Part 1 identified the problem: money in one pile, no visibility by purpose. Part 2 showed the four patterns people fall into when they lack structure. This article explains what the structure actually is and how the mechanics work.

A cash flow management system separates money by purpose at the bank account level. Separate accounts, each serving one function, each with its own balance. Income arrives, gets distributed across the accounts by a set of percentages, and from that point forward each balance tells you what is available for that purpose. The distribution happens every time income deposits. The balances stay current because the bank updates them, not because you remembered to log something.

That is the whole idea. The rest of this article is the mechanics.

What “System” Actually Means

The word gets used loosely. People call a spreadsheet a system. They call a budget app a system. Those are tools that require your ongoing participation to function. When the participation stops, the tool stops working.

A cash flow system is different because it operates on structure. The structure is the account architecture: separate checking accounts, each serving one purpose, each with its own balance. Once the architecture exists, the system works on a distribution rhythm tied to your pay schedule. You distribute money on payday. You spend from the right accounts between paydays. Each balance reflects reality without logging, categorizing, or reviewing transactions.

The difference shows up on a Wednesday evening when one partner asks if the family can go out to eat this weekend. With a tracking tool, you open the app, check your dining category, try to remember if you logged the coffee run from Tuesday, and make a judgment call about what the pooled balance can actually handle. With a cash flow system, you check one account balance. The discretionary account: $68. That is what is available for optional spending. The answer took three seconds and required no calculation, no memory, and no judgment call.

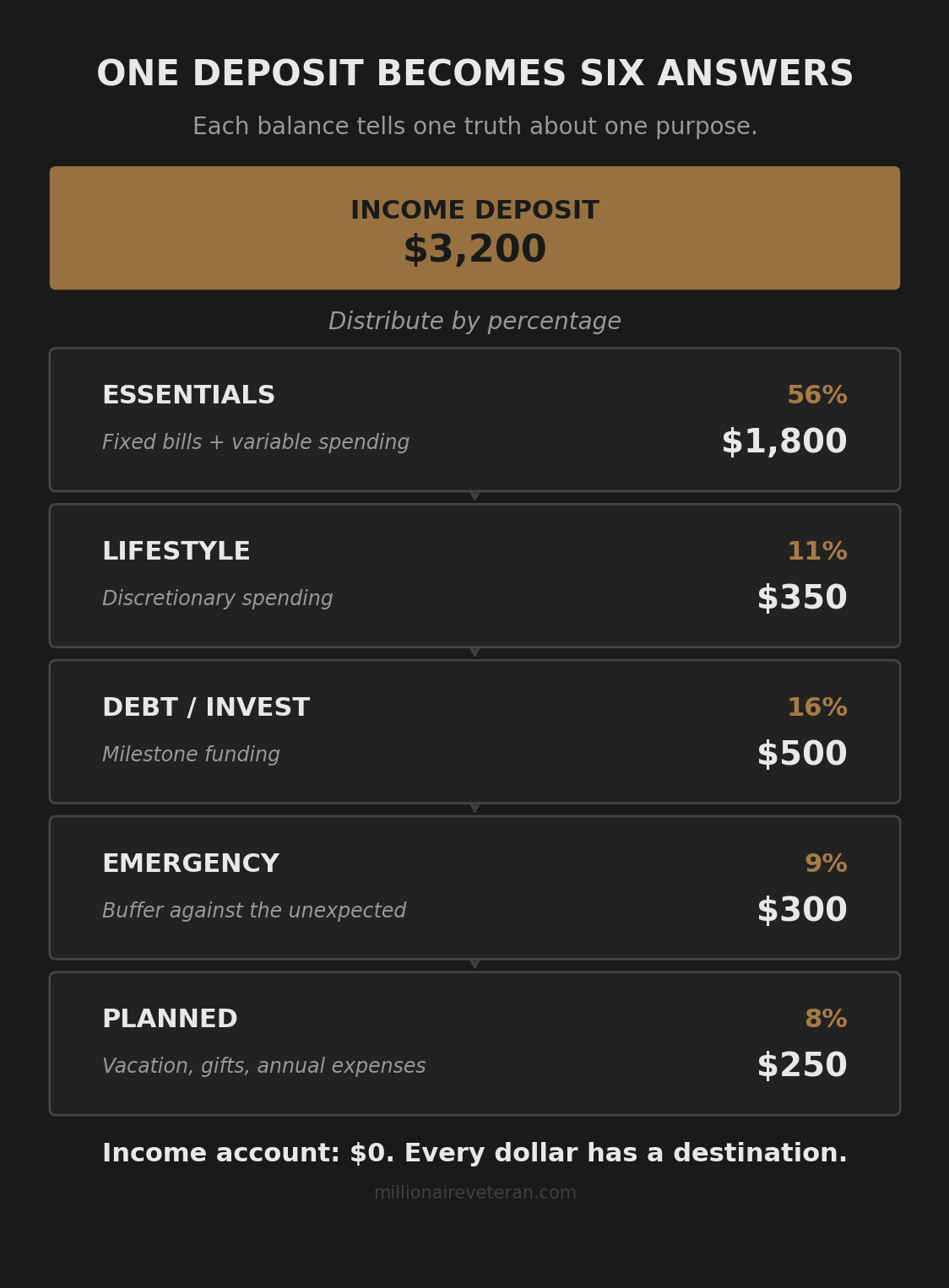

Separation by Purpose

Every dollar that enters your household serves one of a handful of purposes. Some dollars pay the mortgage. Some buy groceries. Some fund the emergency reserve. Some go toward debt payoff or investing. Some cover discretionary spending. Some are earmarked for known future expenses that land once or twice a year.

In a single checking account, all of these dollars sit in one pile with one number. That number cannot tell you how much is for groceries versus how much is committed to the mortgage versus how much is truly discretionary. The dollar committed to rent and the dollar available for date night look identical.

Separation by purpose means each major category gets its own account. All income lands in one account first. From there it gets distributed to the others. Fixed obligations go to one account: rent, utilities, insurance, car payment. Groceries and household supplies go to another. Discretionary spending goes to a third. Emergency reserves sit in a savings account. Milestone funding for debt payoff or investing sits in another. Known future expenses like holiday gifts, car registration, and annual insurance premiums accumulate in their own account so they stop feeling like emergencies when they arrive on schedule.

When money is separated, each balance tells one truth about one purpose. The fixed obligations account has $2,100. That covers this pay period’s committed bills. The groceries account has $340. That is what is available for food until the next payday. The discretionary account has $112. That is the money for optional spending, visible as a number, without any calculation.

The separation does the work that tracking tries to do. Tracking asks you to monitor every transaction and assign it to a category after the fact. Separation assigns the money to a category before any transaction happens. One approach requires daily attention to a tool. The other requires attention on payday plus the discipline to spend from the right accounts and check the balance before purchases. The system creates the visibility. You still have to use it.

The Envelope Method, Modernized

Cash envelopes worked for exactly this reason. Payday arrived, cash went into labeled envelopes: rent, groceries, gas, savings, spending money. When the grocery envelope was empty, groceries were done for the month. Nobody tracked transactions. Nobody categorized purchases. The physical separation was the entire system. The envelope balance was the truth every time you opened it.

The digital version applies the same principle with separate checking accounts. Each account is an envelope. When you spend from the groceries account, you are pulling from the groceries envelope. When you spend from the discretionary account, you are pulling from the discretionary envelope. The account balance is the modern equivalent of feeling the thickness of the envelope.

The principle survived a century because it works on human psychology. People spend differently from a $340 groceries account than from a $4,300 pooled checking account. The smaller, purpose-specific number creates natural restraint without requiring willpower. You see $340 for groceries, you plan meals around $340. You see $4,300 in a pooled account, you plan around a number that includes next week’s rent.

Most credit unions allow multiple checking accounts at no additional cost. Navy Federal works well for this and is what I use personally. The account setup is a one-time effort. The distribution that follows is a recurring rhythm.

The Distribution Rhythm

Each time income deposits, all of it lands in one account. From there, you distribute it to the other accounts based on a set of allocation percentages. The percentages stay the same regardless of which deposit it is. The dollar amounts adjust because the percentages are applied to whatever amount arrives.

This means the system scales with income changes. A promotion, a reenlistment bonus, a pay raise. The percentages stay the same. The dollars flowing to each account increase proportionally. A PCS that changes BAH means the deposit amount changes, but the percentages and the account structure stay the same. Adjust the percentages if needed at the next monthly check, but the system does not need to be rebuilt.

The distribution is manual. That is by design. The act of moving money from the income account to each purpose-specific account builds the behavioral connection between earning and allocating. Automating it removes the one moment where you actively engage with where your money is going. The distribution takes under five minutes once the percentages are established. The first time takes longer because you are learning the rhythm.

After distribution, the income account balance is zero. Every dollar has been assigned a destination. The rest of the period is spent from the right accounts. Earn, distribute, spend from the right accounts, repeat.

What “The Balance Is the Answer” Means in Practice

Before the system, the question at every purchase is “can I afford this?” That question requires calculation. Subtract committed obligations from the checking balance, estimate what is left for discretionary spending, remember what you already spent this week, and make a judgment call.

After the system, the question becomes “does this account have the money?” The discretionary account has $112. Dinner costs $45. The account goes to $67. The answer was in the balance before you asked the question.

For couples, both partners can see every account balance independently. No gatekeeper, no spreadsheet to interpret, no mental ledger that only one person maintains. “What can we spend on groceries this week?” is answered by a number both people can check on their own phone. The argument about what the checking balance really means disappears because each balance means exactly one thing.

The Monthly Calibration

The system requires ongoing attention. The distribution rhythm handles each pay period. But allocations need periodic review to stay accurate.

Once a month, check whether the system is calibrated. Are any accounts consistently running out before the next payday? That allocation is too low. Are any accounts building a surplus that sits unused? That money could be redirected to a milestone. Have any new recurring charges appeared that were not in the original plan? Subscription creep is real and it adds up silently.

This monthly check is how the system stays honest. The first month is pure calibration. The distribution amounts will be wrong. In the Basilone family story that runs through the Millionaire Veteran community, John and Lena set their Lifestyle allocation at $125 per paycheck. By day eleven, the account was at $6.12. Lena had accidentally used the wrong card for groceries. John bought a video game without checking the balance. They had nineteen days until the next paycheck. That was the system working. In the old world, they would have kept spending from the pooled account and not noticed until a bill bounced. The Compass Method made the overspend visible immediately. They adjusted for month two.

By month three, the percentages reflect reality. The monthly check becomes a quick scan rather than a rebuild. But it does not go away. Financial circumstances change. Expenses shift. Income adjusts. New subscriptions appear that nobody actively decided to keep. A credit card that was supposed to be frozen gets used for an emergency and now carries a balance again. The system absorbs all of that, but only if someone looks at it once a month and makes the tweaks. The check is what keeps the system honest over time.

How Military Pay Fits

Military compensation arrives from multiple sources on different schedules. Base pay and BAS are part of the biweekly DFAS deposit. BAH lands on its own schedule. Special pay, incentive pay, and bonuses arrive on their own timelines.

All of it flows into the same income account. The distribution percentages apply to each deposit as it arrives. The biweekly DFAS deposit triggers one distribution. If BAH deposits on a different day, it triggers its own distribution using the same percentages. The dollar amounts are different because the deposit sizes are different, but the percentages remain constant.

Two months per year, biweekly pay produces a third paycheck. The standard month is built on two biweekly deposits, not 2.167 (the annualized average that overstates what actually arrives in 10 of 12 months). The third check is real income. The default is to route it toward the active milestone, but the family decides. Some split it. Some direct it entirely to the milestone. The system handles either choice.

PCS moves change the inputs. BAH adjusts. Cost of living shifts. The allocation percentages may need tweaking, but the account structure stays the same. The accounts do not change. Only the numbers in the distribution adjust.

Deployments shift the numbers in a different way. Income increases from hostile fire pay and family separation allowance. Some personal expenses decrease. The family at home continues spending from the same accounts. The distribution percentages may shift temporarily. The accounts and the rhythm stay the same.

Where Budgeting Fits

Budgeting and cash flow management are two different tools. A budget starts after money is spent: it categorizes transactions, compares them to a plan, and produces a report. A cash flow system starts before money is spent: it distributes money into purpose-specific accounts and lets the balances constrain spending in real time.

Both approaches exist. The difference is in what they demand. A budget requires sustained daily attention: logging, categorizing, reviewing. A cash flow system requires setup effort and a brief distribution on each payday, plus a monthly check to keep allocations calibrated.

Lena Basilone had tried budgeting twice before the Compass Method. A spreadsheet that lasted two weeks. An app that lasted a month. Both times, life happened and tracking stopped. When John brought her the cash flow system, her first reaction was “I’m not doing another budget.” The distinction that changed her mind: the money actually moves. The control is at the bank account level, not in a spreadsheet that falls apart when you stop updating it. A year later, the accounts are still running. No spreadsheet survived a month.

The cash flow system inside the Millionaire Veteran community is called the Compass Method. It takes everything described in this article and turns it into a repeatable structure: six accounts, a distribution rhythm, and a monthly check that keeps the whole thing calibrated. The mechanics you just read are the foundation. The Compass Method is the implementation.

The daily attention model breaks whenever life gets complicated. Deployments, PCS moves, unpredictable schedules, a new kid, a career change. The periodic distribution model survives all of it because the structure does not depend on sustained tracking. For readers who have budgeted successfully for years, a cash flow system may feel unnecessary. For readers who have tried and failed, or who have never tried either approach, the Compass Method is designed to work when life gets in the way.

Next in the Series

Now you understand the mechanics. Part 4: The Compass Method on Military Pay shows you the specific system: six named accounts, the Payday Ritual, Point Accounts for added precision, and what the first three months of running it actually look like.

Join the Community

Millionaire Veteran is a free community where military families learn the Azimuth Framework: Spend Less, Earn More, Invest Smarter. In that order. The Compass Method is the cash flow system inside the Spend Less domain. The full implementation, built on your real numbers with a personal AI advisor, lives inside the community.

The balance is the answer.

About the Author

Joshua Breaux

Retired U.S. Marine

Financial Management Analyst

BS & MBA in Analytics

His family runs on the same systems he teaches here.

This content is educational and does not constitute personalized financial advice. Millionaire Veteran is not affiliated with the Thrift Savings Plan, FRTIB, or the U.S. Government. Past performance does not guarantee future results.