I tried budgets. More than one. They lasted a few days, sometimes a week, occasionally past the next payday before something broke. Categories drifted, transactions stacked up, and by the time I caught up I was reading the spreadsheet like a hostage note from my past self. It did not click until I stopped budgeting and started running a cash flow system. Money got separated by purpose at the bank account level. The bank balance did the tracking instead of a spreadsheet. That is when it worked, for me and for my family.

If you searched for a biweekly budget, you are in the same place I was. The friction is real. You get paid twice a month, but the bills do not split half and half. Some months one paycheck has more bills than the other. Some months a renewal hits early and tips the math. That mismatch is not in your head.

One technical note: military pay is semi-monthly (the 1st and the 15th), not biweekly. The cadence is close enough that the friction feels the same, and “biweekly” is the search term most people use, so I am going to use it the way you do. For dual-income households where a spouse is on a true biweekly civilian schedule, the mechanics in this article still work.

Here is what the biweekly budget can do, and where it stops.

The Real Problem Isn’t the Timing. It’s the Visibility.

The biweekly mismatch is real, but it is not the deepest layer of what is going wrong. Move all the bills around between the two paychecks however you want; you can build a 12-tab spreadsheet that tells you which check funds which line item. The structural problem stays.

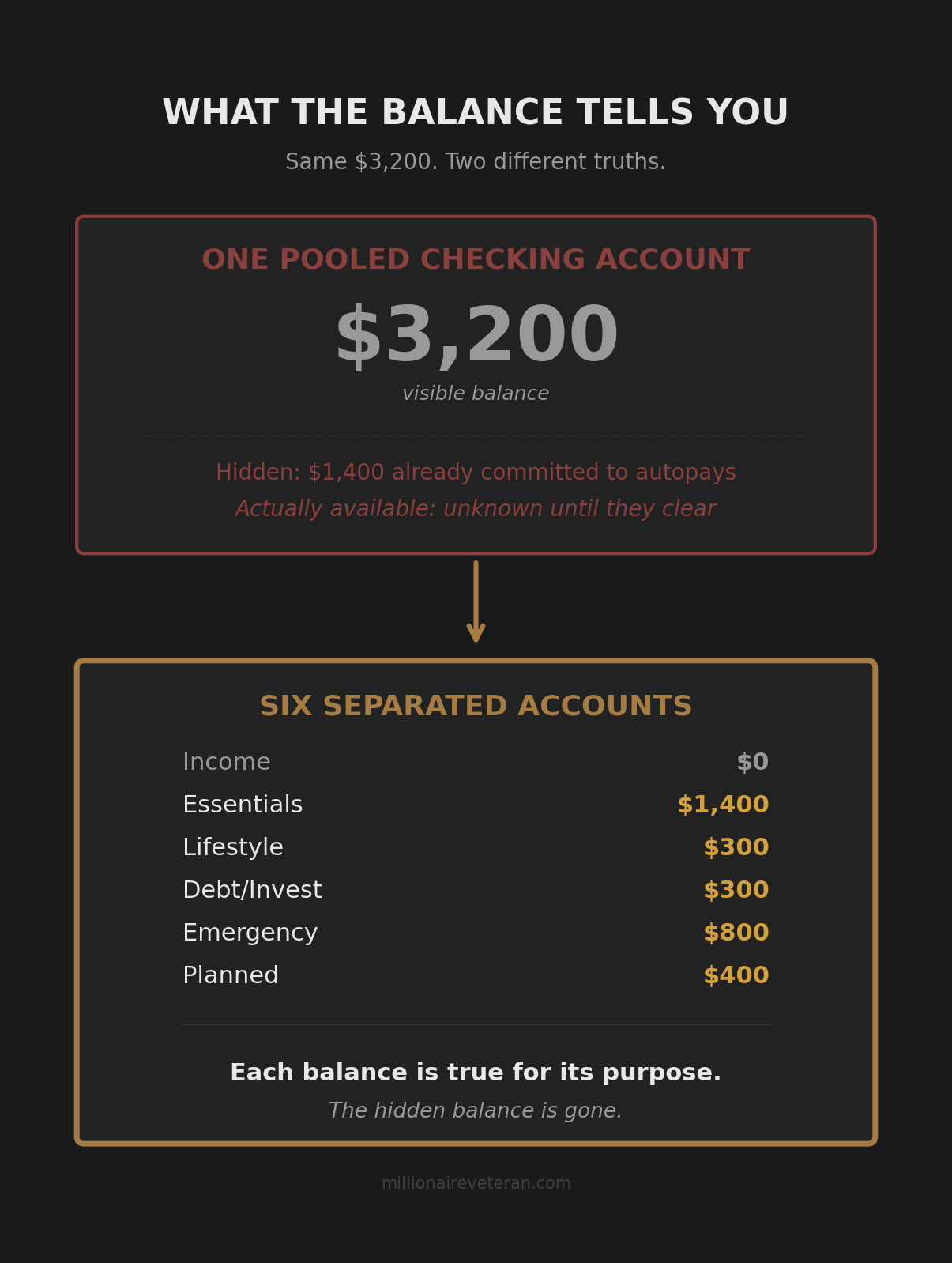

Here is the deeper layer. When every dollar runs through one pooled checking account, the balance you see is not the balance you have. Half of it is already promised to autopays that have not drafted yet, to the credit card payment that posts next week, to the cell bill that runs on the 7th. Until those line items hit the account, the number on the screen overstates what is actually available. By the time the deductions have all cleared, the next paycheck has already landed and the cycle repeats.

A biweekly budget tries to fix this by splitting bills between paychecks on paper. The paper plan is fine. The bank account does not know about it. When you stand in line at the grocery store and the app shows $1,800 in the checking account, the budget says “but $1,400 of that is committed before next payday.” Now you are doing math against an invisible plan, in real time, with stale data.

The cadence is just where the failure shows up first. Weekly, biweekly, semi-monthly, monthly, it does not matter. Any household running money through one pooled checking account is dealing with the same visibility problem. Military families happen to feel it on a semi-monthly cadence with a few additional moving pieces, but the failure pattern itself is universal. It shows up in commission-only households, freelancer households, dual-income households where two pay cycles overlap. The pooled account lies to everybody.

That is what no biweekly budget can solve, and what the rest of this article is about fixing.

What a Biweekly Budget Solves (And What It Still Can’t Touch)

A biweekly budget gets one thing right. It anchors planning to when money actually arrives, not to a generic monthly number. That is closer to reality than pretending one paycheck shows up a month. The instinct to align planning with deposit timing is correct.

Two things it still cannot touch.

First, the balance still lies. The biweekly split lives on paper or in an app, but the bank account is one balance, and that balance includes money already promised to autopays that have not drafted. The number on the screen is wrong by hundreds or thousands of dollars depending on where you are in the cycle.

Second, the categorization work does not go away. Every transaction still has to be tagged after the fact: was this groceries or household, was this personal or family spending, did the right line on the spreadsheet cover it. Twenty transactions a week is twenty decisions before the data is even useful. By week two most people are behind. By week four the categories are guesses, and the spreadsheet is a story you tell yourself.

None of this is a discipline problem. The reader doing all of the above is doing the right things with the wrong tool. A budget is a backward-looking measurement device trying to do a forward-looking allocation job. The tool category is the issue, and a smarter biweekly version of the same tool runs into the same wall.

This article focuses on the biweekly cadence. The broader version of the same reframe (budgets fail because of their architecture, not the reader’s discipline) is the subject of how to stop living paycheck to paycheck on military pay.

50/30/20 With Three Bank Accounts Gets Closer

50/30/20 is one of the more common frameworks people land on after the biweekly budget fails: take 50 percent of take-home pay for needs, 30 percent for wants, 20 percent for saving and debt. The math is forward-looking and percentage-based. You commit to the splits up front and live inside them.

If 50/30/20 lives only in your head, it runs into the same wall as the biweekly budget. You still have one checking account with one balance. The splits exist on paper while the money sits in a pool, and the point of purchase still requires math against an invisible plan.

But 50/30/20 can be run with three bank accounts: a Needs account, a Wants account, and a Save/Debt account. Set up that way, the principle starts working. Each account’s balance tells you the truth for its purpose. Pay hits, the splits route by percentage, and you are no longer doing math against a lying balance.

That setup is genuinely closer to the answer. The reason it stops short is granularity. Three buckets cover broad territory.

The “Wants” bucket lumps personal coffee with the family vacation fund with replacing the washing machine when it dies. None of those are the same thing, and none of them should share a balance.

The “Save/Debt” bucket lumps emergency cash with retirement investing with attacking a credit card. The behaviors and the priority order for each are different, and lumping them together hides that order. Most households have a sequence: build a buffer, attack high-interest debt, fund retirement, fund larger goals. One account does not show you the sequence.

The “Needs vs Wants” line is also fuzzy. Is the gym a need? The family streaming bundle? Pet insurance? The decision is judgment, and judgment in real time at a checkout is exactly where budgets fail.

50/30/20 with three accounts is the right direction. It stops one move short of the granularity that handles real life.

Where the Compass Method Picks It Up

The Compass Method is a cash flow management system. It runs the same separation principle as 50/30/20 with three accounts, but takes the granularity to the level real households actually need.

Six accounts at the bank, structured so each one serves one purpose:

- Income: everything you earn lands here. Pure routing. No spending happens from this account.

- Essentials: the must-pay obligations. Rent, utilities, insurance, debt minimums, anything where non-payment causes eviction, repossession, shutoff, or collections.

- Lifestyle: discretionary spending. Personal, dining, entertainment, anything optional. When this account is empty, discretionary spending stops until next payday. That is the system working.

- Debt/Invest: above-minimum debt payoff while you are attacking debt, investment funding once the debt attack is over. No debit card on this one. Money leaves only through intentional transfers.

- Emergency: the actual unexpected, like a transmission failure, an urgent vet bill, a sudden flight home. Conscious access only. Not raided for lifestyle shortfalls.

- Planned: known future spending that exceeds one month. Holiday gifts, vacation, the next vehicle. Funded in advance so the spending does not blow up the month it arrives.

The Essential vs Lifestyle test is binary. One question: “If I stopped paying this, would something break?” Break means eviction, repossession, shutoff, collections, legal consequence. Not “life gets harder,” not “the kids are disappointed.” The gym is not essential. The streaming bundle is not essential. The mortgage is. The car payment is. The clarity replaces the fuzzy “needs vs wants” call.

Within those six, what are called Point Accounts add precision when an account is too broad. Essentials usually splits into a Fixed account (autopay bills, no debit card) and a Variable account (groceries, gas, household supplies, with its own debit card). Lifestyle for couples typically splits into personal accounts per spouse plus a family shared account, so the conversation about who spent what stops happening.

Allocation is percentage-based and calibrated over time, not locked once. The first month is calibration: you commit to a forward target, then adjust based on what actually shows up. While attacking high-interest debt, the Debt/Invest account gets the share that would later go to investing. Once that debt is cleared, the same account redirects to investments. The percentages move with the phase.

The math fits semi-monthly military pay cleanly. Two deposits a month, the same percentage applied to each, no annualizing and dividing by twelve. If one of those deposits is a different size (special pay, a small differential), the same percentages still apply.

What stays the same with this system. Every spending decision is still yours. If the Lifestyle account is at $87 today and a family meal is planned for Friday, you are still the one deciding whether the coffee today or the dinner Friday gets that money. The Compass Method does not remove the decision. It removes the lying balance underneath the decision.

What changes. The number you see for each purpose is true. Essentials are funded before anything else moves. Emergency money is not accidentally in the same pile as lifestyle. The allocation was decided up front, in calm, with the full picture in front of you, and gets recalibrated monthly at a structured check-in instead of fought at the checkout line.

What This Does to the Biweekly Question

Once money is separated by purpose at the bank level, which paycheck pays for what stops being a question. Essentials gets the same percentage of every deposit. Rent comes out of Essentials. Whether the funding shows up via the 1st check, the 15th check, or both, the math is the same because the percentages are the same.

Lifestyle works the same. Emergency works the same. Planned works the same. Every deposit triggers a routing, the routing is identical each time, and the accounts hold the right balances by purpose between paydays.

For dual-income households where one paycheck is biweekly and another is semi-monthly, both deposits trigger their own routing. Same percentages, different dollar amounts because the deposit sizes differ. The system scales without recalculating the plan.

The friction the biweekly budget was trying to solve (that the bills do not split half and half) gets dissolved by a different category of fix. The fix is not better timing. The fix is bank-account-level separation that makes the timing irrelevant.

Your Next Step

For the full diagnosis of why one pooled checking account lies to every household, the front-door article in this series covers it at single, couple, and family scale: Where Does My Money Go: The Question Every Military Family Eventually Asks.

For a closer look at what a cash flow system does at the mechanical level, and where it actually differs from budgeting, this one goes deeper: What a Cash Flow System Actually Does.

Join the free community

When you are ready to build the structure with your real numbers (your actual semi-monthly pay, your bills, your milestone, whatever income variability your household has) that happens inside the Millionaire Veteran free community. The Diagnostic Review walks you through it, and an AI advisor calibrates the percentages with your numbers. Not a template you will quit in three weeks.

About the Author

Joshua Breaux

Retired U.S. Marine

Financial Management Analyst

BS & MBA in Analytics

His family runs on the same systems he teaches here.

This content is educational and does not constitute personalized financial advice. Millionaire Veteran is not affiliated with the Thrift Savings Plan, FRTIB, or the U.S. Government. Past performance does not guarantee future results.