The vehicle registration bill shows up every year on the same month. You know the amount within a few dollars. And it still lands like a surprise, because the money to cover it was sitting in the same checking account as the rent, the groceries, and everything else, and everything else got to it first. That gap between a cost you saw coming and a cost you actually had money for is exactly what a sinking fund closes.

A sinking fund is money you set aside on a schedule for a known, irregular cost so that the cost is already paid for when it arrives. Not a monthly bill. The once-a-year, every-few-months, you-know-it-is-coming kind of cost. This article walks through what a sinking fund is, how to run one, how it differs from an emergency fund, and why a real account beats a labeled category every time.

What a Sinking Fund Is

A sinking fund is a pool of money you build up a little at a time for a specific cost that is coming but is not part of your monthly bills. You name the cost, estimate the amount, divide by the number of months until it is due, and move that slice aside every payday. By the time the cost lands, the money is already there. You pay it and move on.

The math is the easy part. Say a cost runs $600 once a year. Split across twelve months, that is $50 a month. A bill that feels like a gut punch when it arrives all at once becomes a $50 set-aside you barely notice. The cost did not change. The timing of how you funded it did. That is the entire mechanism, and it is the reason a sinking fund works for people who have never managed to save any other way. You are not asking yourself to come up with $600 in a hard month. You handled it a slice at a time, months ago, when the slice was small.

People run sinking funds for the costs that wreck a normal budget precisely because they are not monthly. Annual vehicle registration. Insurance premiums paid every six or twelve months. Holiday spending. Replacing worn gear and boots before they fail. A reenlistment-leave road trip you already know you are taking. The annual eye exam. None of these are emergencies. You can see every one of them coming. The problem was never that they were unpredictable. The problem was that the money for them lived in the same place as the money for everything else, where it got spent on whatever was in front of you that week.

That is the whole idea. You decide in advance, fund on a schedule, and the predictable cost stops being a crisis. By the time the bill arrives, the money has been waiting for weeks, so paying it is a single transfer rather than a scramble, and the month absorbs it without flinching.

Sinking Fund vs Emergency Fund

This is where people get tangled, so it is worth being precise. A sinking fund and an emergency fund do different jobs, and confusing them is how both end up empty.

A sinking fund is for costs you know are coming. You can name them and you can roughly date them. Registration in March. The premium in July. Gifts in December. The amount is knowable and the timing is knowable. You are not reacting to anything. You are pre-paying a future you can already see.

An emergency fund is the opposite. It is a buffer for costs you cannot predict at all. The transmission that fails on a Tuesday. The medical bill nobody scheduled. The stretch where income shape changes and the deposits do not look like they used to. You do not know the amount and you do not know the date, which is the entire reason the money has to be sitting there before you need it. Common guidance puts an emergency fund at three to six months of essential expenses, and that range exists because nobody can forecast a true emergency down to the dollar.

Here is why the distinction matters in practice. When both jobs are funded from the same pile, the planned cost raids the buffer. You dip into the emergency money to cover the registration because the registration is due and the emergency money is what is available. Now the registration is paid and the buffer is gone, and the next actual emergency finds an empty account. Then a real shock lands a month later, and you are reaching for a credit card to cover the thing the emergency fund existed to cover. The fund did its job on paper. It just was not there when the job came up, because a predictable cost ate it first.

Two different jobs need two different places. One is planned. One is protection. A sinking fund drains to zero on purpose, every time the cost it was built for arrives, and then it refills for the next cycle. An emergency fund is supposed to sit untouched for months or years, and the day you use it is the day something went wrong. Funding them from one balance forces them to compete, and the predictable cost wins that fight every time because it has a due date and the emergency does not have one yet. Keep them apart and each one can do what it is for.

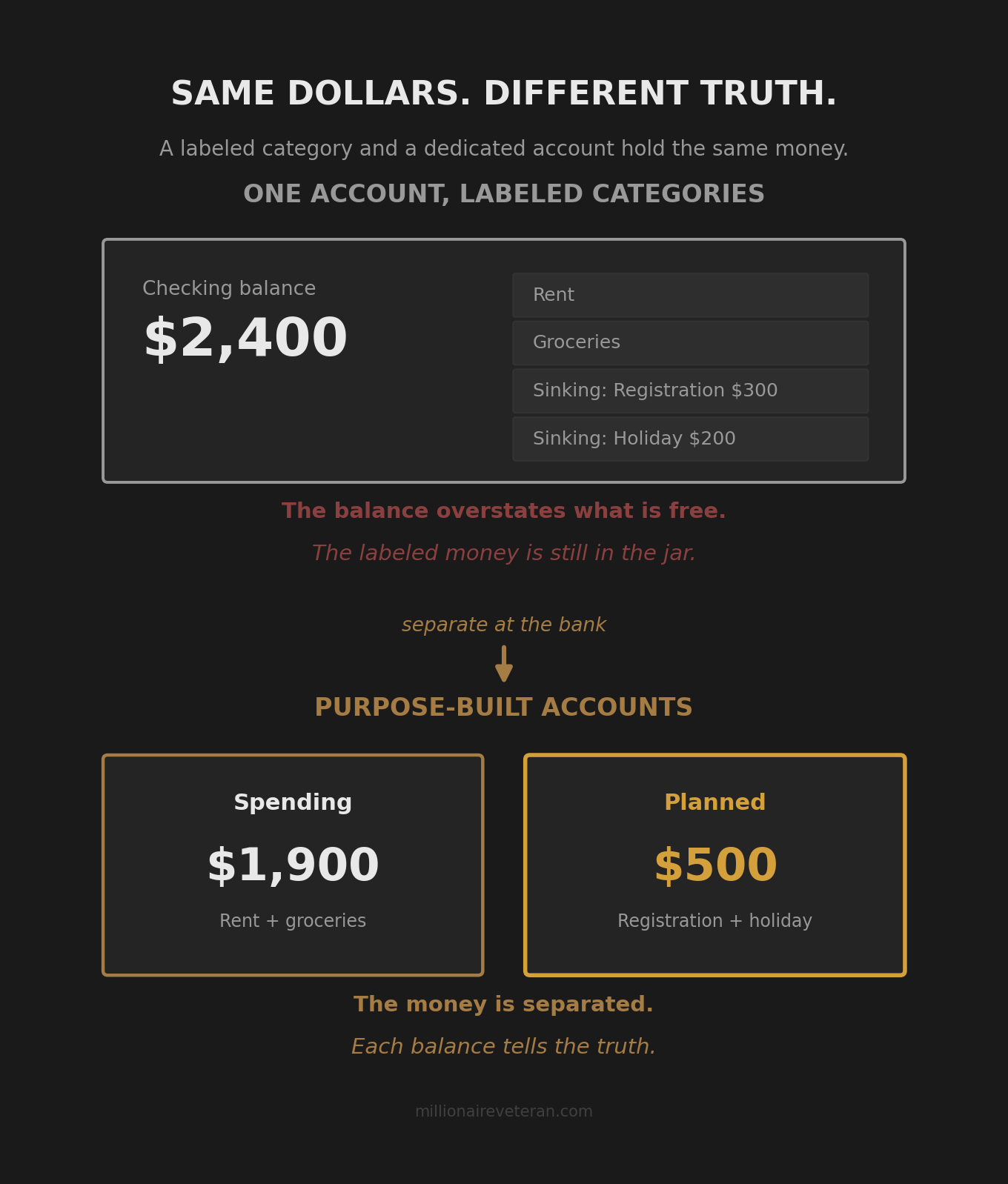

Why a Tracked Category Quietly Fails

Most budgeting tools will let you create a sinking fund without opening anything new. You make a category, you label it, you assign it a target, and the app shows you a tidy little progress bar. It looks like separation. It is not.

The money is labeled, but it is not separated. It is still sitting in one account, in one balance, next to the rent money and the grocery money and the gas money. The label exists only inside the app. The bank does not know about it. Your debit card does not know about it. The balance you see when you check your account includes the registration money, the holiday money, and the rent money all stacked together, which means the balance overstates what is actually free. Part of that number is already spoken for by a label only you can see.

So a tight week arrives. The account shows more than there really is, because the sinking-fund money is hiding inside the total. You spend against the number you see. The labeled money gets used, not out of carelessness, but because nothing physically stops it. A category is a sticky note on a shared jar. It works right up until someone reaches into the jar, and the someone is usually you, on a Thursday, with a number on the screen that looked fine.

This is the same failure the pooled account always produces. One balance cannot tell you what is available for each separate purpose. It can only tell you the total, and the total lies by including money that belongs to four different jobs. It is the same reason budgets keep breaking when they lean on willpower instead of structure.

A sinking fund is just separation by purpose with a deadline attached.

A label inside one account delivers the deadline without delivering the separation. Half the tool is missing, and it is the half that does the work.

The Better Medium: A Dedicated Account

The fix is not more discipline. The fix is a better container. Move the sinking fund out of the label and into its own account.

When the money sits in a separate, purpose-built account, the balance in your spending account finally tells the truth, because the sinking-fund money is no longer hiding in it. And the sinking-fund balance grows untouched, because it is somewhere your daily spending does not reach. You are not trusting yourself to honor a sticky note anymore. The bank is holding the line for you. Same dollars, different container, completely different result.

This is separation by purpose at the bank level, and it is the principle behind what a cash flow system actually does. The Compass Method, the cash flow system taught across this site, builds the whole structure on exactly this idea: money divided into purpose-built accounts so each balance answers one question honestly. Within that structure, your sinking funds have a home. It is called the Planned account, and it holds the known future spending that lands more than a month out: the vehicle costs, the travel, the gifts, the gear. The Planned account is the sinking fund concept given a permanent place to live.

Order still matters. The essentials come first. The essentials that cannot wait get funded at the front of the line, before anything discretionary. Once the must-pay obligations are covered, the planned set gets funded on its schedule. You are not choosing between rent and the registration fund. You are funding rent, then feeding the registration fund a slice at a time so it is full when March comes.

How to Run Your Sinking Funds Without Tracking

Running a sinking fund well takes almost no ongoing effort, which surprises people who are used to budgeting apps demanding daily attention. The effort is front-loaded into two decisions. After that, the account balance does the reporting.

First, pick the costs. Look at the year and name the predictable, irregular ones. Registration, premiums, holiday spending, gear replacement, the trip you already know about. You do not need to catch every possible cost on day one. Start with the few that have burned you before.

Second, size each one. Take the cost and divide it by the number of months until it is due. That is your per-month set-aside. If a cost is due in four months, you are funding it faster than one due in twelve. The arithmetic is honest and it is the same every time: cost, divided by runway, equals the slice.

Then route the slice on payday, once, into the purpose-built account, and stop watching it. There is no category to reconcile and no app to update. The account balance is the status. When the cost arrives, you check the account, the money is there, you pay it. The work was the decision and the routing. The maintenance is close to zero, because the balance does the reporting for you.

How many sinking funds you run is a personal call, not a rule. Some people keep one combined planned account and track the costs in their head. Some split it further. Both work, because the principle is the same in either case: the money is separated where you cannot spend it by accident, and the balance tells you the truth.

Your Next Step

A sinking fund is one application of a single idea: separate money by purpose, and the balance stops lying to you. That idea does not have to stop at the costs you can see coming. It works just as well for your essentials, your everyday spending, and your emergency buffer, when every dollar gets the same account-level separation the sinking fund just earned.

That is the full picture behind what a cash flow system actually does, the system that gives every dollar the same truth-telling separation the sinking fund just earned. The sinking fund is a clean place to start, because once you feel a predictable cost arrive already paid for, you stop wanting to run any of your money any other way. Fix the cash flow first. Everything else gets easier.

Build Your Planned Account With Your Real Numbers

The Compass Method setup inside the Millionaire Veteran free community walks you through the six-account structure, including the Planned account where your sinking funds live, using your actual take-home pay and the actual costs you know are coming. The AI advisor inside the community calculates each per-payday set-aside from your real numbers, so the account is full when the bill lands instead of guessed at. The community is free and there is nothing to buy.

About the Author

Joshua Breaux

Retired U.S. Marine

Financial Management Analyst

BS & MBA in Analytics

His family runs on the same systems he teaches here.

This content is educational and does not constitute personalized financial advice. Millionaire Veteran is not affiliated with the Thrift Savings Plan, FRTIB, or the U.S. Government. Past performance does not guarantee future results.