Coast FIRE is the milestone where your invested balance is large enough that, with no further contributions, compounding alone will grow it to your full retirement number by the time you actually retire. Once you cross that point, you no longer have to invest aggressively. You still have to cover your current living expenses from some income source, but the retirement account compounds without any further contributions from you. It grows. You coast.

That is the canonical definition. The number itself, your personal Coast FIRE number, depends on three inputs: your target retirement balance at traditional retirement age, your expected real annualized return between now and then, and the number of years between today and that target retirement.

The article walks through what Coast FIRE actually is, what makes it work, and where the math gets stuck for most civilian readers. Then it shows why the math is structurally different for military families. The pension, VA disability, and TRICARE stack covers the one assumption that civilian Coast FIRE almost always handwaves: the floor income that has to cover your living expenses while the retirement account compounds on its own.

I am writing this from the position of a retired Marine who has run these numbers for my own household and for other military families inside the Millionaire Veteran community. The framework below is general. The specific dollar figures are illustrative. Verify your own numbers against your actual pension projection from DFAS, your actual VA disability if applicable, and your actual TSP and IRA balances before treating any of this as a plan.

What Coast FIRE Actually Is

Coast FIRE sits inside the larger Financial Independence (FI) framework as a midpoint, not a destination. The full FI number is the balance that, at a safe withdrawal rate, generates enough income to cover your expenses for life. Coast FIRE is the smaller balance, earlier in the journey, that compounds without further contributions to reach the full FI number by traditional retirement age.

The math runs in reverse from the full FI number. Pick a traditional retirement age, often 65. Pick your full FI number at that age. Pick a real annualized return assumption, commonly 7% for an equity-weighted long horizon. Then discount backwards: present balance equals future FI number divided by (1 + r) raised to the number of years between now and target retirement.

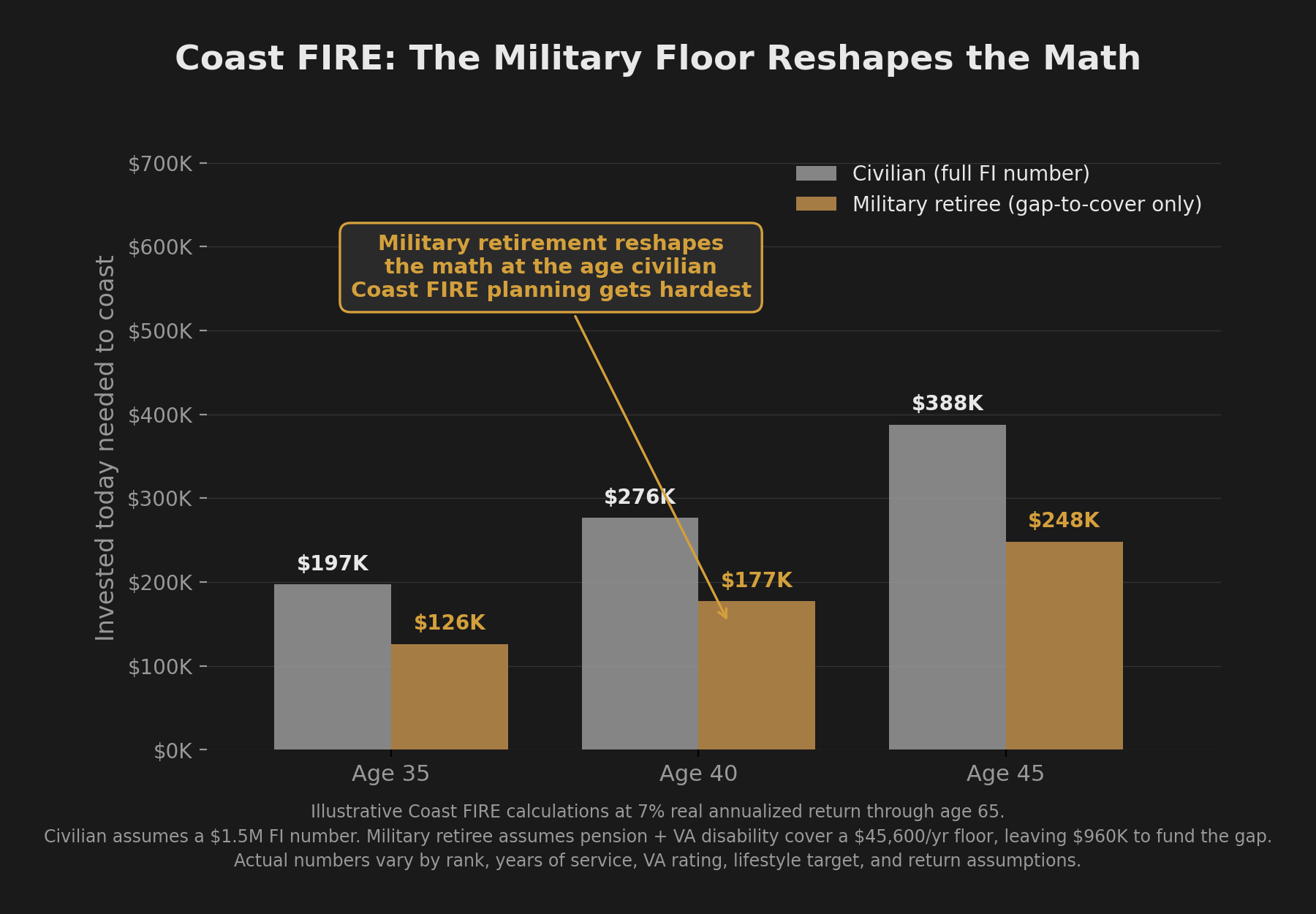

A concrete example helps. Assume a full FI number of $1.5 million at age 65, a 7% real annualized return, and a current age of 35. Thirty years of compounding at 7% real means each dollar invested today becomes about $7.61. The Coast FIRE number is $1.5 million divided by 7.61, or approximately $197,000. If you have $197,000 invested at age 35 and you never contribute another dollar, the projection has you reaching $1.5 million by age 65.

That is the math people mean when they say “I hit Coast FIRE.” They hit the balance that will compound itself to the full FI number without further additions. They can stop investing for retirement. They are still working, in most cases, because they still have current living expenses to cover. The retirement account is just no longer demanding new contributions.

The assumption hiding inside that paragraph is the one civilian Coast FIRE writing rarely solves. Where does the income to cover current living expenses come from while the retirement account compounds on its own?

The Floor Income Problem in Civilian Coast FIRE

Most civilian Coast FIRE content gestures at the floor income question with three options. Each one is real. Each one carries friction.

Find a less stressful job. Real. Also usually means a pay cut, which affects current lifestyle, savings rate for non-retirement goals, and any debt the household still carries. The job market access required to make this transition cleanly is itself a constraint. Industries that pay well are not always industries that have lower-stress versions of the same role.

Switch to part-time work at the current employer. Real. Often comes with the loss of employer-sponsored healthcare, which is the single biggest variable for pre-Medicare-age households. Healthcare premiums on the individual market routinely run higher than a mortgage, whatever the household size. Part-time work that triggers loss of employer health coverage can flip the household budget on its own.

Pursue passion work for lower income. Real. Income is uncertain, healthcare is unsolved, and geographic constraints often apply. The freelance writer in Manhattan and the freelance writer in rural Montana face the same federal tax structure but radically different cost-of-living math.

The unsolved problem under all three options is healthcare and floor income simultaneously. The Coast FIRE math works cleanly on a spreadsheet. The implementation friction is the floor-income question, and most civilian articles either skip the question or assume the reader will figure it out.

Why Military Coast FIRE Is Structurally Different

For service members who retire from active service after twenty or more years, the floor income calculation looks fundamentally different.

The military pension and VA disability cover the floor Coast FIRE assumes you have to build.

Three pieces stack together and address the exact three variables that break civilian Coast FIRE plans.

The pension. Inflation-adjusted lifetime income, paid through the rest of your life regardless of any other income you have or do not have. The amount depends on years of service, the High-3 average for High-3 retirees, the BRS multiplier for those who entered under the Blended Retirement System, and whether any survivor benefit elections reduce the gross. The pension is the floor that civilian plans have to construct from scratch. It is already there for the retiree.

VA disability, where applicable. Tax-free lifetime income at the rated percentage, paid through life. VA disability compensation does not reduce the pension. The two stack. For a retiree with a service-connected disability rating, the VA monthly compensation lands on top of the pension as additional tax-free floor income. The exact figure depends on the rating and the family size, and the VA compensation tables are updated annually.

TRICARE for retirees. Healthcare access at premiums dramatically below civilian retiree healthcare costs. The single biggest pre-Medicare expense variable for civilian households is mostly resolved structurally for military retirees. TRICARE is not free, but the cost surface is bounded and predictable in a way the individual marketplace is not.

Stacked together, these three address floor income, longevity, and healthcare in one structural package. The military retiree at age 40, fresh off twenty years of service, does not need to “find” floor income to enable Coast FIRE. The pension is the floor. VA, where applicable, adds to it. TRICARE bounds the healthcare variable. The Coast FIRE conversation can then move past the floor-income question and back to what it was supposed to be: how much do I need invested today so it compounds to cover the gap between my floor and my desired retirement lifestyle.

The Military Coast FIRE Math

A concrete illustrative example shows the calculation in action. Every number below is illustrative. Run yours against actual DFAS pension projections and the current VA disability tables before relying on the framework.

Take an E-7 retiring at age 40 with twenty years of service. The illustrative monthly pension lands somewhere around $2,600 a month, depending on the High-3 average and whether the retiree is under BRS or High-3. Assume a VA disability rating of 50%, which puts the monthly VA compensation around $1,200 a month under current tables. Floor income from those two sources: $3,800 a month, or $45,600 a year. TRICARE bounds the healthcare exposure on top of that.

Assume the same retiree wants a retirement lifestyle at age 65 that costs $7,000 a month, or $84,000 a year, in today’s dollars. The pension and VA continue paying through retirement (with inflation adjustments for the pension portion). The gap between the floor and the desired lifestyle is $84,000 minus $45,600, or $38,400 a year.

Applying the 4% safe withdrawal rate convention, the invested balance required at age 65 to generate $38,400 a year is $38,400 divided by 0.04, or $960,000. That is the FI number specific to this retiree’s situation, and it is meaningfully smaller than the $1.5 million number civilian Coast FIRE writing tends to default to.

Now run the Coast FIRE math on that $960,000 number. Twenty-five years from age 40 to age 65 at 7% real annualized return compounds each dollar to about $5.43. The Coast FIRE balance required at age 40 is $960,000 divided by 5.43, or approximately $177,000.

At age 40, with $177,000 in TSP and IRA balances combined, this illustrative retiree could stop contributing to retirement entirely and the projection has the balance closing the gap to $960,000 by age 65, on top of the pension and VA continuing to pay the floor. The retiree is at Coast FIRE the day the career ends.

The framework is the takeaway, not the specific dollar amount. The number changes with rank, years of service, VA rating, lifestyle target, and return assumptions. The structural point is that the floor income built into military retirement reshapes the Coast FIRE calculation at the exact career stage when civilian Coast FIRE planning gets hardest.

Where Coast FIRE Sits on the FI Spectrum

Coast FIRE is one stage on a broader spectrum that runs from financial survival through complete financial independence. The framework that orders the stages is the FI Spectrum, which lays out five stages: Surviving, Stable, Building, Coasting, and Fully Independent. Coast FIRE corresponds to Stage 4, Coasting. Stage 4 is the target. The harder question the spectrum answers is which stage you are standing at right now, and until you know that, the Coast FIRE math stays theoretical.

For military families, Stage 4 often arrives earlier than for civilians. The pension reduces the gap to the full FI number. Some military retirees effectively land in Stage 4 the day they retire, depending on how much they accumulated in TSP and IRA balances during the career and the gap between their pension and their desired lifestyle. Others land closer to Stage 3 (Building) at retirement and reach Coasting a few years into the retirement-job phase. The position on the spectrum depends on the inputs, not on rank or any single career variable.

The compounding math underneath all of this is the same math covered in the Millionaire Veteran math article on what it actually takes to reach seven figures on military pay. The Coast FIRE calculation is the same compounding math run in reverse from a smaller target number. Understanding one helps understand the other.

Your Next Step

The Coast FIRE calculation in the prior section uses one illustrative example. The actual numbers for any individual reader depend on their pension projection, their VA situation if applicable, their lifestyle target, their accumulated balances, and the return assumptions they want to use. The full FI Spectrum framework places those inputs in context: what stage you are currently in, what stage is next, and what milestone defines the move between them.

The specific calculation of your personal Coast FIRE number, with your real pension projection, your VA rating, and your accumulated balance, is the next layer down from this article.

The wedge to carry forward is this. The military version of Coast FIRE arrives earlier than the civilian version because the floor income is built into the career rather than constructed from scratch. The math that follows from that structural advantage often surprises readers who assume Financial Independence is for people who joined a Silicon Valley startup at twenty-two.

Two pieces sit upstream of any Coast FIRE calculation and quietly determine whether the math works at all. The first is the accumulation work that happens during the career. The Coast FIRE number is meaningful only if the actual TSP and IRA balances reach it in time, which requires consistent contribution behavior across the years before the projection compounds the rest of the way home. The second is the contingency planning for the assumptions baked into the math. Returns can underperform the 7% real assumption for stretches. VA ratings can change. Lifestyle targets shift. The Coast FIRE calculation is a planning tool, not a guarantee, and treating the projected number as a finish line ignores the work of maintaining the underlying assumptions until the projection actually plays out.

Find Out Where You Sit on the FI Spectrum

Millionaire Veteran is a free community where military families put their real numbers on the Azimuth Roadmap: rank, take-home, contributions, and current TSP and IRA balances. The Diagnostic Review shows which FI Spectrum stage you are actually in and the next milestone to clear. It is a placement, not a Coast FIRE calculator or a TSP fund prescription. The Compass Method then routes the cash flow so the contributions actually leave the paycheck on payday, every payday.

About the Author

Joshua Breaux

Retired U.S. Marine

Financial Management Analyst

BS & MBA in Analytics

His family runs on the same systems he teaches here.

This content is educational and does not constitute personalized financial advice. Millionaire Veteran is not affiliated with the Thrift Savings Plan, FRTIB, or the U.S. Government. Past performance does not guarantee future results.