Most “TSP withdrawal rules” content covers one specific flavor. One article on hardship withdrawals. Another on the lump sum. A third on rolling the balance to an IRA. The reader looking for the full picture has to piece it together from three sources that do not agree on the framing and rarely tell you which option applies to which situation.

This article does the other thing. It lays out all five withdrawal categories in one place, the penalty gate that sits across most of them, and the structural variables that determine which option fits which reader. It is a map, not a recommendation.

Here is the structure of the map. First, the five categories of TSP withdrawal so the full picture is clear before the details. Second, the 10% early withdrawal penalty and the exceptions that override it, because that one rule shapes most of the decision space. Third, the in-service options available while you are still working. Fourth, the post-separation options that open up after you leave federal or military service. Fifth, the Required Minimum Distribution rule that turns on later in retirement. Sixth, the place where the rules end and the personal choice begins.

All figures in this article are current as of 2026 and reflect the SECURE 2.0 Act provisions in effect this year. Withdrawal rules change with legislation. Verify against IRS Publication 590-B and TSP.gov before acting on anything below.

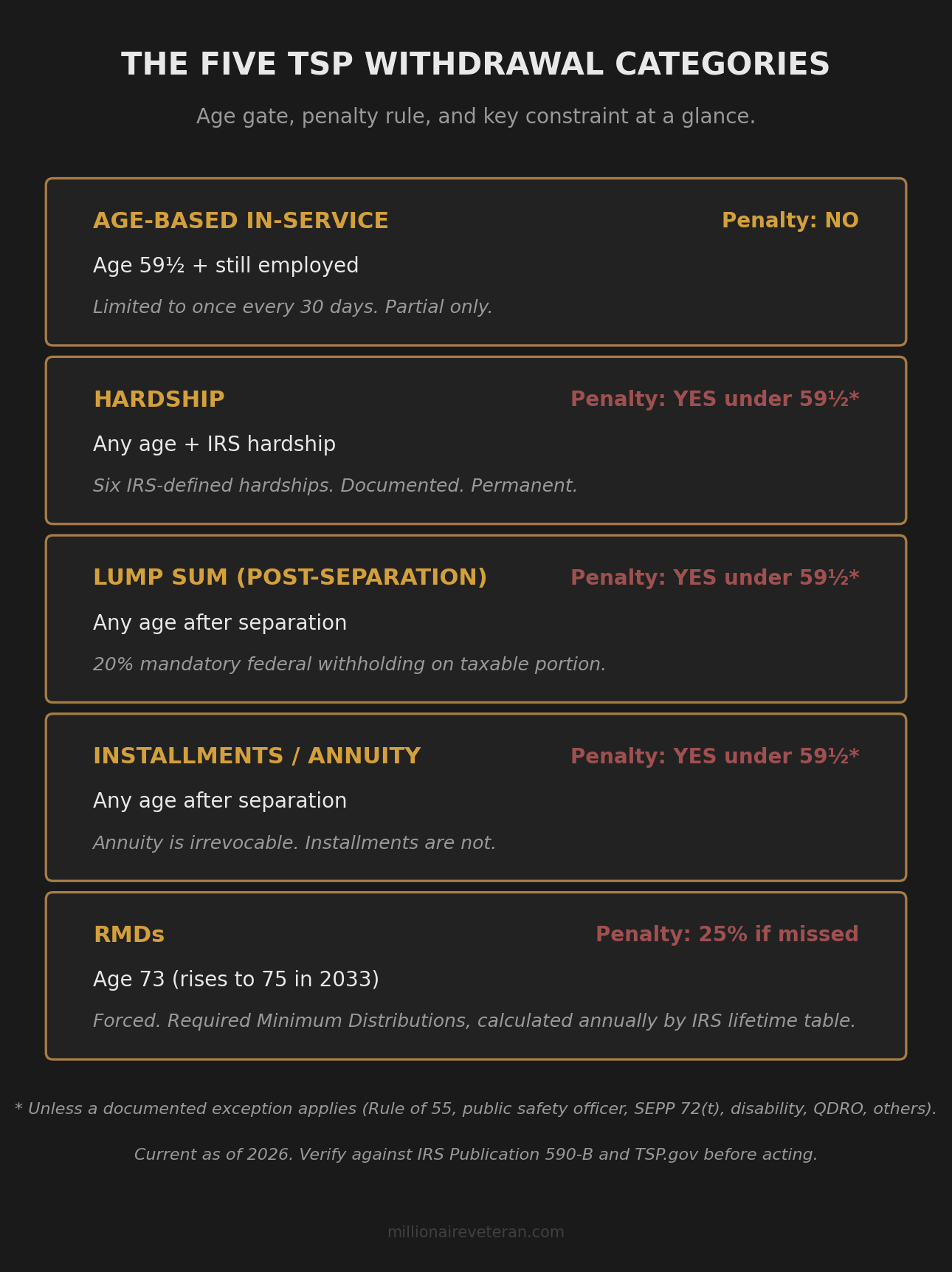

The Five Categories of TSP Withdrawal

The Thrift Savings Plan (TSP) is administered by the Federal Retirement Thrift Investment Board (FRTIB) under rules set by Congress and the IRS. Withdrawals fall into five categories, organized by when in your career the option becomes available.

In-service age-based withdrawal. Available at age 59½ while you are still federally employed, active-duty, or guard/reserve. Penalty-free because of the age. Lets you access part of the balance before separation.

Hardship withdrawal. Available at any age while still employed if one of the IRS-defined hardship categories applies. Subject to the 10% early withdrawal penalty if you are under 59½ unless another exception applies. The hardship must be documented.

Post-separation withdrawals. Available after you leave federal or military service. Four sub-options: single payment, installments, life annuity, or transfer/rollover to an IRA or other qualified plan.

Required Minimum Distributions (RMDs). Forced distributions that turn on at age 73 under current SECURE 2.0 rules, rising to age 75 for those who turn 74 after 2032. Applies to any balance still inside the TSP at that age.

A note on what is not on this list. The TSP loan program is a separate mechanism. Loans are repaid; withdrawals are not. Loans are not withdrawals, and the rules below do not apply to them. Loans get their own article when that gets written.

The Penalty Gate: The 10% Early Withdrawal Penalty

The single biggest rule across TSP withdrawals is the 10% early withdrawal penalty under Internal Revenue Code section 72(t). The default: any distribution from a tax-deferred retirement account before age 59½ is hit with a 10% federal penalty on top of regular income tax on the distribution.

A concrete example shows why the penalty matters. A separating service member at age 50 takes a $50,000 lump sum from a Traditional TSP balance, no exception applies, and the household is in the 22% federal income tax bracket. The math runs: $5,000 penalty plus $11,000 federal income tax plus state income tax where applicable. Before state tax, that $50,000 distribution delivers about $34,000 to the household checking account. The penalty alone took 10% off the top of an already-taxed withdrawal.

There are documented exceptions that allow penalty-free withdrawals before age 59½. The ones that matter most for TSP participants:

The Rule of 55. If you separate from federal or military service in the year you turn 55 or any year after, withdrawals from that employer’s TSP are penalty-free. The rule applies to the TSP specifically, not to an IRA rollover. If you roll the balance to an IRA first and then withdraw, the Rule of 55 does not protect you.

The age-50 public safety officer exception. Qualifying public safety officers who separate in or after the year they turn 50, or with 25 years of qualifying service (whichever comes first under SECURE 2.0), get penalty-free access to the TSP.

Substantially equal periodic payments (SEPP) under section 72(t). A formula-based stream of payments, set up before age 59½ and continuing for at least five years or until age 59½ (whichever is later). Rigid. The IRS-allowed calculation methods are tightly constrained, and breaking the schedule retroactively assesses the penalty on all earlier withdrawals.

Disability, qualified domestic relations orders (QDRO), birth or adoption distributions up to $5,000, and terminal illness. Each has its own documentation rules and limits.

The exception is the difference between $34,000 in hand and $39,000 in hand on the example above. Whether an exception applies is usually the first thing to check before any early withdrawal decision gets serious.

In-Service Withdrawals (While You Are Still In)

Two in-service options exist. They serve different situations.

Age-based in-service withdrawal. At 59½ and still employed, you can take partial withdrawals from your TSP balance without separating from service. The age threshold makes it penalty-free. Income tax still applies to Traditional balances. Roth TSP withdrawals follow the Roth qualified-distribution rules, which require both the 59½ age and a five-year holding period on the Roth account itself. The mechanism is useful for active-duty members serving past 59½ and for federal civilians who want partial access before retirement without disrupting employment.

Hardship withdrawal. Available at any age while still employed if one of the IRS-recognized hardships applies. The current list covers six categories: certain medical expenses, costs related to purchasing a principal residence, prevention of eviction or foreclosure on a principal residence, qualifying higher education expenses, funeral and burial expenses, and repairs to a principal residence that qualify under the casualty deduction rules. Each category has its own documentation requirements.

The hardship withdrawal is a withdrawal, not a loan. The balance leaves and does not return. The 10% early withdrawal penalty applies if you are under 59½ and no other exception covers the situation. Federal income tax applies on the taxable portion. Most readers thinking about a hardship withdrawal underweight the third cost: the compounding lost on the dollars that left the account. A $20,000 hardship withdrawal at age 35 is not a $20,000 reduction at retirement. At a 7% real return for 30 years, the same dollars left invested would have been worth roughly $152,000 at age 65. The penalty and the income tax are visible. The compounding loss is invisible and usually the largest cost.

The strategic decision about whether to take a hardship withdrawal is its own conversation. This article covers the rule that defines the option, not the decision about whether to use it.

Post-Separation Withdrawals (After You Are Out)

Once you separate from federal or military service, four post-separation options open up. They can be combined within FRTIB rules.

Single payment. A lump-sum distribution of part or all of your balance. The TSP applies a mandatory 20% federal income tax withholding on the taxable portion (Traditional balances and any earnings on Roth contributions that do not meet qualified-distribution rules). The 20% is withholding, not the final tax. The actual tax owed depends on the rest of your income that year. The 10% early withdrawal penalty applies if you are under 59½ unless an exception applies. The Rule of 55 commonly applies for service members who separate in or after the year they turn 55.

Installments. Scheduled distributions: monthly, quarterly, or annual. You can specify a dollar amount or have the TSP calculate based on IRS life expectancy tables. Installments smooth income across tax years and can reduce the year-by-year tax burden for retirees with no other income. Penalty rules still apply to installment payments taken before 59½ unless an exception applies.

Life annuity. The FRTIB partners with an annuity provider to convert part or all of your balance into a stream of payments guaranteed for life. The trade is flexibility for certainty. Once the annuity contract is purchased, the decision is irrevocable. The annuity income is fixed at purchase and does not benefit from future market gains. Useful for participants who want a portion of retirement income hedged against longevity risk and against their own sequencing decisions.

Transfer or rollover to an IRA or other qualified plan. A direct rollover sends the balance to a Traditional IRA, Roth IRA (for Roth TSP balances), or another employer plan that accepts rollovers. A direct rollover avoids the 20% mandatory withholding and avoids the early withdrawal penalty even if you are under 59½, because no distribution to you ever occurs. The rollover trades the TSP’s expense ratios for whatever expense ratios the receiving account carries. The TSP is one of the lowest-cost retirement plans in the country, and rolling out usually means paying more in fund expenses. The rollover also opens up the full range of investment options, which is the other half of the trade.

Each post-separation option carries its own tax and penalty consequences. None of the four is universally best. The right choice depends on age at separation, other income sources, pension status under the Blended Retirement System or the legacy High-3 system, marital and beneficiary considerations, and the structural Roth or Traditional split inside the existing TSP balance.

Required Minimum Distributions

The RMD rule turns on at age 73 under current SECURE 2.0 provisions for participants born between 1951 and 1959. Participants born in 1960 or later see the threshold rise to age 75, with the new threshold first taking effect starting in 2033. RMDs apply to any TSP balance still inside the plan at that age.

The annual RMD amount is calculated by the IRS Uniform Lifetime Table: divide the prior-year-end account balance by the table factor for the participant’s age. As a rough illustration, the Uniform Lifetime divisor at age 73 sits around 26.5, which puts the first-year RMD at roughly 3.8% of the balance. The factor drops as the participant ages, which means the RMD percentage of the remaining balance climbs each year. The TSP calculates the figure automatically and distributes it on schedule unless the participant takes it manually first. Missing an RMD triggers a 25% excise tax on the missed amount, reduced from the pre-SECURE 2.0 figure of 50%, and the excise tax can drop to 10% if the missed RMD is taken and reported promptly under SECURE 2.0 correction rules.

One Roth-specific note matters here. Roth TSP balances are subject to RMDs while inside the TSP, even though Roth IRAs are not. A rollover of Roth TSP balances into a Roth IRA before RMD age removes the Roth balance from the RMD calculation entirely. That one move changes the math on forced distributions for the rest of retirement, and it is downstream of contribution-stage choices that decide which dollars get Roth treatment in the first place.

The Rules Are Knowable; The Choice Is Personal

Everything above is the rule. The rules are the same for every participant. What varies is the situation each participant brings to the rules.

A service member separating at age 42 with twenty years of service, a Blended Retirement System pension, an active-duty spouse still earning, no inefficient debt, and a Traditional-heavy TSP balance faces a different post-separation calculus than a civilian federal employee separating at age 62 with no pension, a spouse who has already retired, and a Roth-heavy balance built across the last decade. Both readers have the same rules above them. The choice each makes is downstream of structural decisions that were made years before the withdrawal window opens.

The rules are knowable; the choice is personal.

The structural decisions that govern the choice show up most clearly in the Roth versus Traditional split inside the existing balance. The split between the Roth and Traditional foundation that governs every withdrawal decision determines which dollars come out tax-free decades later and which dollars come out as ordinary income. That structural choice, made during the contribution years, shapes every withdrawal decision listed above.

The second decision that shapes the withdrawal stage is sequencing. The first five to ten years of withdrawals run into a market risk that participants in the accumulation phase rarely think about. A bad return sequence early in retirement can permanently impair the account even if the long-run average return is fine. The article on the two TSP risks your BRS briefing never covered walks through the sequence-of-returns angle in depth and is the right next stop for any reader thinking about withdrawal timing.

Both structural decisions live upstream of the rules. The rules tell you what is allowed. The structure determines what is wise.

Plan Your Withdrawals With Your Real Numbers

The Firewatch Blueprint walks through the structural framework that determines which TSP withdrawal options actually fit a participant’s situation. Not a withdrawal recommendation. The framework that lets you see how your contribution stack, your Roth and Traditional split, your timeline to separation, and your pension status interact with the rules above before the withdrawal decision is in front of you.

Get the Blueprint to see the framework before you need to use it. Free. Delivered to your inbox.

About the Author

Joshua Breaux

Retired U.S. Marine

Financial Management Analyst

BS & MBA in Analytics

His family runs on the same systems he teaches here.

This content is educational and does not constitute personalized financial advice. Millionaire Veteran is not affiliated with the Thrift Savings Plan, FRTIB, or the U.S. Government. Past performance does not guarantee future results.