The name Millionaire Veteran sounds like clickbait. It is a compound interest calculation.

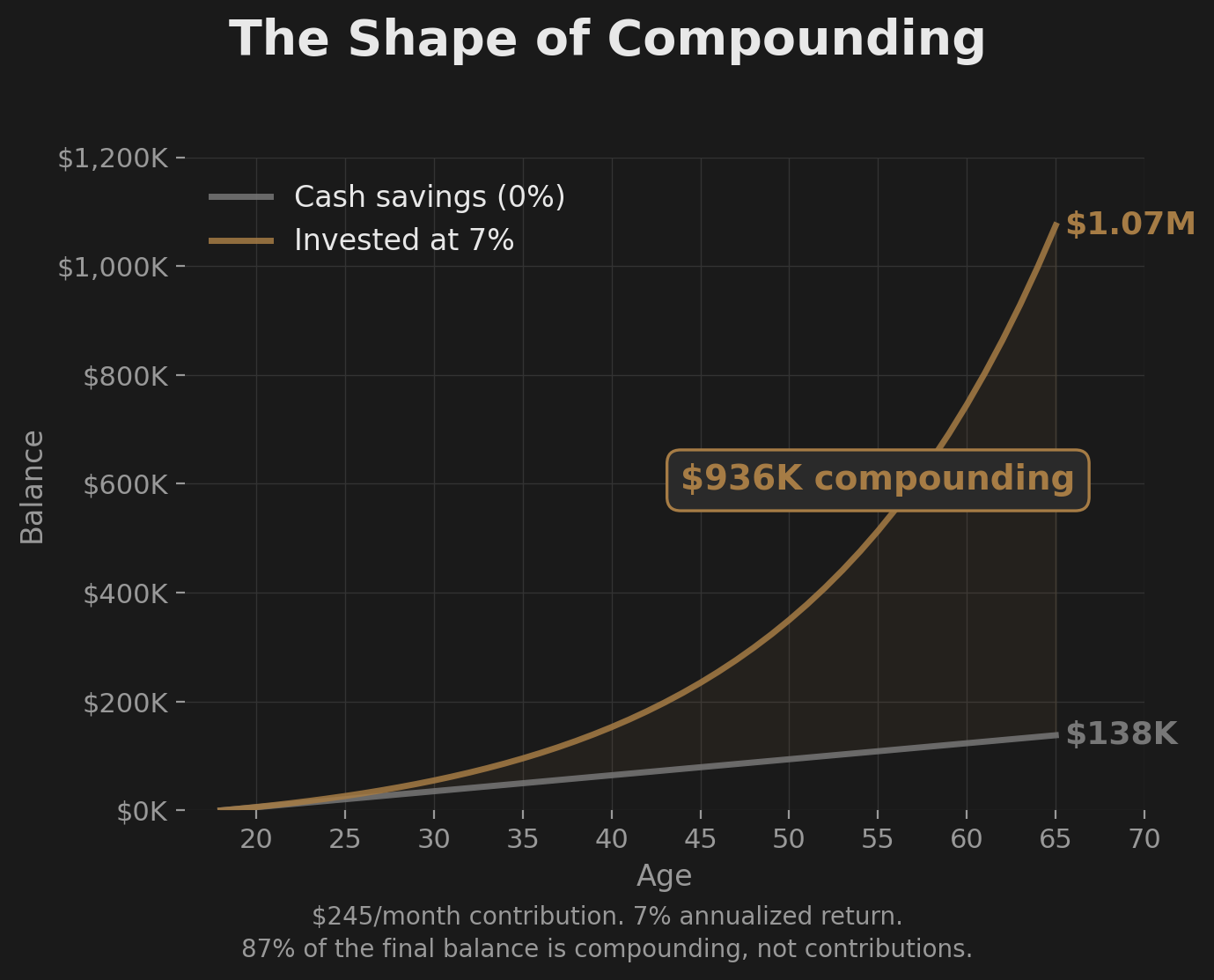

An 18-year-old service member who invests $245 per month at a historical average return of 7% would accumulate over $1,000,000 by age 65. Total out-of-pocket contributions over those 47 years: approximately $138,000. The other $862,000 is compounding. The investor contributed 13% of the final balance. Time and growth produced the rest.

That is the standard compound interest formula applied to a number most enlisted members can free up from a single paycheck.

This article is the baseline proof. A demonstration that the compounding engine works at military pay levels, starting with $245 per month.

The Shape of Compounding

Numbers on a page are one thing. The shape of growth over time tells a different story.

If you plot $245 per month at 7% over 47 years, the first decade looks flat. The line barely separates from someone who stuffed the same cash under a mattress. At age 28, both balances are close enough that the difference feels academic.

Then the crossover point hits around age 28. Annual growth on the invested balance starts exceeding annual contributions. From that point forward, compounding contributes more each year than the investor does. The gap between the two lines widens without anything changing about the investor’s behavior.

The first $500,000 took 37 years to build. The second $500,000 took 10.

Same person. Same $245 per month. Same 7%. The only variable was time.

By age 64, the portfolio’s expected annual growth is roughly $70,000. The invested capital is producing income-level returns without additional contributions. That is what people mean when they talk about the time value of money. A dollar today has more opportunity than a dollar later, because it has more runway to compound.

Most people quit before the curve bends. The quiet risk is not a market crash. It is giving up during year eight because the balance looks the same as a savings account and the whole thing feels pointless.

“But What About My Situation?”

The $245 per month case study is a baseline, and baselines invite questions. Fair. Here are the ones that come up most.

“I am older than 18.”

The math still works. Your starting point changes your personal graph, not the principle. An E-5 at 26 has different numbers than a private at 18. The curve is shorter and steeper, which means contributions matter more and time matters differently. But compounding still does the heavy lifting in every scenario where the timeline exceeds 15 years.

“I want more than $1,000,000.”

Good. The case study used $245 per month because it is a number most service members can reach. The actual contribution targets for maxing all tax-advantaged accounts are significantly higher. A million dollars is the floor of what is possible on military pay, not the ceiling.

“I want it before 65.”

That is the entire point. The approach is not “contribute $245 per month and wait half a century.” The approach is: define what you want your future to look like, then backwards-plan from there. Higher contributions, earlier start, or both compress the timeline. The math is the same engine. The inputs are yours.

“$245 per month for 47 years sounds impossible to maintain.”

Nobody is asking you to lock in $245 forever. The case study proves that even a small, fixed contribution produces a massive result over time. Your actual contributions will change as rank, income, and life circumstances change. Some years you will contribute more. Some years you will contribute less. Compounding does not require perfection. It requires consistency.

The Military Advantage

Most personal finance content is written for civilians. It assumes employer-matched 401(k) plans with high expense ratios, no pension, no guaranteed healthcare, and a career path with no predictable pay trajectory. Your financial environment looks different.

TSP. The Thrift Savings Plan is one of the lowest-cost retirement vehicles in the country. Expense ratios that civilian 401(k) holders pay ten times more for. The investment options are simple, diversified, and institutional-grade.

BRS matching. The Blended Retirement System provides automatic and matching contributions up to 5% of base pay. That is an immediate positive return before the market does anything. For a deeper look at how BRS changed the retirement calculation, the Invest Smarter series covers the full mechanics.

Predictable pay trajectory. Military pay increases with rank and time in service on a published schedule. You can project your income five years out with reasonable accuracy. Most civilians cannot do that. That predictability makes backwards-planning from a contribution target possible in a way that most career paths do not allow.

Pension. The BRS pension at 20 years pays 40% of the average of your three highest years of base pay, for life. That income stream reduces how much your investment portfolio needs to produce. A military retiree with a pension needs a smaller portfolio to cover the same lifestyle as a civilian with no pension.

VA disability. Tax-free lifetime income for service-connected conditions. This is not something to plan around, but for those who qualify, it is a significant financial floor that most retirement calculators do not account for.

TRICARE. Healthcare cost uncertainty is one of the largest retirement planning variables for civilians. Military retirees and their families retain access to TRICARE. That removes a variable that derails civilian retirement plans regularly.

These advantages are structural, not theoretical. They show up on your LES every pay period. The question is whether you are using them or letting them sit there.

The Real Target: Max Your Tax-Advantaged Accounts

The baseline proof used $245 per month. That is $2,940 per year. The actual target is significantly higher.

TSP allows $24,500 per year in elective deferrals (2026). A traditional or Roth IRA allows $7,500 per year per person. For a married service member with a spouse, that is $24,500 plus $7,500 plus $7,500 in spousal IRA contributions: $39,500 per year in tax-advantaged space. Plus the BRS match on top.

That is the real destination. Not $245 per month. The full capacity of every tax-advantaged container available to you.

Why max everything? Because this target is the first checkpoint where the numbers work in real life. Getting there is the forcing function that makes the rest of the system self-evident.

To free up $3,000 or more per month for retirement contributions, you have to eliminate high-interest debt. You cannot service 22% credit card balances and max your TSP at the same time. The math fights itself.

To eliminate debt and keep it gone, you need a cash flow system that prevents new debt from forming. Money needs to be routed on arrival, not managed by memory at the end of the month. That is what the Spend Less domain covers in depth.

To close the gap between your current contributions and the max, you may need income beyond base pay. Military pay has a ceiling. If the gap between take-home and full contribution targets is wider than what you can cut, additional income is the only remaining lever. The Earn More series breaks down exactly where that ceiling is.

The system builds itself backwards from this target. The milestones in the roadmap (covered in a later article in this series) are the sequence for getting there. Each milestone clears a gate that makes the next one possible.

The asymmetric hedge. Front-loading retirement accounts is the safer bet. Your vision of the future will change. It always does.

If your future vision gets simpler over time, you overshoot. You end up with more saved than you needed. That is a problem everyone wants to have.

If you start conservatively and your future vision later requires more, you cannot get back the compounding time you lost. A family that grows, a spouse who stops working, a health condition that changes your cost structure, a child’s education needs. These are real. And the math is unforgiving in one direction: you can always spend less of what you saved, but you cannot go back and save more during years that already passed.

If you save more than you needed, you have options. If you save less, you cannot recover the compounding years you missed.

The Time Variable

Every year of delay costs more than the year before it. Not as a guilt trip. As a compounding formula applied to inaction.

A 20-year-old who invests $500 per month at 7% would have approximately $1,900,000 by age 65. A 25-year-old investing the same $500 per month would have approximately $1,300,000 by age 65. Five years of delay cost roughly $600,000 in final balance. The contributions difference between those two scenarios is $30,000. The compounding difference is $570,000.

That ratio matters. Thirty thousand dollars of actual money produced over half a million dollars of difference, purely because of when it was invested. The dollars themselves are identical. The timing is not.

The E-2 reading this right now has the single biggest advantage in this entire article: time. Every month of contributions at 18 or 19 is worth more than every month of contributions at 35. Not because the dollars are different, but because they have more runway to compound. An E-2 who starts putting $200 per month into the C Fund in their first year of service is doing something that no amount of catch-up contributions at E-7 can fully replicate.

The E-6 reading this wishes they had started at E-2. But the math does not punish late starters as harshly as people fear. Starting at 30 with higher contributions and a clear system still produces results that most Americans never achieve. The median retirement savings for Americans aged 55 to 64 is roughly $185,000. A military family that starts investing seriously at 30 and maintains discipline through a 20-year career will exceed that number significantly, especially with BRS matching and a pension floor underneath them.

The earlier you start, the less each month has to carry. The later you start, the more each month matters. Both paths can work. One is easier. Neither is impossible.

The real cost of delay is options. Every year of compounding you capture is a year of future flexibility. Every year you miss narrows the range of outcomes available to you. How many options do you want to have at 45? At 55? That is the question the numbers are answering, whether you run them or not.

What Comes Next

$245 per month and $39,500 per year are very different starting points. Most people reading this are not currently maxing every tax-advantaged account. The gap between where you are and where the full contribution targets sit is real, and it is probably wider than you want it to be.

That distance looks different for everyone. A family with two car payments and a credit card balance is in a different position than a dual-income household with no debt. A first-termer contributing 5% to TSP is in a different position than a senior NCO already maxing their IRA. The formula is the same for all of them. The starting line is not.

The next article in this series maps out where you are right now. The path forward looks different depending on whether you are covering the basics, building stability, or already watching the compounding curve start to bend. There are recognizable stages, and each one has a different set of next moves.

Start With Your Real Numbers

You have seen the math. You know the targets. The question is where you stand relative to them.

The free Millionaire Veteran community includes the Diagnostic Review, which places you on the roadmap with your actual numbers. Your rank, your take-home, your current debt load, your existing contributions. From there, the system walks you through what to do first, what to do next, and why that sequence matters for your specific situation.

No guesswork. No generic advice. Your gap, your sequence, your next milestone.

About the Author

Joshua Breaux

Retired U.S. Marine

Financial Management Analyst

BS & MBA in Analytics

His family runs on the same systems he teaches here.

This content is educational and does not constitute personalized financial advice. Millionaire Veteran is not affiliated with the Thrift Savings Plan, FRTIB, or the U.S. Government. Past performance does not guarantee future results.