Most military retirement planning articles answer one question: should you take Legacy or BRS, and if BRS, lump sum or annuity?

That covers maybe a quarter of the actual decision. Pension election matters. So do TSP and IRA contributions, healthcare coverage, the tax mix in retirement, and what your earned income looks like in your second career. The pieces interlock. Optimizing one in isolation leaves money on the floor.

This article walks the four moving parts a service member at 12, 15, or 18 years actually has to plan around. It does not personalize. It frames the variables so you can see the whole board before you make decisions on any single piece.

What Most Military Retirement Planning Articles Miss

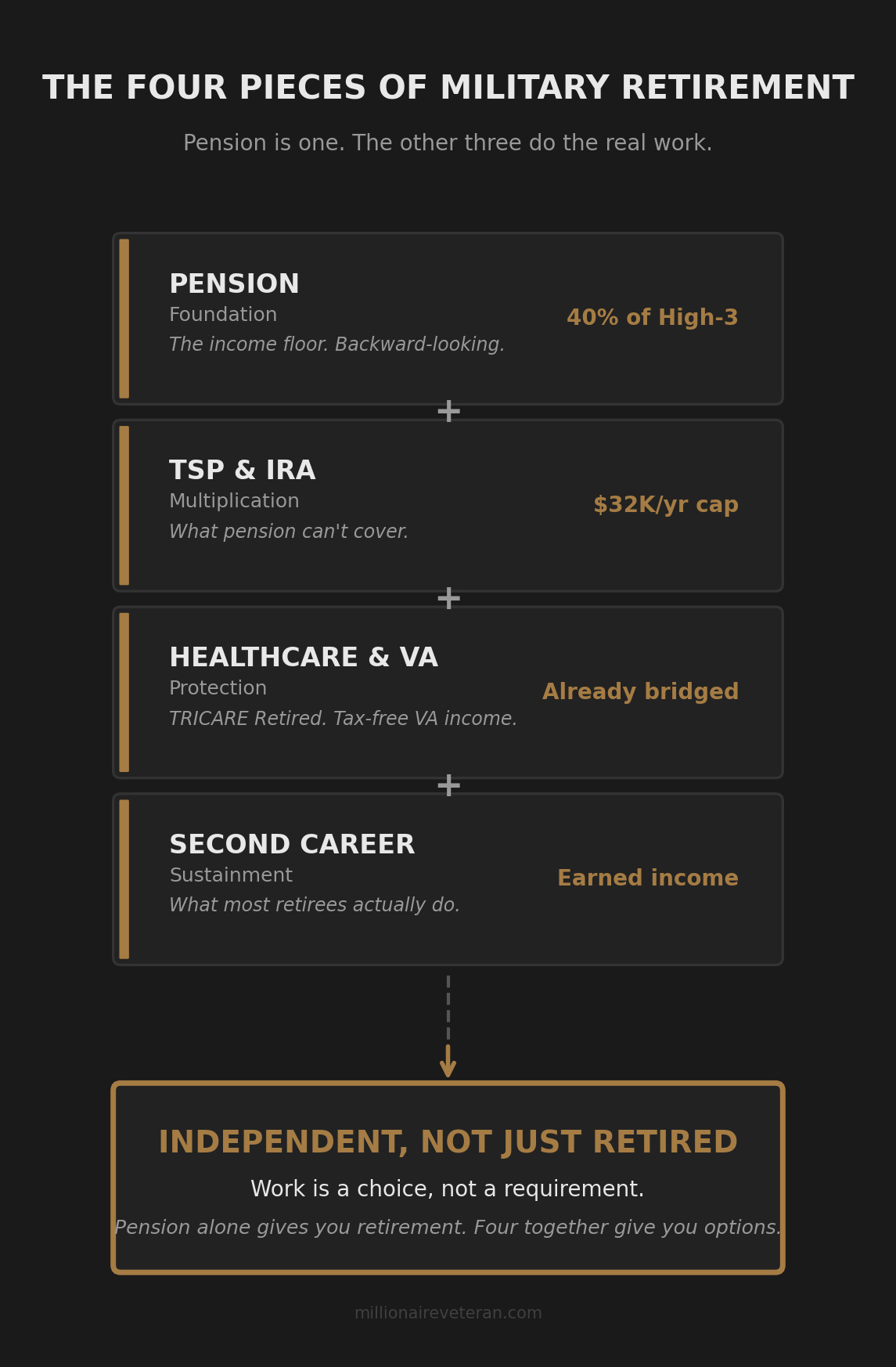

The pension is the most visible part of military retirement, so it gets most of the attention. It is also the part you have the least control over. The percentage is set by the Blended Retirement System. The dollar amount is set by your final High-3 base pay. Once you pass the 20-year mark, the pension calculation is almost entirely backward-looking.

Most of what determines whether retirement actually works is forward-looking. How much you have in TSP and IRAs by the time you separate. Whether you have used Roth TSP, Traditional TSP, or both. Whether you are eligible for VA disability and at what rating. Whether you stay in the military healthcare system after separation. Whether your household runs a cash flow system that keeps contributions consistent through promotions, pay raises, and life changes. And what work, if any, you do in the years between separation and traditional retirement age.

Each of those variables changes the answer to the question “is this enough?” Pension alone almost never is.

The Pension: What It Actually Replaces (And What It Doesn’t)

Under the Blended Retirement System, your pension at 20 years is 40% of your High-3 average base pay. High-3 means the average of your highest 36 months of base pay, which for most retirees is the last 36 months.

Concrete numbers using 2026 pay tables, rounded:

- E-7 retiring at 20 years: roughly $2,240 per month, or about $26,900 per year

- O-4 retiring at 20 years: roughly $3,460 per month, or about $41,500 per year

- O-5 retiring at 20 years: roughly $4,160 per month, or about $50,000 per year

- O-6 retiring at 20 years: roughly $5,060 per month, or about $60,700 per year

Each year of service past 20 adds another 2% of High-3, so a 24-year retirement bumps the multiplier to 48% instead of 40%. The numbers above scale up accordingly.

That is the income side at the moment of retirement. Two issues complicate it over time.

First, lifespan. A retirement that lasts 30 to 40 years has a different shape than one that lasts 15. Inflation eats fixed dollar amounts. Cost of living adjustments help, but your purchasing power 25 years into retirement looks different than your purchasing power on day one.

Second, what the pension actually replaces. If you were an O-4 making $8,650 per month in base pay, your pension replaces 40% of base pay, not 40% of total compensation. BAH, BAS, special pays, and bonuses do not factor into the pension calculation. The income drop at retirement is larger than the pension percentage suggests because the income you had during service included pay categories the pension never replaces.

The pension is a floor. It is not a complete plan.

TSP and IRA: Different Job, Same Importance

The pension protects against living too long. Investment accounts protect against everything else.

TSP and IRA contributions cover the part of retirement the pension cannot. Unexpected medical expenses outside the military system. A larger or smaller lifestyle than the pension dollar amount supports. Helping a child or parent. Inflation outpacing COLA. A second career that pays less than expected.

For 2026, the TSP elective deferral limit is $24,500. The IRA limit is $7,500 per person. A married service member contributing the full elective deferral plus IRA contributions for both spouses is putting roughly $39,500 per year into tax-advantaged retirement containers. Plus the BRS match on top of TSP contributions.

That number is the actual target for service members planning to retire. Not “save what you can.” Not “max out TSP eventually.” Both standard tax-advantaged containers, fully funded, every year possible.

The two accounts do different things in retirement. TSP gives you a single low-cost investment lineup. IRAs give you flexibility, with different fund choices, different tax options, and different withdrawal rules. Most retirees benefit from having both. The case for maxing TSP first comes down to the BRS match. The case for funding IRAs alongside TSP comes down to retirement flexibility.

The math from Millionaire Veteran: The Math Behind Becoming a Millionaire on Military Pay runs the same way here. Compounding works at military pay levels. The math gets there. But only if the contributions actually happen, year after year, with no extended pauses.

The most common failure mode is starting late. A service member who waits until 12 or 15 years in to start maxing their TSP gives up most of the compounding window. Concrete example: $24,500 per year for 20 years at a 7% average return reaches roughly $1,000,000 at separation. The same contribution made only for the last 8 years of a 20-year career, with $0 in the first 12 years, reaches roughly $260,000. Same annual contribution, same time at the deferral limit, but a quarter of the balance at retirement. Compounding rewards starts, not effort applied at the end.

TRICARE and VA: The Healthcare Variable Civilians Cannot Solve

Civilian retirement planning has a healthcare problem that does not apply to you in the same way.

In civilian financial-independence circles, the bridge from employer health coverage to Medicare at age 65 is the single most common reason retirement plans fail. Plans built on solid investment math get destroyed by health insurance costs in the gap years.

Military retirees who serve 20 years are eligible for TRICARE Retired (TRICARE Prime or Select for retirees). After age 65, TRICARE for Life pairs with Medicare to cover most healthcare costs. It is not free, but the costs are predictable and far lower than what a civilian retiree faces buying coverage on the open market.

VA disability adds another layer. Service-connected conditions rated by the VA generate a tax-free monthly payment. The 2026 rates (effective December 1, 2025) start at $180.42 per month for a 10% rating with no dependents and reach $4,158.17 per month for a 100% rating with a spouse, with higher amounts for veterans with children or special monthly compensation. Combined ratings of 30% to 70% are common among retiring service members and produce meaningful tax-free income. That income reduces what the pension and investment accounts have to cover.

Two practical notes. First, dental and vision coverage is not in TRICARE Retired by default. The FEDVIP program covers those for retirees and dependents through separate enrollment. Second, the TRICARE for Life pairing with Medicare at 65 requires Medicare Part B enrollment, which carries a monthly premium. Neither of these undoes the structural advantage. They are footnotes, not blockers.

Civilian retirement plans spend years figuring out how to bridge the healthcare gap. Yours is already bridged. The rest of the plan still needs work, but the largest unknown in civilian financial-independence math does not apply to you.

The Tax Trap Most Retirees Walk Into

Pension is taxable. Social Security is partially taxable, depending on combined income. Traditional TSP withdrawals are taxable. VA disability is the only piece that is not.

The result, for many retirees, is a higher tax bracket in retirement than they expected during service. Three sources of taxable income stacking on top of each other. If most of your TSP balance is in Traditional, you are paying ordinary income tax on every dollar you withdraw, on top of the pension and Social Security.

A concrete example. An O-5 retiring at 20 with a $50,000 pension, $30,000 in annual Social Security at full retirement age, and $40,000 per year drawn from a Traditional TSP balance has roughly $115,000 of taxable income (Social Security taxation is partial). Married filing jointly with the standard deduction, that lands in the 22% bracket. A retiree with a meaningful Roth balance can pull the same total income but draw more of it from Roth. Same lifestyle, lower tax bill, more flexibility.

The fix starts during service. Roth TSP contributions and Roth IRAs build a tax-free pool you can draw from in retirement to manage your bracket. Combat Zone Tax Exclusion windows are an exceptional time for Roth contributions because the income going in is already untaxed. The full Roth versus Traditional decision is its own topic with too many variables to compress into one section. The headline for retirement planning purposes: a 100% Traditional balance creates a tax problem that is harder to solve later than to avoid earlier.

If you are at year 12 or 15 with everything in Traditional, the in-plan Roth conversion process the TSP introduced in 2026 gives you a tool to rebalance the mix. Conversions are taxable in the year they happen, so timing matters. Years with combat zone exclusions, lower household income, or planned separation can create bracket space for conversions at lower marginal rates.

Post-Service Income: Plan For It, Not Around It

Most military retirement planning content ignores or downplays second-career income. In practice, most retired service members keep working in some form. Government civilian roles. Defense industry. Consulting. Teaching. Trades. Small business.

That income changes what the rest of the plan has to do. A retired O-5 with a pension of $50,000 a year and a second-career civilian salary of $90,000 has a different planning problem than the same officer with a pension and no other income. The investment accounts get more time to grow before withdrawals start. The Social Security claiming decision shifts. The tax mix gets more complicated.

Planning for “pension only, nothing else” is conservative but unrealistic for most retirees. Planning for “pension plus typical second-career income” is closer to what actually happens. The right framing assumes the second-career income is part of the picture, then stress-tests what happens if it is not.

The second-career planning question most service members underweight is the gap between the moment of separation and the start of the second job.

Concrete numbers. A retired E-7 takes home roughly $2,240 per month from the pension. If essential household expenses (housing, utilities, insurance, food, transportation) run $5,000 per month, the pension covers about 45% of fixed costs. A three to six month civilian job search creates a gap of roughly $11,000 to $22,000 between what the pension delivers and what the household actually spends. Without a real emergency fund sitting separate from investment accounts, that gap gets covered by credit cards, early TSP withdrawals (which trigger a 10% penalty if you separated before age 55), or selling investments at whatever price the market is offering when you happen to need cash. None of those options leave you better off than walking into separation with the gap already pre-funded.

The fix is structural, not heroic. A safety net of three to six months of essential expenses, in a separate savings account, sized before you submit the retirement paperwork. That account does one job: it absorbs the gap years between active duty income and post-service income, without disrupting the long-term retirement plan.

Independent or Just Retired?

A military retirement gives you a steady income. Financial independence gives you options.

Different bars. Most service members who hit 20 years are retired in the technical sense. The pension shows up every month. They are not financially independent in the FI sense, where investment income alone covers chosen expenses with no other earned income required. The two states are often confused, and the confusion costs people years.

The retired service member whose pension covers core living costs but whose investment accounts are thin has options that look like options. They can stop working, but only if their lifestyle stays close to the pension dollar amount. They can cover an emergency, but only if the emergency is small. They can support a family member or take a sabbatical, but the budget tightens fast.

The retired service member with a fully funded TSP, a Roth IRA balance, three months of safety net, no inefficient debt, and a healthy money management system has actual options. They can take the second-career job that interests them, not the one that pays. They can stop working without compressing their lifestyle. They can absorb an unexpected expense without restructuring the household.

This is the part of military retirement planning that the pension election and the contribution limits do not tell you on their own.

Where to Go From Here

If you are early in service or just starting to think about this, the math behind it is in The Math Behind Becoming a Millionaire on Military Pay. That article walks through how compounding actually works at military pay levels and shows the contribution targets that make the system work.

If you want to know where you are right now on the path, The FI Spectrum: Five Stages Between Surviving and Fully Independent gives you a way to locate yourself. Surviving, stable, building, Coast FI, and fully independent are recognizable states. Most service members reading this are at one of the middle three.

The investing side of the plan starts with The Blended Retirement System Changed Everything. The pension calculation changed when BRS replaced High-3 for everyone entering after 2018. That article covers what the change actually was and why it shifts the planning math.

The full sequence, including what to do first, second, and third, is in The Six Milestones Between You and Financial Independence.

Take the First Real Step

You can read every retirement planning article on the internet. Most service members do, eventually. The reading does not change your numbers.

The free Millionaire Veteran community walks through a Diagnostic Review that takes your real income, real debt, real spending, and real account balances and maps them to the roadmap. It shows you which milestone you are at, what gate you need to clear next, and what your contribution allocations should look like with your actual numbers.

The blog teaches the framework. The community puts you in it.

About the Author

Joshua Breaux

Retired U.S. Marine

Financial Management Analyst

BS & MBA in Analytics

His family runs on the same systems he teaches here.

This content is educational and does not constitute personalized financial advice. Millionaire Veteran is not affiliated with the Thrift Savings Plan, FRTIB, or the U.S. Government. Past performance does not guarantee future results.