Envelope budgeting actually works. It has worked since before there were apps, before there were spreadsheets, before there were debit cards. People who run it consistently end the month knowing exactly where their money went and never wondering if there is enough for groceries on the 28th.

The principle behind it is simple, and it is the same principle that powers every working cash flow system today: every dollar gets a job before it is spent, and the place that holds the dollars tells you the truth about what is available without any tracking.

What follows is the honest walkthrough of how does envelope budgeting work in practice, why it works when methods built around tracking and willpower do not, where physical cash strains against a 2026 financial life, and what the modern equivalent looks like once you are carrying a phone with a bank app on it.

This is for two readers. The one who has never used envelopes and is curious whether they make sense to try. And the one who tried envelopes during a tight stretch, found something worked, and wants to understand the structure well enough to either run it better or graduate it.

How Envelope Budgeting Works: The Mechanics

The mechanics are simple enough to fit on an index card.

On payday, you withdraw cash. Not all of it. The portion you control with discretionary spending decisions across the next two weeks (or month, depending on your pay cycle). The fixed obligations like rent, the mortgage, the car payment, utilities, and insurance run on autopay from your checking account. Envelopes do not touch those. The envelope system handles the dollars where your weekly choices actually determine how much you spend.

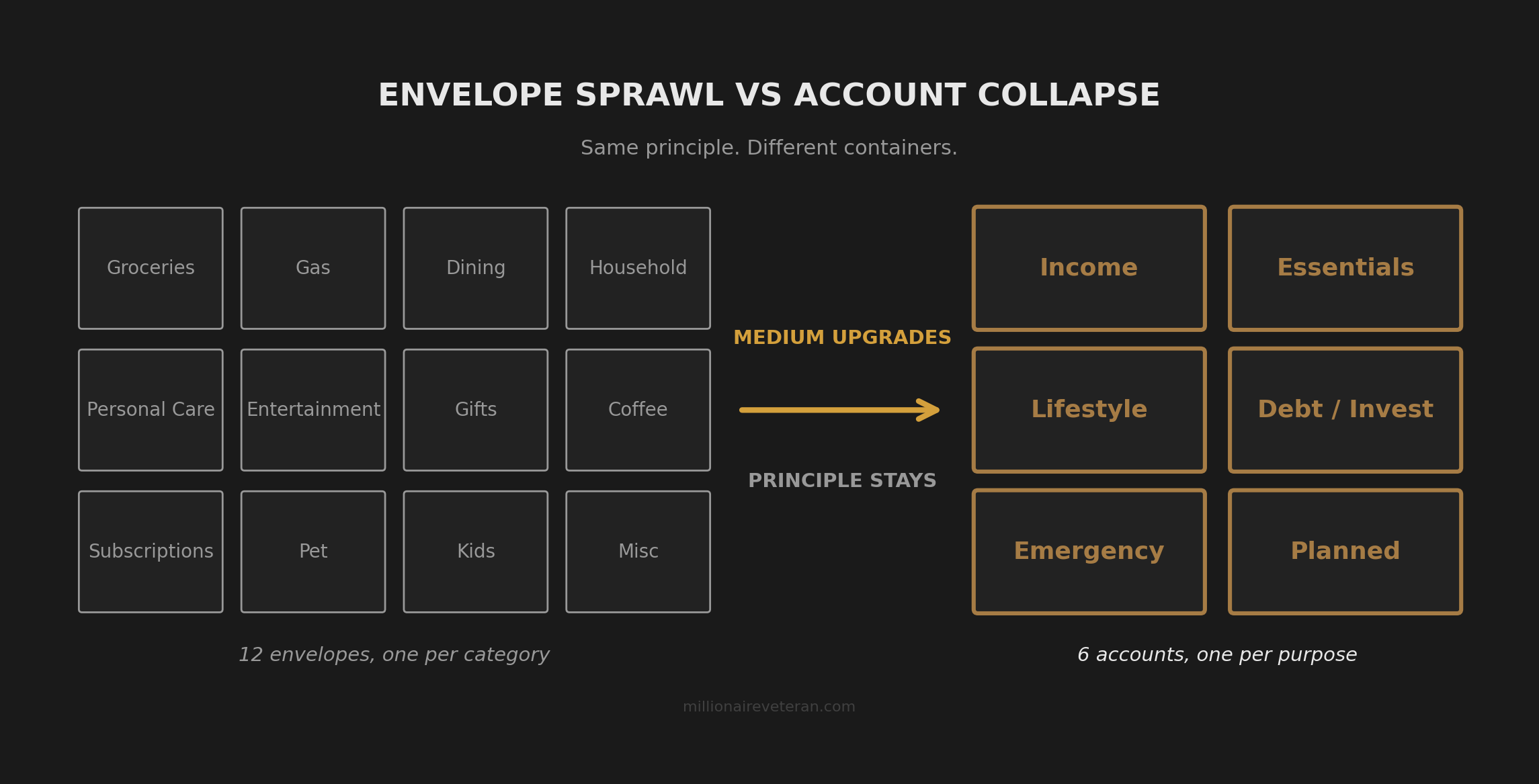

You set up one labeled envelope per spending category. The classic categories are Groceries, Gas, Dining, Household, Personal Care, Entertainment, Gifts. Optional additions show up based on actual spending patterns: a Coffee envelope, a Subscriptions envelope, a Pet envelope, anything else that recurs.

You decide in advance how much goes in each envelope. The decisions can come from prior-month spending or from a fresh estimate of what is realistic. The numbers are commitments, not guesses. A household running envelopes for a biweekly paycheck lands on something like $200 in Groceries, $80 in Gas, $60 in Dining, $50 in Household, $40 in Personal Care, $40 in Entertainment, $30 in Gifts. The specific numbers are illustrative. The point is the decision happens on payday, in advance, and the dollars are physically separated to enforce it.

You spend only from the relevant envelope. Grocery store trip comes out of Groceries. Gas pump comes out of Gas. The Friday dinner out comes out of Dining. The decision at the register is not “can I afford this?” It is “is there cash in this envelope?” The balance is the answer.

When an envelope is empty, that category is done until the next payday. No transfers from other envelopes. No “I’ll just put it on the card and reconcile later.” The empty envelope is the system working. The discomfort of the empty envelope is the feedback the method exists to deliver.

A few practical questions readers almost always have:

- What about bills? Bills run autopay from a checking account, not from envelopes. The envelope system is for the variable spending where your behavior actually controls the dollar amount, not for fixed obligations.

- What about online purchases? This is the first real friction. Cash does not work on Amazon. Envelope budgeters in 2026 either use a separate debit card linked to an account funded by the envelope’s worth, or they convert online purchases back into cash withdrawals after the fact. Both are workarounds. We will come back to this.

- What about saving and investing? The Savings envelope is one option but a weak one because savings dollars live better in a separate account that earns interest and is harder to raid. Envelope budgeters usually pair the system with a separate savings transfer that happens on payday before the cash withdrawal.

The mechanics are the mechanics. The structure beats most things readers have tried for one reason: every dollar of discretionary spending has a job decided in advance, and the cash physically enforces it.

Why It Works When Other Methods Do Not

The mechanics above answer the question “how does envelope budgeting work” at the procedural level. The deeper question is why the method holds when so many other systems quietly fall apart. The answer is structural, not motivational.

Most failed budgeting systems share one feature: the decision about where money goes happens AFTER the money has been spent. The reader categorizes a transaction at the end of the day or the end of the week. The plan and the actual spending are two different documents, and the gap between them is closed through reconciliation work.

Envelope budgeting reverses the order. The decision happens BEFORE the dollar moves. The envelope is filled with cash on payday, and that cash represents a commitment. By the time the reader is at the grocery store, the decision is already locked in. The work at the register is verification, not deliberation.

This is the same structural advantage that any working cash flow system has. Separation by purpose, decided in advance, physically enforced by the medium. The envelope holds only what was assigned to that purpose. The dollars cannot drift into discretionary spending because they are not sitting in a single pool where drift is possible.

The balance in the envelope tells you what is available. No app, no spreadsheet, no mental math. Counting the bills inside is the report. Counting takes five seconds. The feedback is constant and accurate without any maintenance work between paydays.

The willpower demand is also lower than people expect. Most readers assume envelopes require iron discipline because cash is physical and visible. The opposite is true. The hard decisions get made on payday, once, when the reader is calm and thinking clearly. The decisions at the register are mechanical: the envelope has cash or it does not. The mental tax of justifying a purchase under fluorescent lights drops to almost zero because the structure has already answered the question.

This is forward-looking allocation. The envelope had it before there was a name for it.

Where Cash Envelopes Strain in 2026

The principle is intact. The cash is the part that has aged. Asking how does envelope budgeting work in a modern financial life surfaces a list of frictions the method did not have to handle in 1985.

Most income does not arrive as cash. Direct deposit happens automatically, which means an envelope budgeter in 2026 has to go withdraw cash on every payday. That extra step is small but real. It also means a portion of every paycheck has to be earmarked for that withdrawal in the first place, which couples the envelope system to a parallel checking-account workflow that defeats some of the simplicity.

Bills, rent, mortgage, utilities, subscriptions, and insurance run on autopay from a checking account. The envelope system has to coexist with that account, which means there are really two systems running in parallel: an envelope system for variable spending and a checking-account workflow for fixed obligations. Each requires its own attention.

Debit cards and online purchases bypass envelopes entirely. The Amazon purchase, the streaming subscription, the gas station tap-to-pay all happen against the checking account balance, not against an envelope. Either the envelope budgeter accepts that any card-based spending lives outside the envelope structure (which leaks the system) or they go through the friction of converting the dollar amount back to cash after the transaction. Both options have a cost.

Envelope sprawl is the slow-motion failure mode. The system starts with seven envelopes. By month three, there are twelve. By month six, there are eighteen because every time a spending pattern surfaces (Pet, Auto Maintenance, Kids’ Sports, Holiday Gifts, Birthday Gifts, Coffee, Lunches at Work, Misc), it gets its own envelope. The number of envelopes balloons past the point where managing them is faster than just using a card and tracking. The principle is right; the medium scales poorly.

A lost wallet, a stolen envelope, or a house fire has no recovery. Cash without a paper trail is gone if it leaves the envelope. Banks have FDIC insurance. A kitchen drawer does not.

Households with two or more people running shared categories hit access friction. Only one envelope, one location, one person can hold it at a time. The dual-card structure that most household finances run on does not have a clean envelope equivalent. Workarounds exist (multiple envelopes for the same category, scheduled handoffs) but each workaround adds maintenance.

None of these are method failures. They are medium failures. The principle of forward-looking, physically-separated, balance-is-the-answer allocation stayed exactly right. The cash itself stopped being the right delivery system for most of what a household needs to manage.

The Modern Equivalent: Purpose-Specific Bank Accounts

The fix is not to abandon the principle. The fix is to upgrade the container.

Each envelope graduates to its own checking or savings account at the bank. Same separation. Same purpose-based assignment. Same balance-is-the-answer feedback. The labeled envelope becomes a labeled account on a phone screen. The cash withdrawal disappears because the money never needs to be cash to be separated.

On payday, deposits route to purpose-specific accounts by percentage. The same decision that used to happen at the cash counter happens once, in advance, at the bank app. Routing the dollars takes a few minutes. After that, every account holds only what belongs there.

Bills autopay from the right account because each fixed obligation is tied to a specific purpose-account. Utilities run from the Essentials account. Subscriptions run from the Lifestyle account. Debit cards work because each card is tied to a specific purpose-account, which means the card naturally enforces the structure at the register without any envelope to carry. Online purchases work for the same reason. The Amazon order debits from whichever account funds that purpose.

The dozen-envelope sprawl collapses to a smaller, purpose-built set of accounts. Six accounts is usually enough because each account holds a purpose (essentials, lifestyle, emergency, milestone funding) rather than a category (groceries, gas, dining, household, personal care, gifts, kids, pet, coffee). The category-level decisions move down into the purpose-account, which means the system handles spending pattern shifts without adding more containers.

The lost-cash risk goes away. The dollars are insured. The access-friction problem goes away because both spouses can have cards tied to shared accounts.

The envelope insight was right; the medium can finally catch up.

This is the Compass Method, the cash flow system built on this exact graduation. The principle the envelope system defended (every dollar has a job; the balance is the answer; the decision happens before the purchase) is preserved in full. What changed is the technology. Cash worked when cash was how most of America paid for things. The bank account works now because the bank account is how most spending actually moves through a household.

Same Household, Two Versions

The clearest way to see the upgrade is to run the same household through both versions of the system.

Imagine a household paid biweekly. Both spouses work. The variable spending categories are Groceries, Gas, Dining, Household, Personal Care, Entertainment, and Gifts.

The envelope version: On payday, one spouse drives to the bank, withdraws roughly $500 in cash, and distributes it into seven labeled envelopes in a kitchen drawer. The grocery trip on Saturday pulls from the Groceries envelope. The Wednesday gas fill-up pulls from the Gas envelope. The Friday dinner out pulls from the Dining envelope. When the Personal Care envelope empties on day eight, that category is done until the next payday. The Amazon order on day eleven runs against the checking account because cash cannot do Amazon, and the household either pulls the corresponding amount from the relevant envelope back into checking after the fact (workaround) or accepts that the Amazon line item lives outside the envelope system (leak).

The bank-account version: On payday, the same household opens the bank app and routes the deposit by pre-set percentages to accounts named Essentials, Lifestyle, Emergency, and Milestone. The Essentials account autopays rent, utilities, insurance, and the grocery debit card pulls from there. The Lifestyle account funds the Dining, Entertainment, and Personal Care decisions through a debit card tied to that account. The Amazon order runs from the Lifestyle account. The grocery trip runs from Essentials. The decision at the register is the same as the envelope version: is there enough in this account for this purchase? The friction of converting cash, the workaround for online purchases, and the second spouse’s access to envelopes all disappear because the account is the envelope, the balance is the truth, and the card carries the structure to wherever spending happens.

Same purposes. Same household. Same dollars. Different containers. The bank-account version handles everything the envelope version handles, plus the things the envelope version could not.

Your Next Step

If you have never tried envelope budgeting, the answer is not to start with paper envelopes in 2026. The answer is to run the modern version from the beginning. The principle is what made envelope budgeting work; the cash was always just the delivery mechanism.

If you have run envelope budgeting and it worked during a tight stretch, the next step is to keep the structure that earned its place and upgrade the container. The friction you ran into (the cash withdrawal, the online purchase workaround, the envelope sprawl) was never your fault. The medium had limits. The bank account does not have those limits.

The next read is What a Cash Flow System Actually Does. It walks through the system itself, with separation by purpose and balance as feedback, at the level the modern envelope version actually operates. For the broader picture of why every budget runs into the same architectural wall, see the architecture-not-discipline thesis.

Fix the cash flow first. Everything else gets easier.

Build the Modern Envelope System With Your Real Numbers

The Diagnostic Review inside the Millionaire Veteran community walks you through your actual income and obligations, then calibrates the routing percentages to your real numbers. The modern envelope system, built for your household, with an AI advisor that uses your real obligations to set the structure. Not a template. The community is free.

About the Author

Joshua Breaux

Retired U.S. Marine

Financial Management Analyst

BS & MBA in Analytics

His family runs on the same systems he teaches here.

This content is educational and does not constitute personalized financial advice. Millionaire Veteran is not affiliated with the Thrift Savings Plan, FRTIB, or the U.S. Government. Past performance does not guarantee future results.