Service members searching for C Fund TSP performance want real numbers, not vague answers. Here they are. The C Fund has delivered an average annual return of approximately 10% since its 2004 inception. It also dropped roughly 50% between late 2008 and early 2009. Both numbers are true. Both matter when you’re managing your TSP.

This article lays out the full track record: the growth, the drawdowns, the recoveries, and what the data looks like when you translate it into a real military career.

What the C Fund Actually Is

The C Fund tracks the S&P 500, an index of large U.S. companies. It doesn’t pick individual stocks. There’s no active manager making calls. The fund owns a slice of hundreds of major companies and moves with the market.

This matters because it changes how you interpret the numbers. When the C Fund drops, the broad U.S. stock market dropped. When it grows, the broad U.S. stock market grew. You’re not betting on a sector or a single company. You’re investing in American business as a whole.

The expense ratio is minimal: one of the lowest-cost large-cap index funds available anywhere. Lower than virtually every civilian 401(k) equivalent.

How TSP C Fund Performance Holds Up Over Time

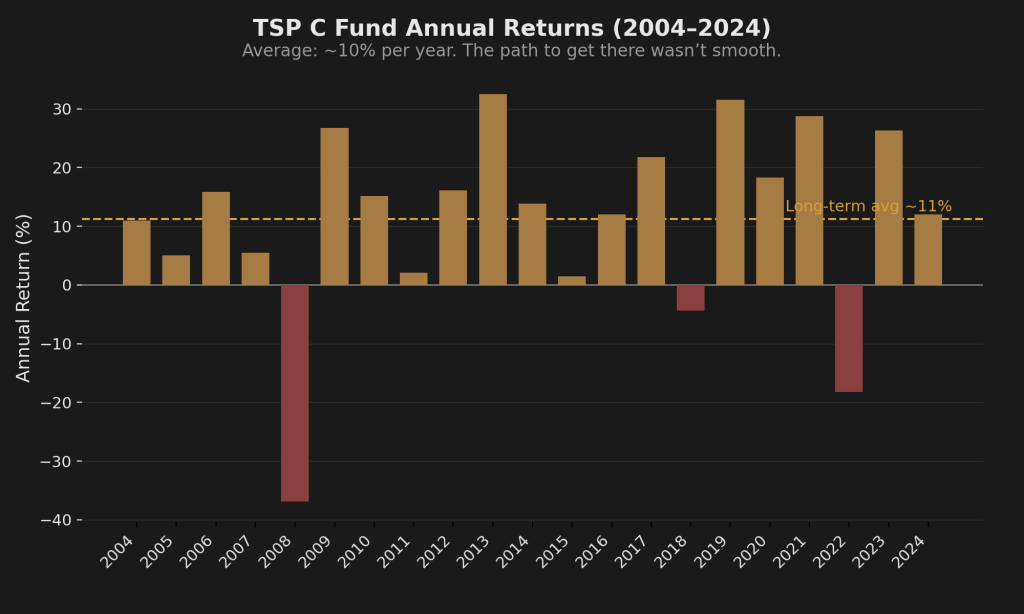

The long-term track record is strong. Since 2004, C Fund TSP performance has averaged approximately 10% per year. That number includes the 2008 financial crisis, the 2020 COVID drop, and the 2022 bear market. All three are folded in.

But the long-term average hides how those returns were distributed. Some years the C Fund returned over 30%. Other years it dropped more than 20%. The average is a useful benchmark. The actual experience of being invested through those years is very different.

Here’s how the returns have played out by era.

Decade Return Summary

| Period | Approximate Annualized Return | What Happened |

|---|---|---|

| 2004-2007 | ~12-14% | Strong post-recession growth, housing boom |

| 2008-2009 | Negative (crisis years) | Financial crisis; ~50% peak-to-trough drawdown |

| 2010-2019 | ~13-14% | One of the strongest bull decades in history |

| 2020 | ~18% | COVID crash and rapid recovery in same calendar year |

| 2021 | ~29% | Post-pandemic market surge |

| 2022 | ~-19% | Rate hike driven bear market |

| 2023-2025 | ~10-12% (estimated) | Recovery and continued growth |

The decade from 2010 to 2019 was exceptional. If you started contributing in 2010 and looked at your balance in 2019, you would have been thrilled. If you started contributing in 2007 and checked your balance in March 2009, the picture would have looked very different, even though the same fund was doing its job the entire time.

What a 20-Year Military Career Looks Like in Real Dollars

Numbers in a table are one thing. What they mean inside a real career is another.

Take a service member who enters service in 2004 and contributes $500 per month to the C Fund for 20 years straight. That’s $6,000 per year, which is well within BRS contribution norms for someone who increases contributions with each promotion.

Total amount contributed over 20 years: $120,000.

Approximate balance after 20 years at the C Fund’s historical average return of ~10%: roughly $340,000 to $380,000.

That’s the compounding effect on a consistent, disciplined contribution. The gains didn’t come from one good year. They came from staying in, year after year, while the contributions kept landing on top of prior growth. The person who contributed $120,000 is sitting on roughly $220,000 to $260,000 in pure growth. Not from timing. Not from fund-switching. From staying put and letting the math work.

Now increase the contribution as rank and pay increase. An E-5 who starts at $500/month and gradually reaches $800/month by E-7 ends up with even more. The numbers scale, but the principle doesn’t change: time in the fund, not timing the fund, is what drives the outcome.

What the Numbers Don’t Show: The Drawdown Picture

Three events are worth understanding directly, because they represent three different types of stress tests for anyone watching their C Fund TSP performance.

2008 to 2009. The C Fund dropped approximately 50% from peak to trough. A $200,000 balance in early 2008 became approximately $100,000 by March 2009. Recovery to new highs took roughly four years. Anyone who sold during the drop locked in that loss permanently. Anyone who held recovered fully and continued growing.

2020. The drop was fast and deep: approximately 34% in about five weeks, February to late March. Recovery was equally fast. Most balances returned to pre-crash levels within five months. The 2020 drawdown tested something different than 2008: not staying power over years, but staying power over weeks. Many investors still made the wrong call.

2022. A slower, grinding decline: approximately 19% over the year as the Federal Reserve raised interest rates aggressively. Less dramatic than the prior two events, but sustained long enough to wear down conviction.

Three different drawdown types. One consistent pattern: the investors who fared worst were the ones who made decisions based on how they felt in the moment.

What Drawdowns Actually Cost in Real Dollars

To see what those drawdowns cost in real dollars, consider a service member 15 years into their career with a $300,000 C Fund balance.

A 50% drawdown: $150,000 gone from the screen. A 34% drawdown: $102,000. A 19% decline: $57,000.

Those are not abstract percentages. They’re the numbers on the app when you log in on a Tuesday morning.

The Part Most People Miss: Dollar-Cost Averaging During Drawdowns

Most people skip right past this when they look at drawdown charts. If you’re actively contributing to your TSP during a drawdown, you’re buying shares at lower prices.

A service member contributing $600/month during the 2008-2009 crisis was buying C Fund shares at a roughly 50% discount to their pre-crisis price. Those shares purchased near the bottom of March 2009 more than tripled in value over the following decade.

This is the structural advantage of being a military service member with automatic payroll deductions. You don’t have to decide to buy during a drawdown. The allotment does it for you. Every pay period, like clockwork, you’re accumulating shares at whatever price the market offers.

The people who benefited most from the 2008 recovery weren’t the ones who timed the bottom. They were the ones who never stopped contributing. Their per-share cost averaged down during the worst of it, and when recovery came, those discounted shares amplified the rebound.

Dollar-cost averaging doesn’t eliminate risk. It doesn’t mean drawdowns are painless. But it does mean that for service members who are still contributing, a drawdown is doing two things at once: temporarily reducing the value of existing shares AND reducing the cost of new ones. The second part only matters if you stay in.

The Behavioral Gap: Same Fund, Different Outcome

The C Fund can do its job. The question is whether you’ll let it.

This is the part that performance charts don’t capture. Two service members can be in the exact same fund, with the exact same contribution rate, and end up with very different outcomes. The difference isn’t the fund. It’s the behavioral pattern underneath it.

A Reactive Mover, someone who shifts to a defensive position when headlines get loud and shifts back after the market recovers, consistently underperforms even while technically invested in the C Fund for most of the period. They miss the recovery. They buy back in after the gains. They pay an invisible tax on every drawdown cycle, not because they chose the wrong fund, but because they reacted at the worst possible moments.

That behavioral gap is measurable. Research consistently shows that the average investor’s actual return lags the fund’s stated return by several percentage points per year, compounded over decades. That determines your actual return more than which fund you picked.

The service members who do best in the C Fund aren’t necessarily the most sophisticated. They’re the ones who built enough understanding of what they’re in that they could hold through a real drawdown without second-guessing themselves.

If you’re curious about which behavioral pattern you’re actually in, that’s the next question worth exploring. The Four TSP Allocation Patterns breaks down all four behavioral patterns, the psychology behind each, and what each one costs over a career.

How TSP C Fund Performance Fits Your Career Stage

The C Fund means something different depending on where you are in your military career. Understanding this is part of understanding what you’re actually holding.

One important distinction: military retirement (leaving active duty) can happen as early as age 38 for someone who enlisted at 18 and served 20 years. But TSP withdrawal without penalty doesn’t begin until age 59.5. That means a service member who “retires” from the military at 38 still has over 20 years before they touch their TSP. The timeline that matters for your C Fund allocation is the distance to withdrawal age, not the distance to your separation date.

Early Career (Age 18 to 30)

Your balance is small. A 50% drawdown on a $15,000 balance is $7,500. That stings, but it’s recoverable in a few months of contributions alone. More importantly, every dollar you contribute during a drawdown buys shares at a discount.

Time is overwhelmingly on your side. A 20-year-old has roughly 40 years before TSP withdrawal age. Even a 30-year-old has nearly 30 years. The math is simple: decades of compounding ahead outweigh any single-year loss.

At this stage, being in the C Fund is almost purely upside over that timeline. The risk is not the drawdown. The risk is getting spooked by a drawdown early on and developing a reactive behavioral pattern that costs you for the rest of your career.

Mid-Career (Age 30 to 45)

Your balance is larger. A 50% drawdown on $150,000 is $75,000. That’s a real number with real psychological weight. But you still have 15 to 30 years before withdrawal age. The recovery math still works in your favor, and dollar-cost averaging during a drawdown at this balance level can add meaningful growth on the back end.

This is the stage where conviction matters most. You have enough money at stake that a drawdown feels serious, but enough time left that holding through it is almost certainly the right call. The service members who panic-sell at this stage aren’t in the wrong fund. They’re missing the foundation beneath their allocation.

The Red Zone (Age 50 to 59, Approaching Withdrawal)

This is where the calculus genuinely shifts. Your balance may be $300,000 or more. A 50% drawdown is $150,000. Recovery takes years, not months. And if you’re within 5 to 10 years of withdrawal age, you may not have the timeline to wait for a full recovery.

The Red Zone doesn’t mean the C Fund is wrong. It means the stakes of being in the C Fund without a plan for drawdown management are highest here. This is where understanding your behavioral pattern matters most, because the cost of a reactive mistake at this balance level can wipe out years of disciplined contributions.

The BRS Connection

Under the Blended Retirement System, the TSP is the primary vehicle for building retirement wealth beyond the reduced pension. The legacy system offered a 50% base pay pension at 20 years. BRS offers 40%, plus government matching in the TSP. That 10% pension gap means the C Fund isn’t just one option among many. For BRS service members, it’s the primary growth mechanism for closing that gap.

This is why C Fund TSP performance matters more under BRS than it did under the legacy system. The TSP balance you accumulate has to do more of the work. That makes both the growth potential and the behavioral risk more consequential than they were a generation ago.

The Question Worth Asking

You came here for C Fund TSP performance data, and now you have it. The long-term return. The drawdowns. The recovery timelines. The career-stage math.

But the number that will matter most to your actual outcome isn’t on any performance chart. It’s the answer to this question: could you hold your position if your balance dropped 40%? Not in theory. In real dollars, on your actual balance, with headlines telling you it’s going lower.

That question has nothing to do with the C Fund itself. The C Fund did its job through every one of those drawdowns. It recovered. It grew. It compounded.

The question is about you. What behavioral pattern are you in? Are you in the C Fund by default, because someone on Reddit said to, or are you in the C Fund by understanding, because you’ve looked at the drawdown math and decided you can hold?

The distance between those two positions is the distance between selling in March 2009 and holding through it. Same fund. Different outcome.

Get the Full Blueprint

The Firewatch Blueprint walks through all four behavioral patterns, the drawdown math in real dollars, and the three-strategy framework built to address each one. If you’re in the C Fund and want to know whether your conviction would survive a real drawdown, this is where that question gets answered.

About the Author

Joshua Breaux

Retired U.S. Marine

Financial Management Analyst

BS & MBA in Analytics

His family runs on the same systems he teaches here.

This content is educational and does not constitute personalized financial advice. Millionaire Veteran is not affiliated with the Thrift Savings Plan, FRTIB, or the U.S. Government. Past performance does not guarantee future results.