I named this site Millionaire Veteran because the math actually works at military pay rates. “TSP millionaire” is not aspirational language for me, it is a mathematical destination that any military participant can reach through consistent contributions, a sensible allocation, and the discipline not to interrupt the compounding when markets get loud. The Federal Retirement Thrift Investment Board (FRTIB) publishes the count of participants who have crossed seven figures in their individual Thrift Savings Plan (TSP) account, and that count has grown steadily over the past decade as more people reach the threshold.

The question most readers bring to this search is whether the number is realistic for them specifically, or whether it is reserved for officers, civilian high earners, or thirty-year careers that ended at the right rank. I will walk through the math directly: what the term means, how it works on military pay, what most coverage of the topic leaves out, and the variables that actually determine when you arrive.

What Counts as a TSP Millionaire

A TSP millionaire is defined by a single number: an individual TSP account balance at or above $1,000,000. That is the threshold. It is not household net worth, not retirement net worth, not the combined account balance of two spouses. It is the balance shown on one TSP statement, in one participant’s name.

The Federal Retirement Thrift Investment Board, which administers the plan, publishes the count of TSP millionaires in its quarterly board meeting minutes. The count tends to fluctuate with market conditions: rising in expansionary periods, dipping during drawdowns, then recovering as markets recover. The trend over the past decade has been steady growth in the total count, driven by a combination of participants reaching the threshold for the first time and existing TSP millionaires staying above it through compounding.

The balance is reached through three inputs: contributions over time, the Blended Retirement System (BRS) match for service members (or the FERS match for federal civilians), and market growth on the accumulated balance. Most TSP millionaires reach the status through some combination of all three, sustained across a long career. The variance across individual paths is enormous, which is why the term itself does not say much about how someone got there. Two TSP millionaires can have entirely different stories.

The Math at Military Pay Rates

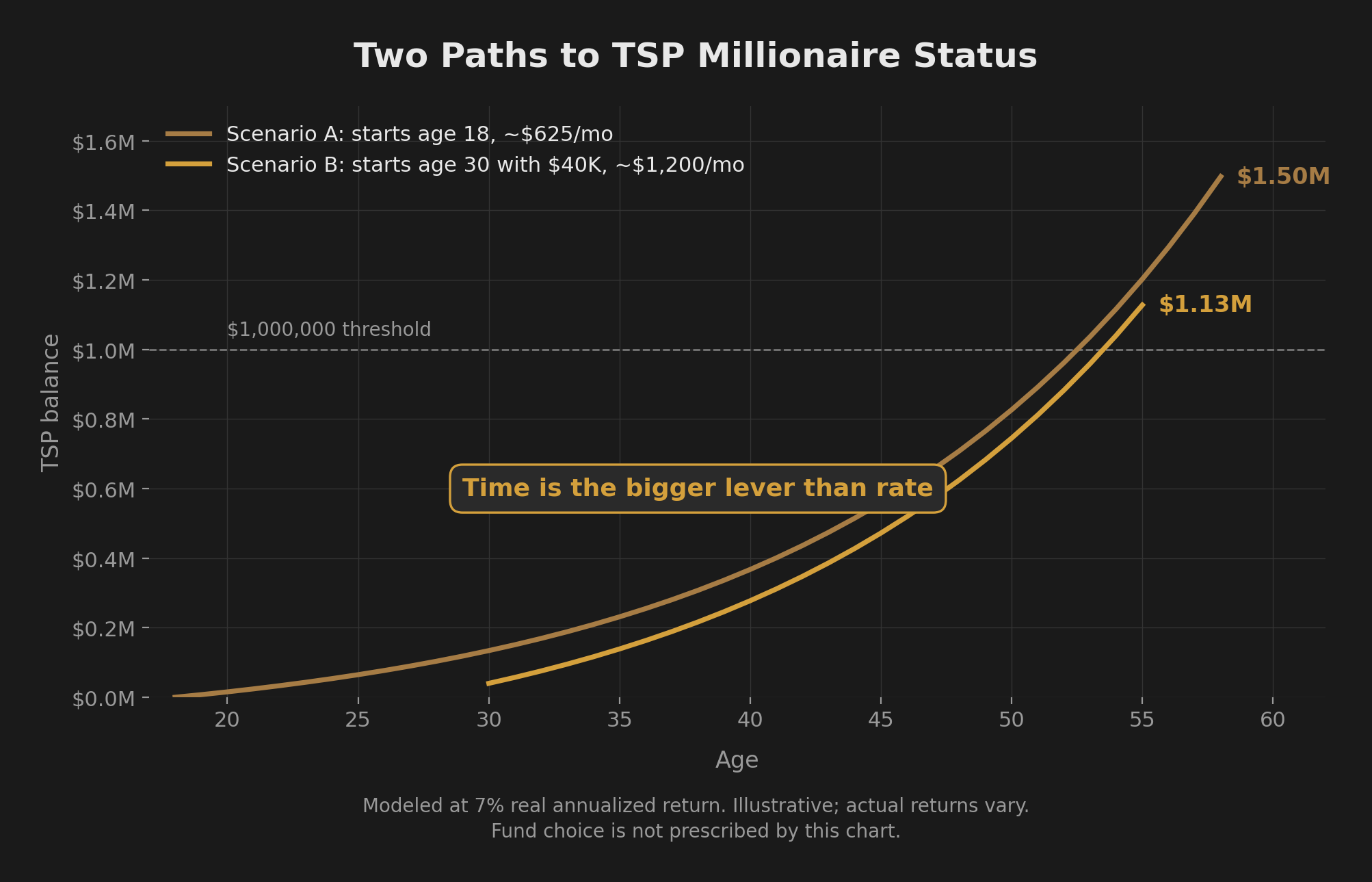

The structural argument is straightforward. Two scenarios show that becoming a TSP millionaire on military pay is a function of time and consistency, not unusual income or contribution heroics. Both scenarios assume a 7% real annualized return as the modeling assumption. That is a standard long-horizon equity-weighted growth assumption used in retirement projections. It is not a guarantee and it is not a fund recommendation.

Scenario A: Steady early-career contributor. A service member enters at 18 and contributes 10% of base pay throughout the career, with base pay growing through rank progression and time-in-service raises. The BRS match adds another 5% of base pay on top of the first 5% contributed. Modeled at 7% real annualized return across the contribution window. By the end of the full TSP-allowable contribution window (which extends into civilian-converted federal service if applicable, or via rollover IRA growth if the participant separates earlier), the account compounds past seven figures.

Scenario B: Mid-career corrector. A service member at 30 with a $40,000 starting balance increases contribution to 15% + BRS match. Modeled at 7% real annualized return over the next 25 years. Account reaches $1,000,000+ before age 55.

Both scenarios are illustrative, not promises. Both use realistic military pay trajectories, realistic contribution rates that are not maxed out, and a single modeling return assumption. Both produce TSP millionaire status well within a normal working life. The reader does not need to be an officer, does not need a 30-year career, and does not need to be contributing the federal limit every year. Time and consistency carry more of the load than income heroics do.

What Most TSP Millionaire Coverage Leaves Out

Most articles about TSP millionaires focus on the highest-balance individuals: senior officers with thirty-plus years of service, high contribution rates throughout their careers, and aggressive fund allocations. That story is real but it is the outlier at the top of the distribution. The MEDIAN TSP millionaire trajectory looks closer to Scenario A or B above: steady contributions over time, holding through volatility, taking the match, and not interrupting the compounding.

The variance under the TSP millionaire label is enormous. Some reach the threshold in their early 50s. Some reach it in their late 60s after starting late. The difference between those two outcomes is mostly about how early the contributions started and how few times the participant interrupted the compounding by selling out during a drawdown or pausing contributions during a hard stretch.

The TSP millionaire is what compounding produces when nobody interrupts it.

That is the part most coverage leaves out. The destination is the math working uninterrupted for long enough. The participants who reach it are not unusually disciplined or unusually well-paid; they are unusually consistent. The pattern repeats across the FRTIB data and across the published profiles of TSP millionaires the federal community produces.

“Uninterrupted” in practice means specific things. It means contributions continue through pay cuts, through PCS moves, through household tightness, through deployments where the dollars feel like they should go somewhere else. It means the allocation stays in place through 2008-style drawdowns, through pandemic-driven volatility, through any of the regular cycles markets put participants through every decade. It means the account does not get raided for non-emergencies, does not get rolled into something with worse expense ratios, and does not get abandoned mid-career when the participant decides retirement is too far away to matter. The interruptions are what destroy the math. Every one that the participant avoids is one less hole the compounding has to climb out of.

Why Military Pay Makes the Math Work

Military pay carries structural advantages that compound alongside the math, and the typical civilian 401(k) plan does not match them on either expense ratio or match rate.

The TSP itself has the lowest expense ratios available in any retirement plan, including 401(k) plans at most employers. Lower expenses mean more of each dollar contributed actually compounds, and over a 30-year horizon the difference between a 0.05% expense ratio and a 0.50% expense ratio is significant.

The BRS match adds 5% of base pay on top of the first 5% the service member contributes. That is a guaranteed 100% return on the matched portion before any market return enters the equation. Most civilian employer matches are a fraction of this.

Military pay trajectories are predictable. Rank progression and time-in-service raises happen on known schedules. That predictability makes it possible to plan contribution rates years in advance and trust that the cash flow will support them as pay grows.

The pension floor (for those who retire from service) reduces how much the TSP needs to do in retirement. A service member with a pension covering basic expenses has more flexibility in how aggressively they draw down the TSP balance, and the TSP itself does not need to cover 100% of retirement income.

VA disability (where applicable) is tax-free income for life. TRICARE removes most of the healthcare cost uncertainty that derails civilian retirement plans. Both reduce the dollar target the TSP needs to hit.

Stacked together, these structural advantages mean military participants starting from the same income as civilian counterparts generally land at higher TSP balances because the math is doing more work and they have more flexibility to keep contributing.

The Variables You Actually Control

Three drivers determine whether you reach TSP millionaire status, and the order they appear in below is the order they actually matter in over a long career.

Allocation. Fund choice within the TSP has the largest single impact on outcome over a 25-year career. The variance between patterns is enormous; the same contribution rate produces very different balances depending on what the dollars are doing inside the account. The framework for the major patterns most TSP holders fall into lives at the four TSP allocation patterns. That article walks through the patterns directly so you can identify which one your current account represents and which one fits the stage you are in.

Holding behavior. What you do during drawdowns matters more than what you do in calm markets. Selling out during a 30% decline and waiting for “things to stabilize” destroys long-term returns more than any single fund choice does. The behavioral test happens at the worst possible moment, when the news is loudest and the urge to act is strongest. The two TSP risks your BRS briefing never covered walks through both behavioral risk and sequence-of-returns risk in detail.

Holding through drawdowns is harder than it sounds. The TSP interface is two clicks away from the G Fund. The market news is in your pocket every hour of the day. Friends and family who do not invest will tell you to “get out before it gets worse.” The discipline to hold is not the discipline to do nothing; it is the discipline to keep doing the thing you already decided to do, in conditions that make the original decision feel wrong. That is why the framework around holding matters more than any one drawdown event. A participant who understands what each fund is supposed to do, understands what a drawdown actually is, and has already pre-decided how to respond to one is materially different from a participant making that decision under pressure for the first time.

Contribution rate. Important, but third on the list at long horizons. Saving more is better than saving less, and the BRS match is the highest-priority contribution dollar in the entire stack. Beyond the match, additional contributions help, but compounding rewards time and consistency more than it rewards small percentage increases at long horizons. A service member contributing a moderate percentage for thirty years in a thoughtful allocation generally outperforms a service member maxing contributions for fifteen years in a poorly chosen one.

The order: allocate thoughtfully, hold the allocation, then layer contributions on top. Most “how to become a TSP millionaire” content reverses this order because contribution rate is the easiest variable to write about.

Your Next Step

Seven figures is reachable. The harder question is whether seven figures is the right target for you, or whether you should be aiming higher because time is the one variable you cannot buy back. Every year of delay costs more than the year before it. Overshooting beats undershooting because the compounding years you skipped are not recoverable later through any contribution rate.

The full Millionaire Veteran math, including the asymmetric-hedge logic on why front-loading tax-advantaged accounts beats waiting, lives at Millionaire Veteran: The Math Behind Becoming a Millionaire on Military Pay. That article extends the case from a single TSP balance to the full retirement architecture and the variables you control across it.

Build Your Path to TSP Millionaire Status With Your Real Numbers

Millionaire Veteran is a free community where military families put their real numbers on the Azimuth Roadmap: rank, take-home, debt load, and timeline. The Diagnostic Review shows which milestone is actually standing between you and seven figures. It is a routing tool, not a fund-recommendation tool. The Compass Method then routes the cash flow so the contributions happen on payday, every payday, instead of getting approved on paper and never leaving the account.

About the Author

Joshua Breaux

Retired U.S. Marine

Financial Management Analyst

BS & MBA in Analytics

His family runs on the same systems he teaches here.

This content is educational and does not constitute personalized financial advice. Millionaire Veteran is not affiliated with the Thrift Savings Plan, FRTIB, or the U.S. Government. Past performance does not guarantee future results.