Most months end the same way. The deposits land, the bills clear, and somehow the balance is gone before the next paycheck. If you have searched “how to stop living paycheck to paycheck” before, you already know the standard advice: build a budget, track every transaction, hold the line at the register. You already know it did not stick.

The problem is structural. The architecture is wrong.

Most paycheck-to-paycheck advice assumes a tool that does not actually fit how money moves through a household. This article is not another budget. We will walk through why budgets break, the three things that actually stop the cycle, and the architecture that makes those three things hold on military pay.

You will need an architecture. Six accounts that decide where your money goes before payday lands, so the rest of the month is mostly just spending what is already there. The setup is real work. The first month is calibration. What goes away after that is the daily categorization and the willpower-at-every-purchase pattern that kills most budgets.

Why Your Budget Keeps Breaking

The dominant advice for stopping the paycheck-to-paycheck cycle is some version of the same instruction: build a budget. Usually that means a zero-based budget where every dollar of income gets assigned to a category before the month begins. Forty categories, sometimes more depending on how granular you go.

Track every purchase. Reconcile the categories. Move money between them when one runs over. Repeat next month.

The problem is not the math. The math works on paper. The problem is the maintenance.

Every transaction needs to be categorized and accounted for. Miss three days because you went on a trip or had a hard week, and you come back to forty uncategorized transactions sitting in the queue. You spend a Saturday afternoon trying to remember which Walmart receipt was for groceries and which was for everything else that ended up in the cart. By the time you have it sorted, two more days of transactions have piled up.

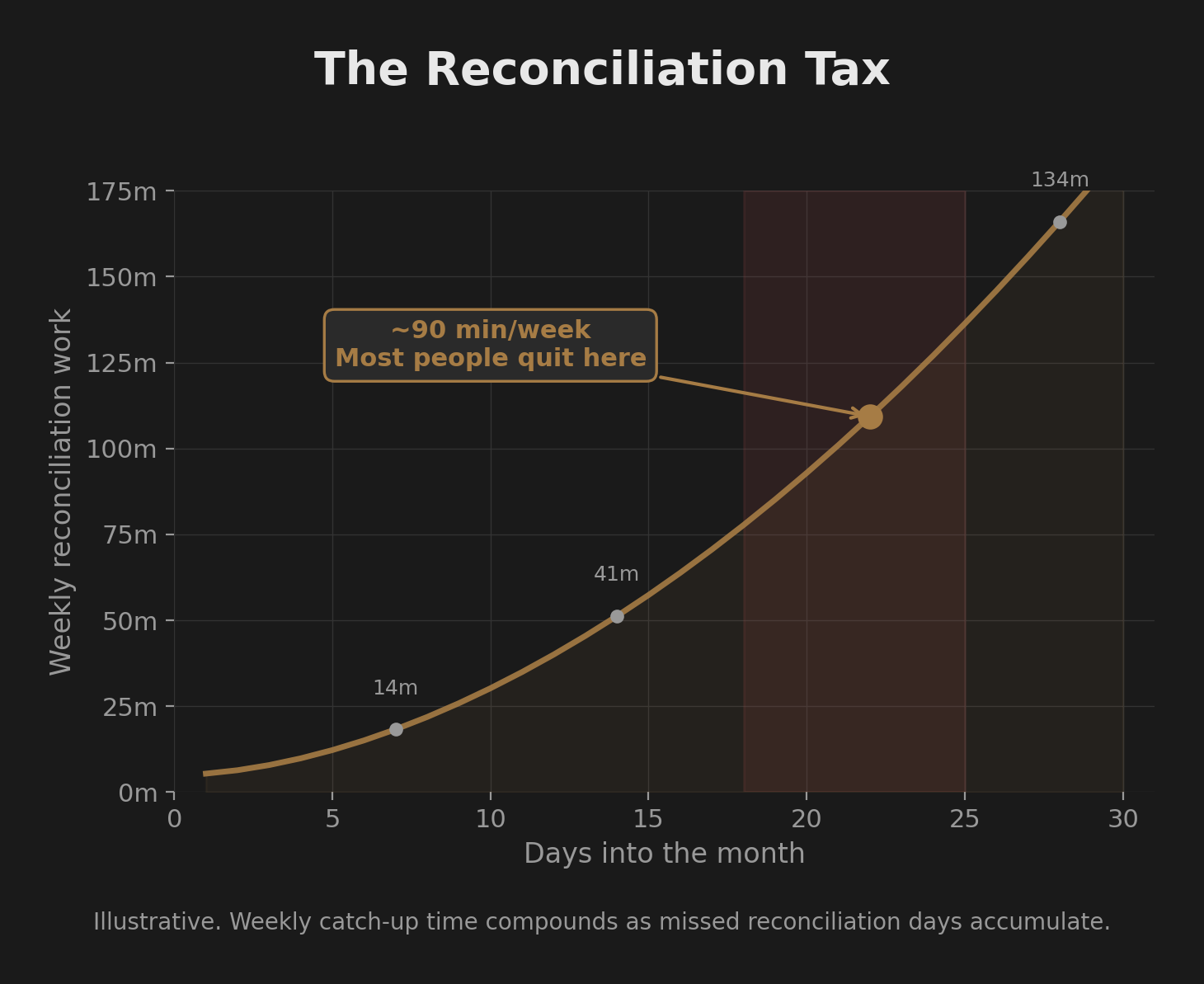

The chart above is the structural failure mode. The line is not “how often you slip.” It is “how much work the system needs to stay current.” That work compounds when you fall behind, and most people quit somewhere between day eighteen and day twenty-five. The tools tell you it is a willpower problem. The tools are wrong. The system requires more discipline to maintain itself than the spending it is supposed to control.

This breaks the same way for everyone whose income is variable: hourly workers with shifting schedules, salespeople on commission, freelancers between contracts, gig workers, and military families with their own particular shapes (BAH that adjusts at every move, BAS that varies by status, reenlistment bonuses and SDP payouts that arrive in lumps, field exercises that take you offline for several days, deployments that reshape income for months). None of this fits the “assign every dollar a job” premise. The premise assumes you know the dollars before they arrive. When you don’t, the model breaks.

One r/MilitaryFinance poster captured it exactly: “I have a budget, but sticking to it seems difficult, I don’t know where the money goes… I haven’t been able to keep an emergency fund because if I can touch it, I’ll take it.” Two halves of the same problem: the budget that does not stick, and the savings that do not stay. These are not lazy people. They are people whose tools failed them.

What 50/30/20 Got Right (And Where It Stops Short)

Not all budgeting advice is wrong. The 50/30/20 rule, popularized in Elizabeth Warren and Amelia Tyagi’s book All Your Worth, has been around for two decades and works better than most alternatives. The rule is simple: half of your after-tax income to needs, thirty percent to wants, twenty percent to savings and debt payoff. No transaction logging. No forty categories. No daily reconciliation.

That instinct is right. Forward-looking allocation by percentage, decided once per pay period, is structurally superior to backward-looking categorization by transaction. 50/30/20 saves people from the reconciliation tax. It scales naturally to variable income because percentages flex with the deposit. A bonus does not blow up the system. A BAH change does not require rebuilding the budget.

But 50/30/20 stops one step short of solving the problem.

The percentages live in your head. The money still lives in one checking account.

Which means at the grocery store, when the total comes out higher than expected, you still have to do the math. Are you over your fifty percent for needs this month? When an unplanned expense lands and the original split has no slot for it, what do you cut? The percentages give you a target. They do not enforce it. Willpower has to enforce it at the point of every transaction, and willpower is the resource that ran out three weeks into your last attempt.

50/30/20 is a real improvement over zero-based budgeting. It is the right shape. It just stops at the threshold of the answer. The next step is to give each percentage its own checking account so the structure does the enforcement, and willpower is no longer the variable. That is what the rest of this article is about.

The Three Things That Actually Stop the Cycle

Three things break the paycheck-to-paycheck cycle when nothing else has. They are not new. They are not secret. They are the things every working budget actually does, stripped down to the parts that matter.

See every dollar before it moves, not after. Backward-looking budgeting tells you what you spent. By the time the categorization is done, the money is already gone. You see the leak after the fact, and you cannot get it back. The shift is to forward-looking visibility: knowing where every dollar is going before it goes there. Not “I spent four hundred on groceries last month.” Instead: “I have four hundred set aside for groceries this month, and the balance is the truth.”

Decide where each dollar goes before payday lands. Most budgeting failures happen at the point of purchase. You are at the register. You are tired. You are doing mental math. You decide the protein is fine because it is just one trip. The decision is happening too late. By the time you are at the register, the money is already in motion. The fix is to decide on payday, once. The percentages flow from the deposit to the places that have already been pre-decided. The decision at the register becomes a balance check, not a willpower test.

Build a structure that survives the next disruption. Life produces disruptions. A move. A deployment. An income drop. A bonus that was not planned. A car repair that was not scheduled. The system has to absorb these without breaking. Most budgets cannot. They were built for a stable month, and stable months are the exception. A structure that survives is one where the disruption changes the dollar amount but not the architecture. The percentages stay constant. The accounts stay the same. The disruption flows through the existing structure.

Architecture, Not Discipline: The Compass Method

The Compass Method is a cash flow management system. It replaces budgeting. It is a different category of tool entirely.

Here is what it actually does. Money is separated by purpose at the bank account level. Not by category. By purpose. Six accounts, four checking and two savings, each one with a single job. When income arrives, you transfer pre-decided percentages from the Income account to each of the others. This is the Payday Ritual: a manual transfer on each payday into accounts you’ve already designated. After that, every dollar is sitting in the right place.

The accounts are Income, Essentials, Lifestyle, Debt/Invest, Emergency, and Planned. Income is the entry point: every paycheck, every bonus, every reimbursement lands here first. Essentials covers the obligations whose non-payment would cause real consequences (rent, utilities, insurance, debt minimums). Lifestyle is everything discretionary. Debt/Invest carries above-minimum debt payoff during the early stages, then becomes investment funding once the inefficient debt is gone. Emergency is the buffer against the unexpected. Planned holds known future costs that do not fit a single month, like gifts, vacation, or a vehicle replacement.

The system does not require categorizing every transaction. It does not require weekly reconciliation across forty buckets. Visibility into your spending is still useful, and most people use a transaction-tracking app to see deposits and outflows in one place, but no human is hand-sorting purchases into categories every Sunday. The balance in each account is the feedback. If the Lifestyle account is empty by the third week, discretionary spending stops. That is the system working as designed. If the Essentials account is running low, that is a signal to look at what is structurally off.

Walk through how this absorbs irregular income. A reenlistment bonus arrives. Twelve thousand dollars lands in the Income account. The pre-decided percentages distribute it the same way they distribute a regular paycheck. A fixed share goes to Essentials. A fixed share goes to the active milestone (which during early stages is debt attack and later is investment). A fixed share goes to Emergency until the buffer target is hit. A fixed share goes to Planned. The bonus does not become a windfall that disappears into discretionary spending. It does not blow up the budget. It scales the system by its size and goes to the same places the next regular paycheck will go.

The same logic handles a BAH adjustment, an SDP payout at the end of a deployment, or special-duty pay that shows up in some months and not others. The system does not have a special mode for any of these. It has one mode. The dollar amounts scale with the deposit. The percentages stay constant.

The decision at the register changes too. Instead of mental math about whether you can afford something, you check the relevant account balance. If the balance covers the purchase, you buy it. If it does not, you wait for the next payday or move money intentionally from another account. The decision is binary, structural, and decoupled from willpower.

Day to day, this changes what the decision feels like. Standing at the grocery store with a cart that came out higher than expected, the question is not “can I afford this?” or “am I being responsible?” The question is “is there enough in the Essentials account?” Same for the dinner out, the new pair of running shoes, the next streaming subscription. You pull up the relevant account balance. The number answers the question. There is no mental tax of justifying the purchase or doing percentage math under fluorescent lights.

There is still ongoing work. The initial setup uses a workbook to calculate the percentages from your real numbers, and the Payday Ritual happens on every paycheck. Once a month, you review the system: are the percentages still right, is one account running dry, is a subscription quietly creeping up. The monthly review is light when the system is steady and heavier after a real life change. What goes away is the daily transaction-categorization and the willpower-at-every-purchase pattern, not the work itself.

Your Next Step Out of the Paycheck-to-Paycheck Cycle

This article gave you the why. The detailed walk-through of what a cash flow system actually does, with separation by purpose and balance as feedback, lives in the next pillar in this domain. Read What a Cash Flow System Actually Does (And Why You Have Never Had One) next if you want to go deeper on the system itself. If you want the full picture of how the four pieces of a financial life fit together, Cutting Spending Alone Won’t Get You There covers that.

Whichever you do, do not go back to trying harder at the budget. The budget was the wrong tool. You have already proven that. The path forward is structural.

Fix the cash flow first. Everything else gets easier.

Build the Architecture for Your Household

If you are ready to actually build the architecture for your household, that work happens inside the Millionaire Veteran community. The community is free. The course inside it walks you through the Compass Method setup with an AI advisor that uses your actual numbers (your real BAH, your real essentials, your real debt, your real income) to build the percentages and the account structure for where you are right now.

About the Author

Joshua Breaux

Retired U.S. Marine

Financial Management Analyst

BS & MBA in Analytics

His family runs on the same systems he teaches here.

This content is educational and does not constitute personalized financial advice. Millionaire Veteran is not affiliated with the Thrift Savings Plan, FRTIB, or the U.S. Government. Past performance does not guarantee future results.