The previous article in this series proved a point: $245 per month at 7% produces over a million dollars. The compounding engine works at military pay levels.

But here is the part that article left open. It showed the destination without asking the harder question: where are you starting from?

A first-termer with $800 in checking and a Charger payment is not in the same position as a senior NCO with a funded emergency account and 15% going to TSP. The formula is the same for both of them. The starting line is not. And the path forward from each of those positions looks completely different.

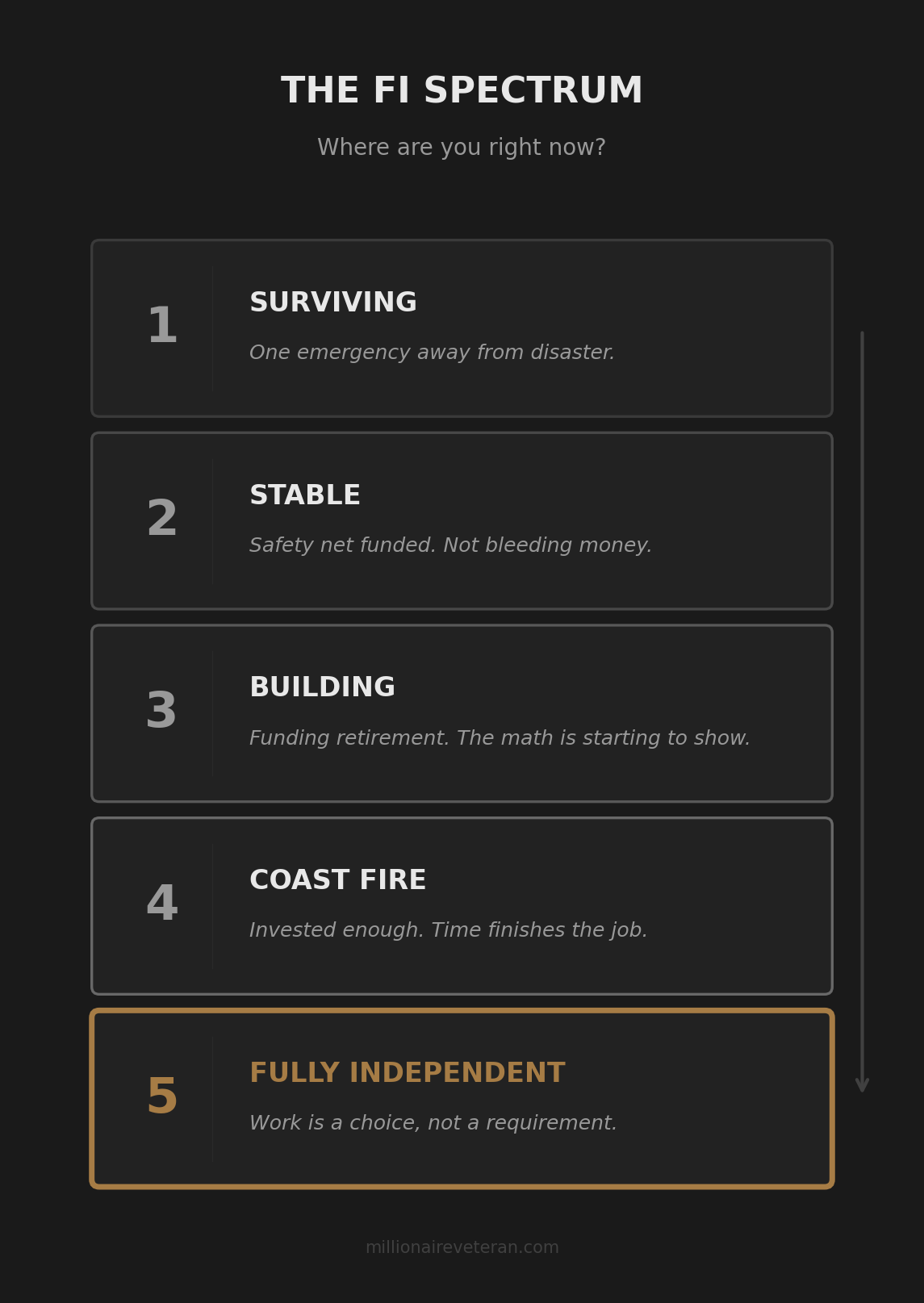

Financial Independence is not a single destination you either reach or fail to reach. It is a spectrum with recognizable stages. Most people are already somewhere on it. They just have not named where.

The All-or-Nothing Problem

Most people hear “Financial Independence” and picture someone retiring at 35 with a seven-figure portfolio and a lifestyle funded entirely by investment returns. That version exists. It is also the version that causes the majority of people to dismiss FI as irrelevant to their lives.

The logic goes: “I am not going to retire at 35. I do not make $200K. Therefore FI is not for me.”

Walk through any FIRE forum online and count how many posts come from software engineers comparing seven-figure portfolios. That is the visible face of the movement. If that is all you see, the conclusion writes itself: this is not your world.

It is your world. You are already on the spectrum. You just may not have a name for where you stand.

Stage 1: Surviving

“I just want to stop being one emergency away from disaster.”

Cash flow is negative or break-even. The checking account balance technically has money in it, but that money is already spoken for by rent, insurance, the car payment, and a dozen autopays that have not drafted yet. When something unexpected happens, it goes on a credit card. There is no buffer.

This is where most E-1 to E-3 families are. Take-home pay after taxes, SGLI, and TSP contributions often lands below $2,000 per month. Housing on-base keeps the roof covered, but everything else runs tight. A set of tires, a vet bill, a broken phone. Any of those can start a credit card balance that compounds in the wrong direction.

Income is low, expenses are real, and nobody handed you a system for routing money on arrival. The default is to manage it by feel, and managing by feel is how the gap between payday and next payday fills up with charges you cannot explain.

The exit from Stage 1 is not earning more or investing more. It is getting a cash flow system running so that every dollar routes to a purpose on the day it arrives. That is what the Spend Less domain covers in depth.

Stage 2: Stable

“I have a safety net and I am not bleeding money to interest.”

Emergency fund is funded. High-interest debt is eliminated or under a deliberate attack plan. Cash flow system is running. You know where your money goes because you decided where it goes before it arrived.

The floor is solid. You are not building wealth yet in any dramatic way, but you stopped the bleeding. The credit card balance is not growing. The checking account is not a mystery on the 14th. There is a buffer between you and the next surprise.

For most people at this stage, this is the first time they feel like they are in control rather than reacting. The household stress level drops. Conversations about money shift from “where did it go” to “where should it go next.”

Stage 2 is where a lot of people stall. The urgency that drove them to fix the bleeding fades once the bleeding stops. The balance is stable, the bills are covered, and the system is working. It feels like enough.

It is enough, in the sense that you are not in crisis anymore. But stability is not momentum. A funded emergency account and zero credit card debt puts you ahead of the majority of American households. It does not produce the compounding results from the previous article. Stage 2 is the foundation. What you build on it determines whether the numbers from that article ever show up in your accounts.

The temptation at Stage 2 is to relax the system. The Charger is paid off, the credit cards are clear, and there is breathing room for the first time in years. That breathing room is real and earned. The question is what happens next: does the freed-up cash flow get absorbed back into lifestyle spending, or does it get redirected into the contribution targets from Stage 3?

Stage 3: Building

“I am funding retirement accounts and the compounding is starting to show up.”

TSP match captured. Maybe an IRA opened. Contributions are consistent. The balance has crossed a threshold where the quarterly statements feel like they are moving, not sitting still.

This is the stage where the crossover math from the previous article starts to feel real. The portfolio’s growth in a good quarter starts approaching what you contributed. The curve has not bent yet, but it is no longer flat.

For the mid-career NCO who woke up at E-5 and started contributing seriously, Stage 3 is where the decision to start pays its first visible dividends. The balance at 32 is not going to retire anyone. But the trajectory is different from the person who is still at Stage 1 at the same age, and that trajectory gap widens every year.

Stage 3 is also where the gap between current contributions and the full tax-advantaged target from the previous article becomes concrete. You are contributing. But are you maxing? TSP at $24,500 per year, IRA at $7,500, spousal IRA at $7,500. That is $39,500 per year. If you are contributing $500 per month, you are at roughly a third of capacity. The distance between a third and full is the distance between a comfortable retirement and a fully independent one.

Closing that gap may require addressing income (the Earn More series covers exactly where the ceiling is) or restructuring how current income flows (the cash flow system from Stage 2 becomes the engine for Stage 3 contributions).

Stage 4: Coast FIRE

“I have invested enough that time finishes the job.”

Coast FIRE is an established concept in the financial independence community. The idea: you have invested enough, early enough, that even without additional contributions, compounding grows the portfolio to your target number by traditional retirement age. Your future is funded. Your present earnings only need to cover current expenses.

For military families, Coast FIRE has a structural advantage that civilians do not have. The pension.

A 20-year military retiree receives 40% of the average of their three highest years of base pay, every month, for life. Add VA disability if applicable. Add TRICARE. Those three income floors mean that a military retiree reaching Coast FIRE needs a significantly smaller portfolio than a civilian in the same position, because a large portion of future living expenses are already covered by non-portfolio income.

An E-7 who retires at 38 with a pension, VA disability, and $300,000 in TSP and IRA accounts is in a fundamentally different position than a 38-year-old civilian with $300,000 and no guaranteed income floor. The civilian needs that portfolio to grow to cover everything. The military retiree needs it to grow to cover the gap above the pension floor.

That is why the compounding math from the previous article is not theoretical for military families. The structural advantages compress the timeline and reduce the target.

Coast FIRE is not retirement. It is the point where the math is working for you even if you stop contributing. Some people at this stage keep working because they want to. Some pivot to lower-stress careers. Some start businesses they have been thinking about for years. The defining characteristic is that the financial pressure is gone. Work continues because the work is worth doing, not because the bills require it.

For a military family, Coast FIRE is often reachable within a 20-year career if TSP contributions start early and remain consistent. An E-6 who started contributing 15% of base pay at E-3 and captured the full BRS match may reach Coast FIRE before their retirement ceremony. The pension then becomes the living-expense engine, and the portfolio becomes the wealth-building engine, compounding untouched.

Stage 5: Fully Independent

“Investment income and guaranteed income cover everything. Work is entirely optional.”

This is the 25x expenses calculation. Take your annual spending, multiply by 25, and that is the portfolio target. The 4% withdrawal rate originates from the 1998 Trinity Study by Cooley, Hubbard, and Walz, which tested historical portfolio survival rates across 30-year periods. That withdrawal rate provides a sustainable income stream from the portfolio.

For military retirees, the 25x number is smaller than it is for civilians because the pension, VA disability, and TRICARE cover a significant portion of annual expenses. If your total annual spending is $60,000 and your pension plus VA covers $36,000, you only need the portfolio to produce $24,000 per year. At 4%, that is a $600,000 portfolio, not $1,500,000.

That is the military advantage applied at its fullest. The structural floor reduces the portfolio requirement. The TSP’s low expense ratios protect the growth. The predictable career trajectory allows backwards-planning from the target. Everything converges.

Full independence does not mean you stop working. It means the financial pressure to work is gone. What you do with your time becomes a decision based on interest, not obligation. Some people at this stage keep serving. Some start businesses. Some coach Little League five days a week. The point is that the decision is theirs.

Where Are You Right Now?

Not where you want to be. Where you actually are.

Most readers are at Stage 1 or Stage 2. That is where the numbers put the majority of enlisted families, and being honest about that starting point is more useful than pretending otherwise.

If you are at Stage 1, the next move is a cash flow system. Not investing advice. Not retirement planning. Not a budgeting app. Getting control of what is already coming in so that every dollar has a destination before it has a chance to disappear.

If you are at Stage 2, the next move is capturing the TSP match and starting to close the gap toward full contribution targets. The foundation is set. Now build on it.

If you are at Stage 3, the next move is identifying what is keeping you from maxing your tax-advantaged accounts and addressing that constraint directly, whether it is debt, income, or allocation decisions.

If you are at Stage 4 or 5, you already know what you are doing. The system is working. The remaining question is what you want to do with the options it created.

Every stage has a next move. And every next move connects back to the same three levers: how you manage cash flow, how you grow income, and how you invest.

The next article in this series explains why working on just one of those three levers is not enough, and how the three compound each other when they work together.

Find Your Stage With Real Numbers

Reading descriptions is one thing. Placing yourself on the spectrum with your actual take-home, your actual debt load, and your actual contribution rate is another.

The free Millionaire Veteran community includes the Diagnostic Review, which does exactly that. It takes your real numbers and maps them to the roadmap. From there, the system walks you through what to do first, what to do next, and why that sequence matters for your specific situation.

Your stage, your numbers, your next move.

About the Author

Joshua Breaux

Retired U.S. Marine

Financial Management Analyst

BS & MBA in Analytics

His family runs on the same systems he teaches here.

This content is educational and does not constitute personalized financial advice. Millionaire Veteran is not affiliated with the Thrift Savings Plan, FRTIB, or the U.S. Government. Past performance does not guarantee future results.