If you searched “Roth TSP vs Traditional TSP” and bounced through three articles that all answered “it depends” before sending you to a calculator, you are not alone. That answer is technically correct and practically useless. It depends on tax rates, retirement timeline, deployment status, and matching mechanics that most civilian-focused articles either ignore or get wrong for military readers.

The straight answer for the vast majority of service members under the Blended Retirement System is Roth, with one critical wrinkle that almost nobody explains: the matching system gives you Traditional whether you wanted it or not, so the real question is never which one to choose. It is how to manage the ratio between them over a career.

This article walks through why Roth wins for most service members, why you already have a Traditional balance you may not have planned for, and how the ratio shifts as your career, deployments, and rank change. It uses 2026 figures throughout and assumes the reader is military, contributing under BRS, and looking for a real answer instead of a hedge.

Roth and Traditional: The Tax Mechanics

Roth contributions come from after-tax money. You pay federal income tax on the contribution in the year you make it, the money grows tax-free inside the account, and your withdrawals in retirement are tax-free. You never owe federal income tax on Roth dollars again.

Traditional contributions come from pre-tax money. Your taxable income drops in the year you contribute, by the amount you contribute. The money grows tax-deferred. You pay ordinary federal income tax on every dollar you withdraw in retirement, at whatever rate applies in the year you take it out.

That is the entire mechanical difference. The Roth TSP vs Traditional TSP question is whether you are better off paying the tax now or paying it later. The rest of this article answers that for a service member under BRS.

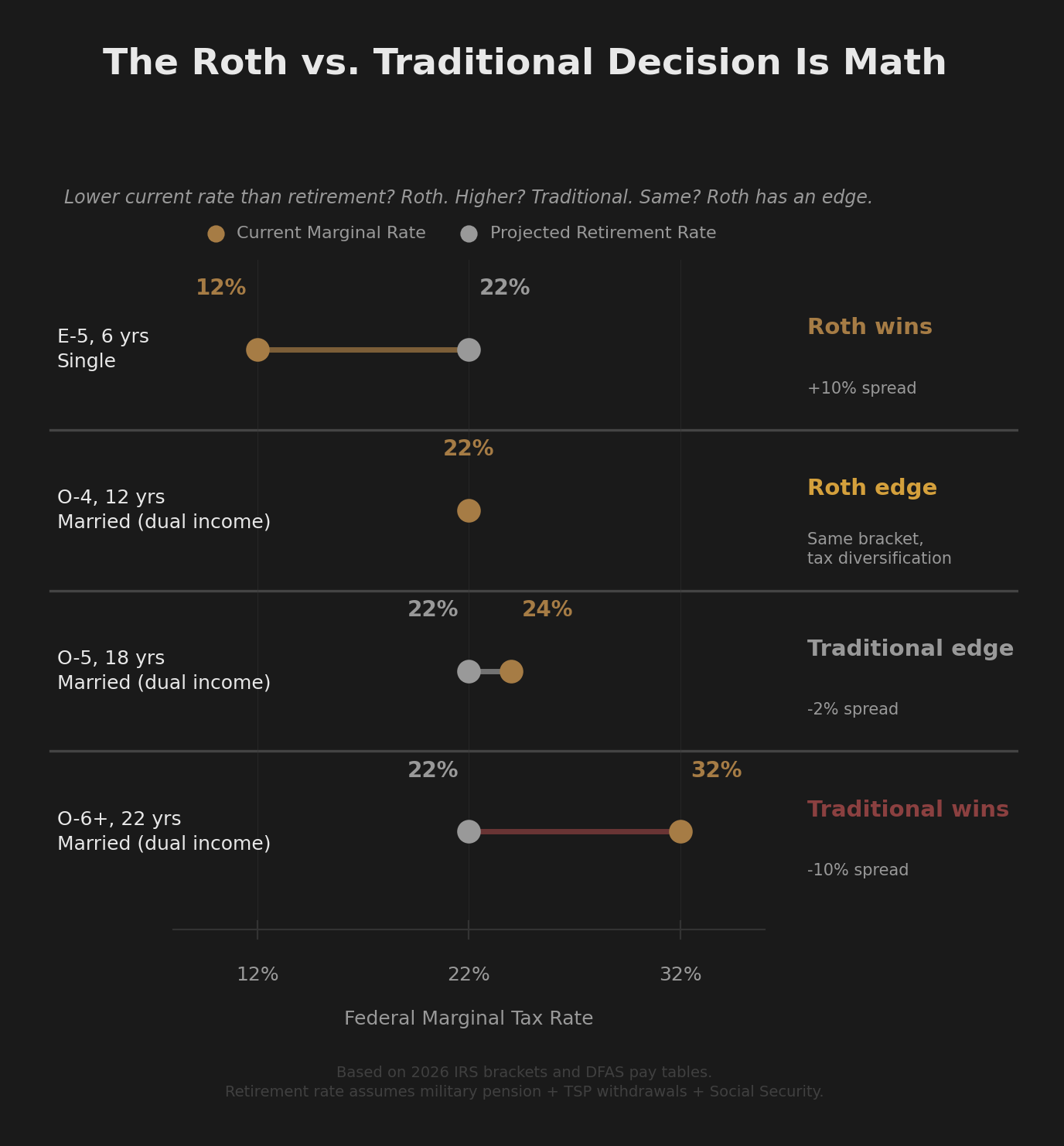

Why Roth Wins for Most Service Members Under BRS

The Roth TSP vs Traditional TSP decision comes down to one comparison: the marginal tax rate you pay on contributions today versus the marginal tax rate you will pay on withdrawals in retirement. If today’s rate is lower, Roth wins. If retirement’s rate is lower, Traditional wins. If they are equal, Roth still has the edge for two structural reasons covered below.

For military members under BRS, the math points to Roth for four compounding reasons.

Current marginal rates are low for the bulk of the force. Enlisted ranks E-1 through E-7 sit in the 10% or 12% federal bracket in 2026 after the standard deduction. Junior officers O-1 through O-3 sit between 12% and 22% depending on filing status and household income. Non-taxable allowances like BAH and BAS keep adjusted gross income lower than total compensation suggests. Paying 12% today on a dollar you will never owe tax on again is one of the strongest positions available in the U.S. tax code.

Retirement income usually stacks into a higher bracket. A BRS retiree at 20 years collects 40% of high-3 base pay as a defined pension, taxable as ordinary income. That alone often clears the standard deduction. Add Social Security, working spouse income, civilian second-career earnings, and TSP withdrawals, and most military retirees find themselves in the 22% bracket or higher in retirement. Every Traditional dollar contributed at 12% during service costs you 10% more on the way out. Every Roth dollar contributed at 12% comes out tax-free.

Combat zone deployments are a Roth accelerator. When you deploy to a designated combat zone, military pay earned during those months is exempt from federal income tax under the Combat Zone Tax Exclusion. Your effective tax rate on that income is zero. Contributing to Roth TSP during a CZTE deployment means the money enters tax-free, grows tax-free, and exits tax-free. There is no better tax position available anywhere in the code for a retirement contribution. Most service members who deploy either miss this window or do not use it fully.

Military pay is unusually predictable. Civilians cannot project their bracket five years out with any confidence. You can. The pay tables are published. Promotion timelines, while not guaranteed, follow patterns. BAH is published annually by ZIP code. An E-3 in their first enlistment can map out their probable bracket at year 5, 10, 15, and 20 within a reasonable range. That projection reliability is what makes the Roth vs Traditional calculation precise for service members in a way it almost never is for civilians.

The exceptions exist. Senior officers approaching retirement with a high-earning spouse, planning a low-income retirement, and confident the retirement bracket will be lower than the current one have a genuine Traditional case. So do members with very specific tax planning needs around state of residence in retirement. These are real but they are the minority. For the majority of service members under BRS who are actively contributing, the answer to “Roth TSP vs Traditional TSP” is Roth.

The Match Wrinkle: You Already Have Traditional Whether You Wanted It or Not

Here is the part the calculator articles do not surface.

DoD matching contributions always go to Traditional TSP. Always. It does not matter what you elected for your own contributions. If you set your TSP contribution to 100% Roth, every dollar of agency matching that lands in your account is Traditional. This is not an oversight or a setting you can change. It is how the system is built.

Vesting works the same regardless: the 1% agency automatic contribution vests after two years of service. The matching contributions begin at two years of service and are immediately vested when received. Your own contributions, Roth or Traditional, are 100% yours from the first paycheck.

The practical consequence: if you have been contributing under BRS for more than two years, you have a Traditional balance in your TSP whether you chose to or not. After a full 20-year career with consistent 5% Roth contributions, a meaningful portion of your total balance, including all the growth on the matching dollars over those decades, sits in Traditional.

This wrinkle is not a bug. It is the structural starting point for the rest of the article. You do not get to pick “all Roth” or “all Traditional” inside the TSP. You get to pick what your own contributions go into, while the match runs in parallel. Every active contributor under BRS ends up with both buckets eventually.

The Real Skill: Managing the Ratio Over Time

The ratio is what separates service members who optimize their structural decisions from those who do not. Five inputs shift it.

Career stage. An E-3 in their first enlistment, basic pay around $30,000, 12% bracket, has no business contributing to Traditional. Every contribution should be Roth. The match runs Traditional in the background and that is more than enough Traditional exposure at this stage. A 100% Roth election here means the ratio at year 4 might be 80% Roth contributions plus 20% Traditional from matching, weighted toward Roth where it belongs.

A mid-career E-7 or O-4 with household income pushing into the 22% bracket has a different calculation. The bracket spread narrows but Roth still wins on retirement bracket projection plus the structural advantages below. The ratio at this stage is often still majority Roth contributions, with the gradual growth of the Traditional matching balance still doing its work in the background.

A senior O-5 or O-6 approaching retirement with high household income and known retirement plans may have the only genuine case for tilting personal contributions toward Traditional, and even then only if the retirement bracket will be meaningfully lower than the current one. This is the minority case.

Deployment status. Every CZTE month is a Roth-only window. If you deploy in 2026 and want to maximize the value of that deployment, the Roth contribution percentage on your TSP election needs to be set before you leave. The dollars going in during the combat zone period are taxed at 0% on the way in. They will be taxed at 0% on the way out. There is no version of this where Traditional is the right choice during CZTE months.

The mandatory Roth catch-up rule. As of January 1, 2026, if you are age 50 or older and your prior-year FICA wages exceeded $150,000, all your catch-up contributions must be designated Roth. You cannot route catch-up to Traditional even if you want to. DFAS handles the routing automatically once the threshold is crossed. This rule affects senior officers and senior enlisted with significant special pays. For anyone caught by it, the ratio shifts toward Roth in the catch-up phase whether they planned it or not.

The conversion window. As of January 28, 2026, TSP allows in-plan Roth conversions. You can move money from your Traditional balance to your Roth balance, pay the tax on the converted amount in the year of conversion, and gain Roth treatment on those dollars going forward. The conversion case holds when current bracket is lower than expected retirement bracket and you have cash outside the TSP to pay the conversion tax. Deployment years, mid-career bracket bumps you are about to outgrow, and the year of separation are the windows where in-plan conversions can re-tune a Traditional-heavy balance toward the ratio you actually want.

Withdrawal flexibility in retirement. Roth TSP has no required minimum distributions as of 2024 under SECURE Act 2.0. Traditional balances are subject to RMDs starting at age 73. This means a Roth-heavy retiree gets to control the timing of every dollar of taxable income. A Traditional-heavy retiree gets forced into a minimum taxable withdrawal whether they need the money or not. The ratio you build during service determines the flexibility you have in retirement.

The ratio is not a one-time decision. It is a continuous adjustment across a career.

The 2026 Rules You Need to Know

The mechanics matter. These are the numbers and timelines for 2026.

Contribution limits. The elective deferral limit for 2026 is $24,500. This is the cap on your own contributions across Roth and Traditional combined, before any catch-up contributions and before the agency 1% and matching contributions. The annual additions limit, which caps your contributions plus all agency contributions plus any tax-exempt combat pay contributions, is $72,000.

Catch-up contributions. If you turn 50 or older in 2026, you can contribute an additional $8,000 in catch-up beyond the elective deferral limit. Total possible: $32,500 in elective deferrals plus catch-up. If you are between ages 60 and 63 during 2026, the SECURE Act 2.0 enhanced catch-up gives you $11,250 instead of $8,000, raising your total possible to $35,750. At 64, you drop back to the standard $8,000 catch-up. This is a narrow window for senior members.

The mandatory Roth catch-up rule. Effective January 1, 2026, members aged 50 and older with prior-year FICA wages above $150,000 must designate all catch-up contributions as Roth. DFAS routes them automatically. This primarily affects senior officers, O-5s and O-6s with significant longevity and special pays, and the most senior enlisted ranks. If you are in this window and were counting on the tax deduction from Traditional catch-up, the deduction is gone and your withholding should be reviewed.

In-plan Roth conversions. TSP enabled in-plan Roth conversions on January 28, 2026, marking the first time participants could convert Traditional balances to Roth without separating from federal service. The mechanics: a minimum of $500 per conversion, maximum 26 conversions per calendar year, and you must leave at least $500 in each non-Roth payroll source after converting. Conversions are permanent. The TSP does not withhold tax on the conversion, so you owe the tax bill yourself, generally through quarterly estimated payments to the IRS to avoid underpayment penalties. The conversion does not satisfy any required minimum distribution.

Contribution timing. TSP matching is calculated per pay period. There is no annual true-up. If you contribute aggressively in the first half of the year and hit the elective deferral limit by August, your contributions stop, and so does the matching. The fix is mechanical: divide your annual target by 26 pay periods. For someone maxing the elective deferral with no catch-up, that is roughly $943 per paycheck. For someone over 50 with full catch-up, $1,250 per paycheck. Steady contributions across the full year guarantee full matching eligibility every period.

CZTE contribution cap. Combat zone tax-exempt pay can be contributed to Roth TSP only up to the elective deferral limit of $24,500. Any combat zone contributions beyond that limit must go to Traditional. The annual additions cap of $72,000 still applies as the ceiling on all contributions, your own plus agency, including tax-exempt combat zone amounts.

The figures cited here reflect 2026 IRS and TSP guidance. These numbers move annually with cost-of-living adjustments. Verify current figures at TSP.gov and IRS.gov before the next tax year.

The Structural Audit

Five questions. Answer with numbers, not feelings.

What is your current marginal federal tax rate? Pull your most recent tax return, find your taxable income, and map it to the 2026 bracket table. If your rate is 12% or 22%, Roth is almost certainly the right default for new contributions. If your rate is 24% or higher and you expect retirement income to be lower than your current income, the Traditional case opens.

What is your projected retirement marginal rate? This is the subjective input. Estimate it by adding up your projected pension (40% of high-3 at 20 years), Social Security, expected spouse income in retirement, anticipated TSP withdrawal rate, and any second-career earnings. Map the total to brackets. Most military retirees land in the 22% bracket. If you are contributing at 12% now and pulling out at 22% later, every Traditional dollar costs you 10% in the lifecycle and every Roth dollar saves it.

Are you maximizing CZTE windows? Every dollar contributed to Roth during a combat zone month is taxed at 0% in and 0% out. If you have a deployment in your future, your TSP contribution election should be set before you leave. If you have deployments behind you where you did not max Roth, those windows are closed permanently. Future deployments get the same treatment.

Is your contribution timing optimized for matching? Take your annual target, divide by 26, and confirm that your per-paycheck contribution leaves you contributing every pay period through December. If your contributions stop in October or November because of front-loading, you are leaving matching dollars on the table every year you do it.

If you are catch-up eligible, are you structured for the mandatory Roth rule? If you are 50 or older and your FICA wages cleared $150,000 last year, your catch-up contributions are Roth by mandate. Confirm your withholding accounts for the after-tax routing. If you were budgeting around a Traditional catch-up deduction, adjust.

These are not hypothetical questions. Each one has a number attached. The number tells you what to do.

I run this audit on my own TSP every January.

Structure Is One Half. Allocation Is the Other.

You came here with a Roth vs Traditional question. If you worked the audit above, you have a clear answer or a bounded set of good options.

That is one half of the TSP equation. The other half is allocation: what funds your money is in, and whether your approach to managing that allocation is one you actually chose or one you fell into.

Most service members sophisticated enough to be researching Roth vs Traditional also have opinions about their fund allocation. They are 100% C Fund because a buddy told them to. They are in an L Fund because it seemed reasonable. They picked a split years ago and never revisited it. The structural decisions you just audited are precise. Brackets. Limits. Mechanics. Your allocation approach deserves the same rigor.

The question worth asking next: did you choose your allocation pattern, or did you fall into it? That article walks through the four patterns every BRS service member ends up in, and the gap that exists in each of them.

New to BRS? The Blended Retirement System fundamentally changed the role of your TSP from supplemental to structural. If that context is new, start here.

Get the Firewatch Blueprint

The structural audit above gives you the framework. The Firewatch Blueprint gives you the full picture: the Roth vs Traditional decision guide that resolves the clear cases outright, a personal worksheet for the middle cases, and the allocation side of the equation that the audit only pointed at.

Three timeline-appropriate approaches matched to three career stages. The data behind each. And a framework for choosing based on your actual situation, not someone else’s Reddit comment.

About the Author

Joshua Breaux

Retired U.S. Marine

Financial Management Analyst

BS & MBA in Analytics

His family runs on the same systems he teaches here.

This content is educational and does not constitute personalized financial advice. Millionaire Veteran is not affiliated with the Thrift Savings Plan, FRTIB, or the U.S. Government. Past performance does not guarantee future results.