Most “zero based budget pros and cons” articles are sales pitches for whatever the writer wants you to use next. The pros are listed lightly, the cons are listed harshly, and the bottom of the page nudges you toward the alternative. That is not what this is.

I have run zero-based budgeting. I have watched other people run it. I have watched it work for some of them and quietly fall apart for most. The pros are real. The cons are real. Both deserve to be on the page without one being weighted to win the argument.

Here is the structure of the evaluator. First, the actual definition of the method, because the word “budget” has been worn out enough that it is worth saying clearly what zero-based budgeting is. Second, the real pros, named honestly and not undercut. Third, the real cons, named honestly and not exaggerated. Fourth, the thing the pros and the cons have in common, because once you see what they share, the choice gets easier. Fifth, the structural alternative that keeps the principle and removes the maintenance cost. Sixth, a clean read on who should pick which.

If you are evaluating zero-based budgeting before you commit to it, you should leave with a clear picture of who the method serves. If you have already tried it and it broke, you should leave knowing whether that was you or the mechanism. Both readers deserve an answer.

What Zero-Based Budgeting Actually Is

Zero-based budgeting (ZBB) is a method where every dollar of income gets assigned a job before the month begins. Income minus all the categories equals zero. Nothing is left unassigned. Nothing is allowed to drift.

The original idea came out of corporate accounting in the 1970s, where it was used by managers who had to justify every line of a department budget from scratch each cycle instead of starting from last year’s number. Personal finance picked it up later. Dave Ramsey taught a version of it inside his Baby Steps framework, and YNAB built a software business around a more flexible version of the same logic. Different presentations, same principle.

Operationally, the method has four moving parts. You build a plan before the month starts. You assign every dollar of income to a category until the math reaches zero. You track every transaction through the month and categorize it against the plan. At month-end you reconcile, see where you drifted, and rebuild the plan for next month with what you learned.

That fourth step is what makes it “zero-based” and not just budgeting. You do not roll last month’s plan forward. You build the next month from a blank page. That rebuild is the discipline. It forces you to look at every category every month and decide whether the assignment still fits.

The reader who searched “zero based budget pros and cons” usually wants three things: a clean definition, a fair evaluation, and a recommendation they can act on. The definition is above. The evaluation is next.

The Pros of Zero-Based Budgeting (Honest)

There are three pros worth naming. None of them are filler. If you are the right reader for the method, these pros carry real weight.

It forces awareness. You cannot run zero-based budgeting without seeing where every dollar goes. For someone who has never tracked spending closely, the first thirty days of the method are genuinely educational. You will discover subscriptions you forgot about, categories that are double what you thought they were, and patterns you would never have noticed without the categorization work. That awareness alone changes behavior, even in people who eventually drop the method.

Every dollar gets assigned. No drift. No “where did $400 go this month?” The plan is explicit before the spending happens. When you stay current with the categorization, the plan is the truth and the truth is auditable. The household that runs zero-based budgeting well does not have arguments about money in the abstract. Both adults can open the same plan and see the same numbers. Done well, that ends the argument.

It surfaces leaks. Recurring charges that crept in, the streaming service nobody watches anymore, the gym membership that has not been used in eight months, the convenience-store snack run that is quietly $180 a month. Zero-based budgeting exposes all of it because nothing is invisible inside the method. You cannot have a category that runs over without seeing it run over. Exposure forces a decision.

These are real strengths. Do not let the cons section overshadow them. People who run zero-based budgeting consistently and well develop a fluent relationship with their money that most adults never reach. They know which categories are fixed and which are flexible. They know which months will be tight and why. They know what an unexpected $500 expense actually displaces, because the rest of the plan is already accounted for. That fluency is the byproduct of doing the work, and the work is the method. That cost is what the next section covers.

The Cons of Zero-Based Budgeting (Honest)

Three cons, each one structural rather than personal. The method has built-in costs. They are not failures of effort. They are properties of the design.

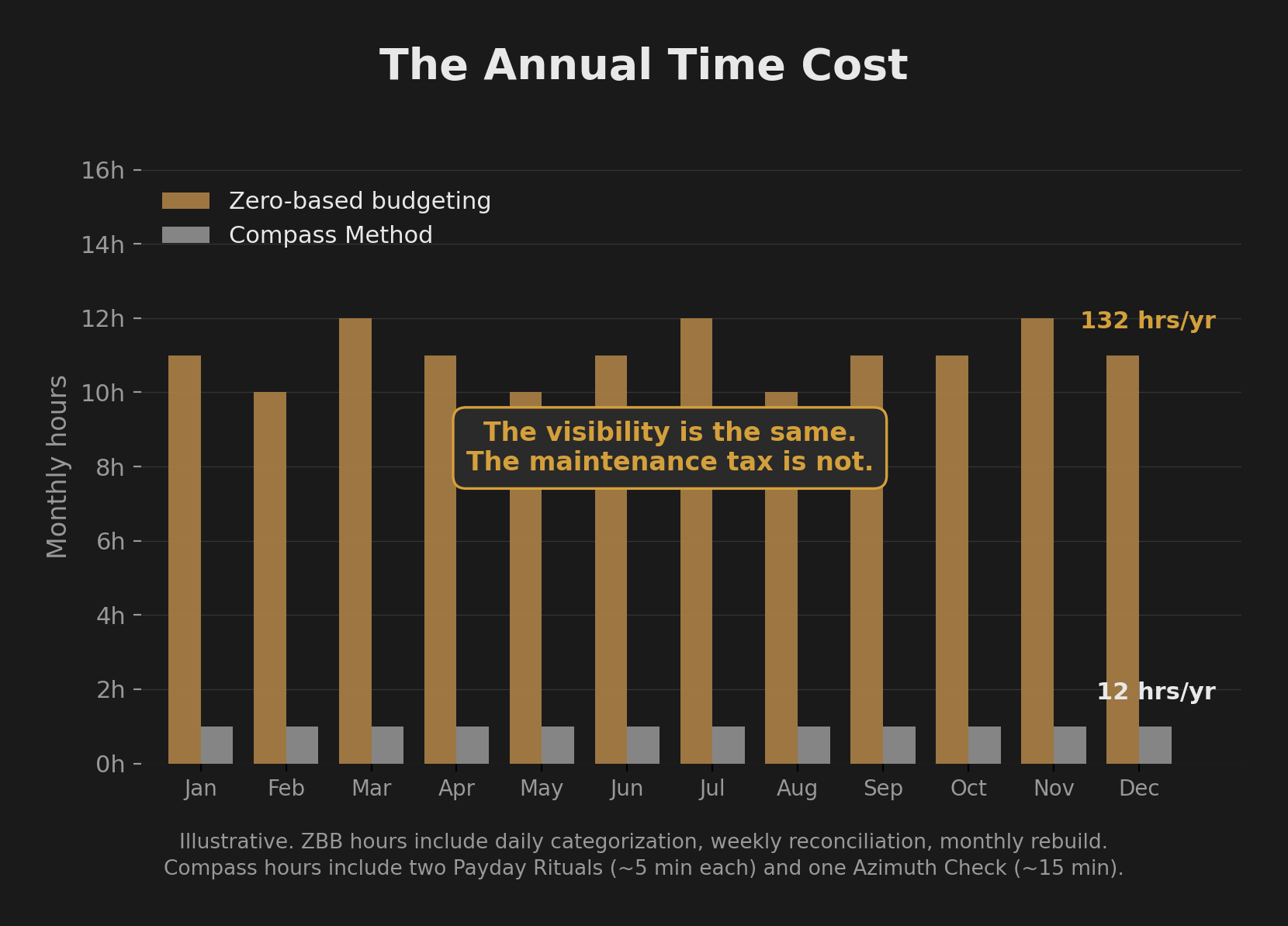

High monthly maintenance. Categorization is daily. Reconciliation is weekly or monthly. The rebuild for the next month is monthly. In my experience running the method, a household keeping up with it well logs several hours a month in categorization and rebuilds alone. That cost compounds when you fall behind. Skip three days and you come back to thirty transactions waiting to be categorized. Skip a week and the backlog feels like a chore instead of a habit. Most attempts die in the third or fourth week, when life gets busy and the catch-up curve gets steep.

Brittle under operational disruption. Any week that pulls you off your daily rhythm puts pressure on the method. For military families, that includes field exercises, TDY rotations, watch standing, and deployment cycles. For everyone else, it includes travel weeks, caregiving stretches, sick weeks, family emergencies, and the normal months where the calendar gets ahead of you. The method assumes you will be available to sit down with the categorization every day or two. When that assumption breaks for ten days in a row, the backlog hits a size where most people stop opening the app. The structural failure point is not motivation. It is the gap between the cadence the method requires and the cadence your life actually delivers.

It does not separate the money. This is the quietest of the three cons and the most consequential. Under zero-based budgeting, all the dollars sit in the same checking account. The “category” is conceptual. It lives on a spreadsheet or inside an app. The dollars assigned to groceries and the dollars assigned to the car payment are mixed together in the same pile, and the only thing keeping them apart is the line item on the screen and your willpower at the register. The plan is visible. The plan is not structural. That distinction matters more than it sounds, because when willpower has to enforce a boundary that the bank account does not enforce, the boundary leaks at the edges. Always.

The pattern across those three connects.

The Pros and Cons All Trace to the Same Thing

Look at the list again. The pros are awareness, assignment, and leak surfacing. The cons are maintenance load, brittleness, and the lack of physical separation. The pros and the cons all trace to the medium.

The medium of zero-based budgeting is a spreadsheet or an app, plus your memory and discipline at the point of purchase. That medium is what produces the awareness, because everything has to be entered to be tracked. That same medium is what produces the maintenance load, because every transaction needs categorization. The medium is what produces the visibility, because the plan is laid out where you can see it. The medium is what produces the brittleness, because the moment you stop entering transactions, the plan stops reflecting reality.

The pros are real; the cons all trace to the medium.

If the pros and the cons share a root, then changing the root changes both columns at once. You do not have to give up the principle of “every dollar assigned” to escape the maintenance tax. You only have to change where the assignment lives. If the assignment lives on a spreadsheet that you have to maintain, you pay the maintenance tax. If the assignment lives at the bank, in actual separate accounts holding actual separate dollars, the tax disappears and the principle survives.

That is the move. Same principle, different medium. The cash flow system that does this is the Compass Method, and the structural cash flow problem it solves gets the full walkthrough over there. The next section here gives you the shape of the alternative so you can compare the two side by side.

The Compass Method: Same Principle, Different Medium

The Compass Method is a cash flow system that runs on six bank accounts instead of one. Four checking, two savings. Each account has a single purpose. The structure looks like this:

- Income (IN): All income lands here. Pass-through only. No spending. No autopays attached.

- Essentials (ES): Must-pay obligations. Rent, utilities, insurance, debt minimums, anything where non-payment causes eviction, shutoff, repossession, or legal consequence.

- Lifestyle (LS): Discretionary spending. When this account is empty, discretionary spending stops until the next payday. That is the system working.

- Debt/Invest (DI): Above-minimum debt payoff first, then investment funding once inefficient debt is gone. No debit card attached.

- Emergency (EM): Buffer against the unexpected. Conscious access only. Moving money out of this account requires a deliberate decision.

- Planned (PL): Known future spending that exceeds one month. Gifts, vacation, vehicle down payment.

On payday, you run the Payday Ritual. You transfer pre-decided percentages of that deposit from Income to each of the other five accounts. Income hits zero. Every dollar is now physically sitting in its assigned account. The ritual takes about five minutes once you have done it a few times. There is no categorization, because the dollars already moved to the right place. The balance in each account is the truth.

The maintenance picture is different in a structural way, not a marginal one. No daily categorization, because there is nothing to categorize. The dollar that left Lifestyle to buy lunch is gone from the Lifestyle balance, and that balance is what tells you how much discretionary spending is left until the next payday. No monthly rebuild. The allocation percentages do drift over time as spending becomes clearer or income and lifestyle change, but those adjustments happen during the monthly Azimuth Check rather than as a full plan rebuild, and the dollar amounts scale automatically with the size of each deposit in between. No backlog when life takes you offline for two weeks, because the accounts hold their state on their own. Come back, run the next Payday Ritual, resume normal.

The same principle that zero-based budgeting got right (“every dollar assigned”) is preserved. What changed is when the assignment happens and where the assignment lives: once per payday, at the bank, in advance, instead of after every transaction, on a spreadsheet, in arrears. That is what it means to say ZBB looks backward; the Compass Method looks forward.

If you want the full walkthrough of what a cash flow system actually does once it is running, that pillar covers the operating rules in depth.

Which One Should You Pick

Three reader profiles. Match yourself honestly.

You are meticulous, detail-loving, and have a long history of holding daily habits. You actually enjoy the reconciliation work. You like opening a budget app in the evening and getting the categories right. The maintenance is not a cost for you, because it is something you would do anyway. Zero-based budgeting will serve you well. Pick it. Run it cleanly. Do not let anyone talk you out of a method that fits your wiring.

Your life rhythm is variable, your weeks get disrupted by operational demands, and you have a pattern of starting strong on budgeting tools and dropping them in week three or four. The Compass Method is the better structural fit. The medium matches the cadence of your actual life. Five minutes on payday is sustainable across deployments, training cycles, parenting through hard seasons, travel weeks, and the normal months where the calendar runs ahead of you. The cost stays low because the work stays in front.

You have already tried zero-based budgeting and watched it slip. The maintenance tax exceeded the value you got from the visibility. That is a structural mismatch, not a personal one. Move to the Compass Method. The visibility survives at the account-balance level. The tax goes away. You will get back the awareness without the daily desk time.

The honest verdict, then, is that the method depends on the reader. Zero-based budgeting is not bad. It is built for a specific kind of household, and that household exists. Most households are not built that way, and a system that requires daily desk attention from a household that cannot reliably give it is a system that is going to fail. Not because the household is broken. Because the medium does not match.

Pick the medium that matches your life.

Start With the Structural Cash Flow Problem

If the medium is the question, the next layer is the broader cash flow problem the medium has to solve. The pillar article on how to stop living paycheck to paycheck on military pay walks through that bigger picture: why income that looks adequate on paper still fails to build margin, what the actual structural failure points are, and how a working cash flow system addresses them. Read that next if you want the full structural picture before you commit to a medium.

Build Your Cash Flow System With Your Real Numbers

The Compass Method setup inside the free Millionaire Veteran community walks you through the six-account structure using your actual pay grade, your actual take-home, your actual recurring obligations, and your actual debt picture. The AI advisor inside the community calculates the percentages from your real numbers, walks you through the first Payday Ritual, and stays with you through the first month of calibration so the splits hold up when life shows up.

About the Author

Joshua Breaux

Retired U.S. Marine

Financial Management Analyst

BS & MBA in Analytics

His family runs on the same systems he teaches here.

This content is educational and does not constitute personalized financial advice. Millionaire Veteran is not affiliated with the Thrift Savings Plan, FRTIB, or the U.S. Government. Past performance does not guarantee future results.