Military pay is predictable. Known pay tables, expected promotion timelines, built-in raises that show up on schedule. BAH adjusts with your base. BAS offsets food costs. The structure is real, and most civilian careers cannot offer anything close to it.

That predictability is an advantage. A significant one. This article is not going to undercut it.

But predictable does not mean unlimited. And the difference between “enough to live on” and “enough to fund everything” is where most military families find a gap they did not know existed.

One Piece of a Larger System

This article covers the income side of the equation. It is part of the Earn More domain in the Azimuth Framework, a three-part system built for military families:

- Spend Less controls what goes out. You get visibility into your cash flow, route every dollar by purpose, and stop the leaks that drain your accounts between paychecks.

- Earn More raises what comes in. That is what this article and the rest of the series are about.

- Invest Smarter puts the surplus to work. TSP allocation, Roth decisions, and the compounding that turns monthly contributions into retirement accounts.

All three domains move together. Earning more without controlling spending just raises the floor alongside the ceiling. Controlling spending without enough income still leaves a gap. Investing without either one means there is nothing to invest. If you have already read the Spend Less series, you know how the cash flow side works. If you are starting here, that is fine. This article stands on its own.

What Consistent Contributions Actually Produce

Before we get to the ceiling, you need to see what is on the other side of it. This is the part most people skip, and it is the reason the gap matters.

An E-3 who starts contributing $500 a month to TSP at age 20, invested in a diversified portfolio averaging 7% annual returns, ends up with approximately $1.26 million by age 59 and a half. That is the retirement account withdrawal age. That is also, on $500 a month, a millionaire.

That same E-3 who waits until 25 to start the same $500 a month? Approximately $867,000 by the same age. Not a millionaire. Same monthly amount. Five fewer years. One is a millionaire. One is not. The only difference is when the contributions started.

The cost of waiting those five years is nearly $400,000. It is not money you lost. It is money that never existed because compound growth had less time to work. Nobody took it from you. It just never appeared.

That does not mean the 25-year-old is out of the game. Run the math the other direction: to hit that same $1.26 million by 59 and a half, the person who starts at 25 needs $727 a month instead of $500. Starting at 30, the number climbs to $1,075. The destination does not change. The contribution required to reach it does.

That is the relationship between time and money in one table. The later you start, the more each month has to carry. And at some point, the monthly contribution required to reach your target starts pressing against what your income can actually absorb. When that happens, you have two options: accept a smaller end state, or find a way to earn more so the contribution fits.

These are hypothetical illustrations, not predictions. Market returns vary. Some years are up 20%, some are down 30%. The 7% figure is a long-term historical average for diversified portfolios, not a guarantee of future performance. But the principle holds: consistent contributions, given enough time and a reasonable rate of return, produce account balances that change the trajectory of a family. The Invest Smarter series covers the mechanics in detail.

The question is not whether you can pay rent this month. It is about whether your income can sustain the contributions that turn into half a million or a million dollars twenty years from now.

The question is whether your pay can get you there.

The Ceiling

Most military families can pay their bills. Military pay covers the essentials, and probably a decent life. That is not the issue.

The issue is what happens after the bills. After groceries, after eating out, after road trips and birthday presents and the things that make this worth doing. Is there enough left to fully fund retirement across every available account?

Sit with that question for a second. Think about your own household. Think about what comes out before you have a chance to decide where it goes.

For a lot of families, the answer is no. Not because military pay is bad. Because one income source, even a reliable and well-structured one, has a mathematical limit on what it can produce. If you are not fully funding retirement, you are leaving money on the table every single month.

The Gap, by the Numbers

Here is what it actually looks like. These numbers use 2026 data: DFAS pay tables with the 3.8% raise, BAH rates for Camp Lejeune (a mid-tier base, with dependents), and current BAS rates. Base pay is taxable. BAH and BAS are not. The take-home column reflects federal income tax, FICA, and North Carolina state tax for married filing jointly. Your state may differ, but the structure is the same everywhere.

BAS covers the service member’s meals, not the family’s groceries. If you have dependents, the grocery bill is a different conversation entirely.

What Full Contribution Looks Like (2026)

| Scenario | TSP | Roth IRA | Spousal Roth IRA | Monthly | Annual |

|---|---|---|---|---|---|

| Single | $2,042 | $625 | n/a | $2,667 | $32,004 |

| Married | $2,042 | $625 | $625 | $3,292 | $39,504 |

Four Ranks, Same Target

| Rank / TIS | E-3 / 3 yrs | E-5 / 8 yrs | E-7 / 14 yrs | O-3 / 6 yrs |

|---|---|---|---|---|

| Base Pay (gross) | $3,198 | $4,300 | $5,835 | $7,737 |

| Taxes (fed + FICA + NC) | -$363 | -$607 | -$975 | -$1,434 |

| BAH (tax-free) | $1,578 | $1,584 | $1,995 | $2,085 |

| BAS (tax-free) | $477 | $477 | $477 | $328 |

| Total Take-Home | $4,890 | $5,754 | $7,332 | $8,716 |

Now subtract the full contribution target and look at what is left to live on:

| Rank / TIS | E-3 / 3 yrs | E-5 / 8 yrs | E-7 / 14 yrs | O-3 / 6 yrs |

|---|---|---|---|---|

| Left after single target ($2,667/mo) | $2,223 | $3,087 | $4,665 | $6,049 |

| Left after married target ($3,292/mo) | $1,598 | $2,462 | $4,040 | $5,424 |

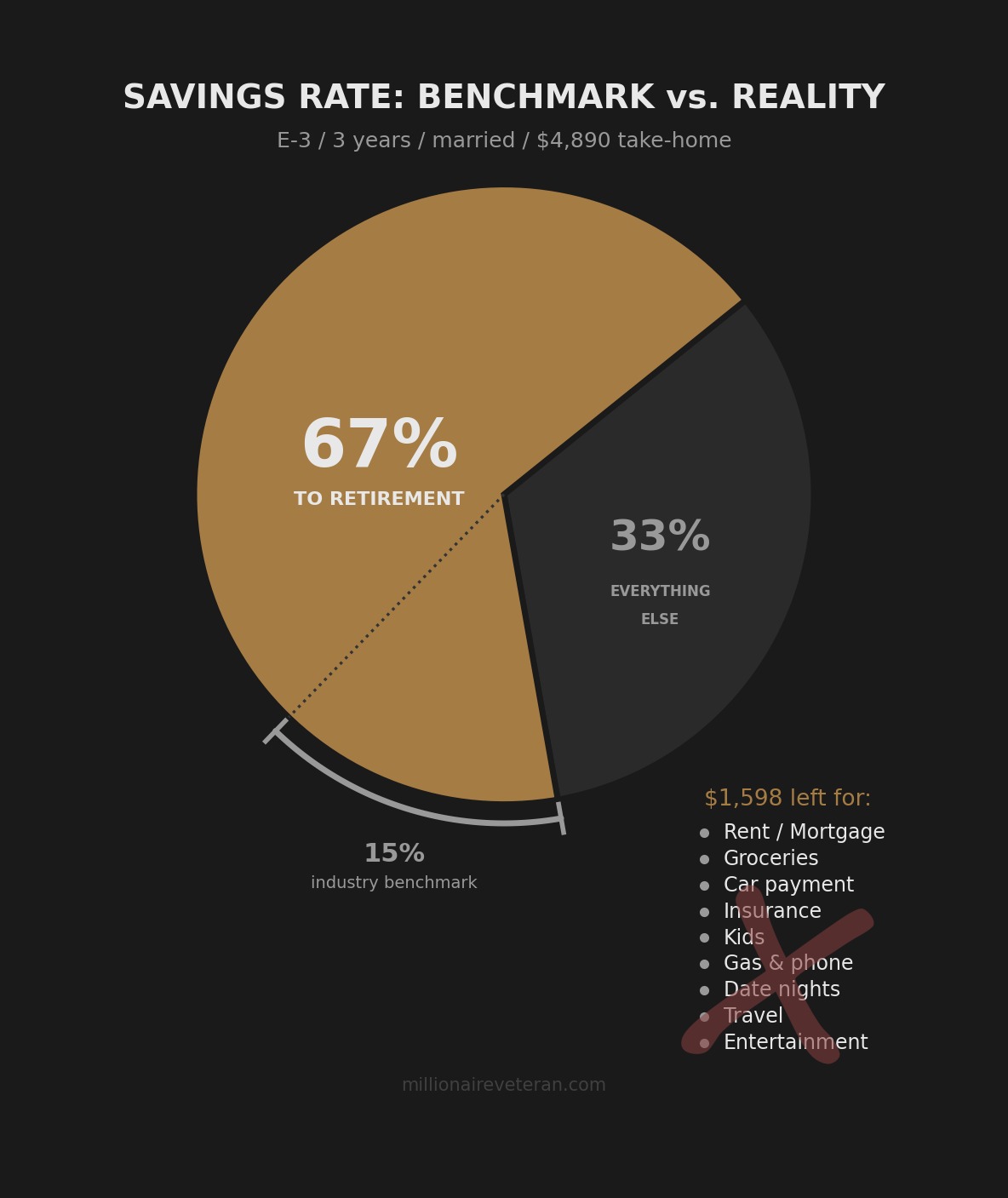

Look at the married row for an E-3. That is what is left for groceries, car payment, gas, phone, insurance, kids, and every other dollar of life after fully funding retirement. You already know whether that works for your family. For most, it does not.

The E-5 has more room but not much. Two car payments, childcare, or any of the normal expenses that come with a family at eight years in, and the margin disappears.

Senior NCOs and officers have real capacity. But capacity and results are not the same thing. The question is whether that money actually gets diverted into retirement accounts or whether it gets absorbed into a slightly nicer truck, a slightly bigger apartment, and a few hundred more a month in dining out. The room exists. The system to capture it does not.

What Those Numbers Mean as a Savings Rate

Turn those dollar amounts into percentages of take-home pay.

For the E-3 married family, maxing every tax-advantaged account takes 67% of take-home. The E-5: 57%. The E-7: 45%. The O-3: 38%.

| Metric | E-3 / 3 yrs | E-5 / 8 yrs | E-7 / 14 yrs | O-3 / 6 yrs |

|---|---|---|---|---|

| Full contribution as % of take-home | 67% | 57% | 45% | 38% |

Fidelity, Vanguard, and T. Rowe Price all converge on the same benchmark: save 15% of income toward retirement, including any employer match. For BRS members, the government contributes 1% automatically and matches up to 4%, so the personal contribution to hit 15% is closer to 10%. That is the number people carry around. Fifteen percent feels responsible. It feels like something you can do and still have a life.

There is a problem with that benchmark. It is a percentage, and the retirement accounts you are trying to fill are not percentages. They are fixed dollar amounts. The TSP limit is $24,500 a year. Each Roth IRA is $7,500. A married couple maxing all three accounts needs $39,504 a year, or $3,292 a month. Those numbers do not adjust based on your income. They do not care whether 15% of your pay gets you there or not.

For an O-3, 15% of take-home is about $1,307 a month. That covers roughly 40% of the full contribution target. For an E-5, 15% is about $863 a month. That is roughly a quarter of the way there. The benchmark gets you moving, and moving is better than standing still. But it does not get you to full funding.

Most families do not start at full funding. You progress toward it over time. Capture the employer match first, then fill IRAs, then push TSP contributions higher as income and discipline allow. There is a sequence, and the sequence exists because trying to do everything at once on a junior paycheck is not a plan. It is a way to burn out your household in two months. The full roadmap with milestones sequenced for service members and their families is inside the free community.

The realistic range for families pushing past the benchmark is somewhere between 25 and 35 percent of take-home. That is doable. You feel it, but you can still fund date nights, entertainment, and the road trip you have been planning for months. The system works when retirement and lifestyle are both funded intentionally. Without that system, lifestyle wins every time and the retirement contribution gets quietly dropped because it is the one expense that does not send you a bill this month.

When the percentage required to reach full funding climbs past what the household can absorb without cutting into the things that keep your family connected and sane, that is the ceiling. That is the signal. The ceiling has to move. The income has to grow so that $3,292 a month sits closer to 15% of what comes in, not 57% or 67%. At that point, full funding feels like what Fidelity described: responsible, sustainable, and part of a life you actually want to live.

I ran these numbers on my own finances when I built the framework. The gap was there. It was smaller than I expected, but it was real, and I was a senior NCO at the time. Seeing that gap clearly was the turning point for my family, because for the first time I had a real, tangible target I could go after and get.

Why Cutting Alone Will Not Close It

The Spend Less domain exists for a reason. Getting visibility into cash flow and routing every dollar with intention creates real margin. It works. For many families, the Spend Less work alone recovers hundreds of dollars a month that were leaking to subscriptions nobody used, insurance nobody shopped, and spending nobody tracked.

But subtraction has a floor. You can cut subscriptions, renegotiate insurance, eat at home more often, pack lunches. At some point you are cutting into the date nights, the road trips to see family, the birthday party for your kid. For junior enlisted, look at that savings rate column. No combination of coupons, meal prep, and canceled subscriptions closes a 50-point spread between 15% and 67% without stripping the life down to something nobody wants to sustain.

You cannot budget your way past a mathematical limit on one income source. The ceiling is structural, and that is what the rest of this series is about.

The Lifestyle Creep Trap

This is where the connection between Spend Less and Earn More gets real.

A family earning $5,000 a month starts a side income stream. Brings in $1,500. Household income jumps to $6,500. That should be progress. The full contribution target that used to eat 66% of income now sits at 51%. Still high, but getting closer to sustainable.

Two months later, the extra $1,500 is gone. A nicer apartment off base because the BAH differential looked like free money. Eating out twice a week instead of once. A couple new subscriptions. An upgrade on the phone plan. New tires for the truck because they were overdue and now there is breathing room. A weekend trip because the family earned it. Nothing dramatic. Nothing irresponsible. Each one felt reasonable in isolation. Together they consumed the entire side income without anyone noticing it happen. The savings rate never moved. The gap quietly refilled itself from the other direction.

Without a system, new income gets absorbed the same way existing income does. The ceiling moves up, but so does the floor. The gap stays the same size.

The Compass Method, the cash flow system taught inside the free community, was built for exactly this. It is not a deprivation plan. It routes every dollar, including the ones you spend on dinner with your family and a weekend trip to the coast. The spending is part of the system, not the enemy of it. Dinner, birthdays, the road trip you have been talking about for three months. All of it gets routed. Nothing leaks. Nothing gets left behind. But it does not happen automatically. It takes intentional setup and some real work to get the system running. That is what the community walks you through.

What Comes Next

One income source can do a lot. It probably cannot do everything. You have seen the numbers now.

Before you take a single step toward earning more, you need to know what not to step in. The internet is full of advice for people who want to make extra money, and most of it is expensive, recycled, or designed to sell you someone else’s dream instead of building your own.

The next article in this series is about that landscape. Five patterns that separate legitimate income education from the stuff that wastes your time and money. Learn to see the patterns first. Then you can move with confidence instead of desperation. Read it before you Google “how to make extra money.”

Build Alongside People Who Get It

The Millionaire Veteran community is free. Inside, members share what is working, what is not, and what they are building. The Earn More tactics are community-driven: verified by people who are actually doing the work, not recycled from someone selling a course. The community is still growing, and the resource library grows with it. That is the point. It stays fresh because real people maintain it.

The community also has the full Compass Method implementation, the cash flow system that routes every dollar you earn, whether from military pay or from something you build on the side, to the right purpose. Because earning more without that system just raises the floor alongside the ceiling.

About the Author

Joshua Breaux

Retired U.S. Marine

Financial Management Analyst

BS & MBA in Analytics

His family runs on the same systems he teaches here.

This content is educational and does not constitute personalized financial advice. Millionaire Veteran is not affiliated with the Thrift Savings Plan, FRTIB, or the U.S. Government. Past performance does not guarantee future results.