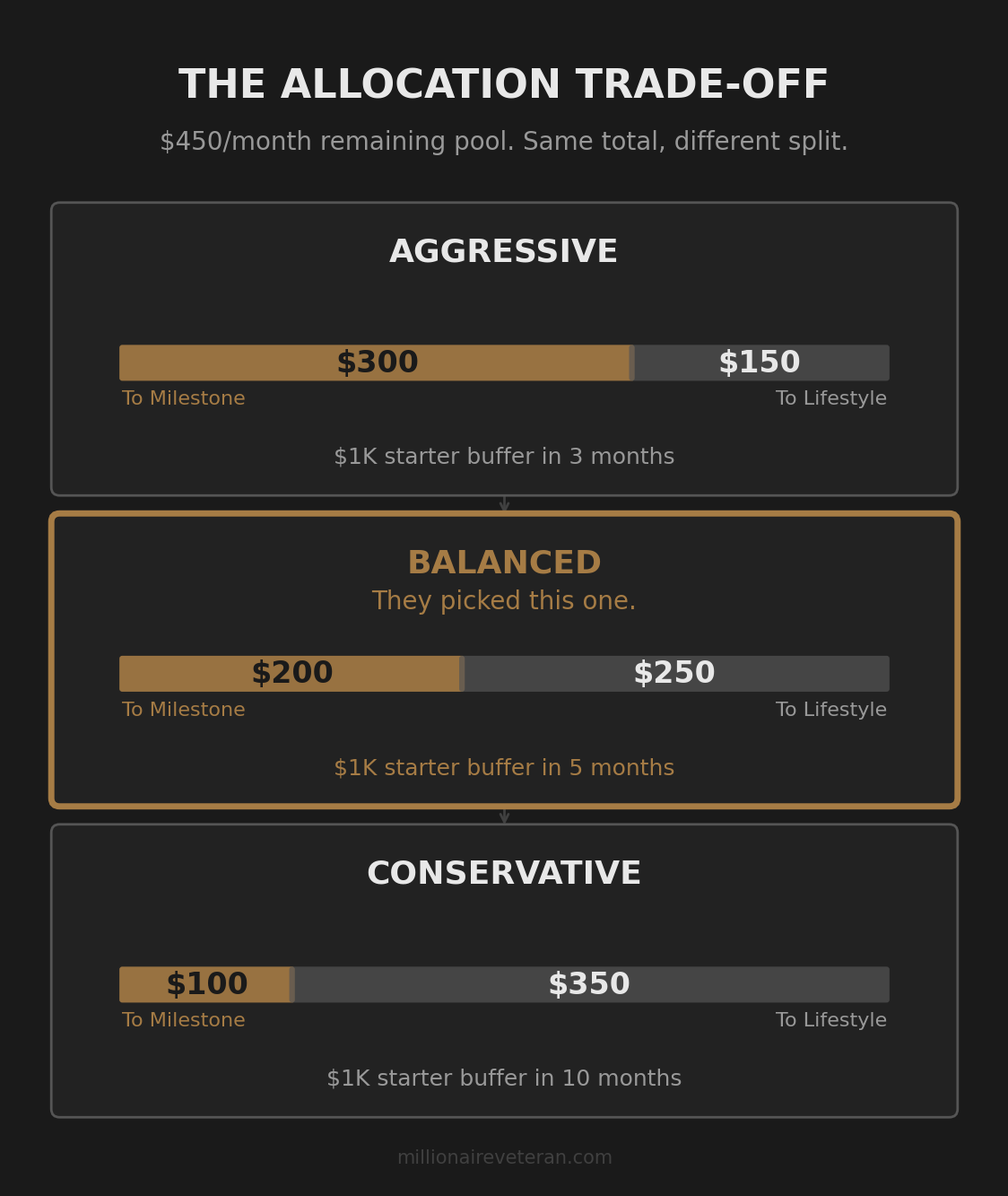

In the Basilone family story, John and Lena had $450 per month in remaining pool after all essentials and fixed commitments. They faced the allocation trade-off head on:

| Split | To Milestone | To Lifestyle | What It Means |

|---|---|---|---|

| Aggressive | $300/mo | $150/mo | Buffer funded in 3 months, tight lifestyle |

| Balanced | $200/mo | $250/mo | Buffer funded in 5 months, sustainable |

| Conservative | $100/mo | $350/mo | Buffer funded in 10 months, more breathing room |

They picked balanced. $200 per month to the milestone. $250 to Lifestyle. They could still go on a date. They were not running themselves into the ground. The milestone took longer than the aggressive path but they sustained it without burning out.

That trade-off between speed and sustainability is personal. An aggressive split that guts quality of life gets abandoned in six weeks. A sustainable split that preserves enough room to live gets maintained for a year. Consistency beats intensity.

The allocation is a living decision. It changes as milestones are reached, as income shifts, and as life circumstances evolve. A PCS changes BAH and cost of living, which means the Essentials number shifts and the percentages need recalculating. A promotion opens room to increase milestone funding without cutting Lifestyle. A new child changes the Essentials number permanently. Each of these triggers a recalculation of the allocation percentages, not a rebuild of the system. The accounts stay the same. The ritual stays the same. The percentages adjust to fit the new reality.

Credit Card Freeze

When the Compass Method starts, credit card spending stops. All of it.

The system cannot tell the truth if new debt is being created outside of it. A credit card charge that does not flow through the Compass Accounts is invisible to the balances. It creates obligations that the system does not know about, which means the account balances are lying again, just from a different direction.

If credit cards have been covering the gap between paychecks, the Compass Method makes that gap visible for the first time. The Lifestyle balance will show exactly how much discretionary money exists. If that number is uncomfortably small, the system is revealing what was previously hidden by credit card spending. That is the system working. The credit card was masking a cash flow problem, not solving it.

If covering Essentials requires credit, that is an income signal. The Compass Method did not create the problem. It surfaced it. The response is on the income side, not the spending side.

Existing credit card debt gets absorbed into the milestone sequence. Minimum payments are an Essential obligation. Above-minimum payoff comes from the Debt/Invest account as part of the active milestone. If the details here feel like a lot, that is expected. The community has full courses and a personal AI advisor that holds the entire system and walks you through it step by step with your real numbers. You do not need to memorize this article. You need to understand enough to know the structure exists and that it works.

What the First Three Months Look Like

Month one: calibration. The allocation percentages will be off. Groceries will run out too early or have money left over. The Lifestyle number will feel too tight or surprisingly adequate. Planned might not have enough yet for the vacation you are eyeing. All of this is expected. Month one is data collection. Check each account balance at the end of the pay period. Note which ran out and which had surplus. Adjust the percentages for month two.

Month two: refinement. The groceries allocation is closer to reality. The Lifestyle number feels honest. Emergency is building. Essentials covers what it needs to cover without thought. You notice that checking the discretionary balance before a purchase has become automatic. The number, whatever it is, feels real.

Month three: rhythm. The Payday Ritual takes under five minutes. The cards are labeled and grabbing the right one is automatic. Autopay handles Essentials. Groceries and Lifestyle spend from their own accounts. The monthly calibration check catches any drift: an account that consistently runs dry gets a percentage increase. An account building unused surplus gets a decrease. The system stays calibrated because you check it, not because it is static.

Build It With Your Numbers

You just read the system. Now build it.

The Millionaire Veteran community is free. Inside, the Milestone 0 (M0) course pairs you with a personal AI advisor that runs the Diagnostic Review on your real income, your real debts, and your real obligations. It scores your debts by how much cash flow they drain. It classifies every charge as Essential or Lifestyle. It builds your account architecture and calibrates your allocations. The Compass Method stops being an article you read and starts being the system your household runs on.

The balance is the answer. Yours starts here.

About the Author

Joshua Breaux

Retired U.S. Marine

Financial Management Analyst

BS & MBA in Analytics

His family runs on the same systems he teaches here.

This content is educational and does not constitute personalized financial advice. Millionaire Veteran is not affiliated with the Thrift Savings Plan, FRTIB, or the U.S. Government. Past performance does not guarantee future results.