Search for the best TSP investment strategy and most of what you’ll find is a version of the four patterns dressed up with confidence.

“Go 100% C Fund and hold.” That’s Pattern 2 with someone else’s conviction attached. “Use the lifecycle fund for your age.” Pattern 3 with an official name. “Watch the moving averages and shift when the market turns.” Pattern 4 with a Telegram group.

The reader who identified their pattern and then sized the real dollar cost of the risks they carry already has the framework to see through this. When you encounter TSP advice anywhere, the first question is which pattern it maps to. If you can map it, you’ve probably found a pattern wearing a strategy’s uniform.

BRS made every service member under it an investor whether they know it or not. The pension gap is real money. The risks are real dollars. And most of the advice available for managing a TSP account doesn’t actually address either one.

So what would?

The Problem with Discretion

Every approach listed above has one thing in common. At some point, someone has to make a judgment call about the market.

That someone is you, or it’s someone you follow. A friend at the smoke pit. A YouTuber who seems confident. A financial advisor who charges a percentage. A Reddit thread with a thousand upvotes.

Judgment works in calm markets. When everything is green, every approach looks smart. The problem is that calm markets are not where your TSP is at risk. Your TSP is at risk when markets are down 40% and the judgment that felt bulletproof in January feels like guessing by March.

The person who said “hold through the dip” on a podcast in October is the same person who says “this time is different” in March. Every time. That is not a character flaw. It is the documented behavior of human beings under financial stress. Discretionary decisions under pressure consistently underperform systematic approaches over complete market cycles. The research on this is not ambiguous.

The question is not “who has the best judgment about the market?” It is “can we remove judgment from the equation entirely?”

What “Rules-Based” Actually Means

A rules-based framework is a set of predefined criteria, built when thinking is clear, that executes the same way regardless of how the market feels, how the news sounds, or what your gut says.

Not prediction. Not reaction. Execution of a plan that was decided before the pressure hit.

The rules are set against defined thresholds. When conditions deteriorate past a specific line, the framework acts. When conditions recover past a specific line, the framework acts again. No one’s opinion is required. No one’s nerve is tested. The criteria do not care whether you’re scared, whether the headlines are loud, or whether your buddy just told you he moved everything to capital preservation last week.

One structural principle matters more than any other: the market falls faster than it rises. A sustained decline can cut a portfolio by half in under 18 months. The recovery from that same decline historically takes years. Any framework built for this reality must reflect the asymmetry. Fast defensive action when conditions deteriorate. Slow, deliberate re-entry when conditions recover.

That re-entry discipline is where most approaches fail. Getting out is the easy part. Getting back in is where the damage happens. If the framework re-enters too quickly during a bear market rally, and the decline resumes, you absorb the second leg of the drawdown. Then you exit again. Then you wait. Then you try again. Each round-trip costs real money and real conviction. This is called whipsaw, and it is the primary failure mode of most timing approaches. It is also why most people who try to manage their own exits and entries end up worse off than if they had simply held.

A framework engineered to manage this asymmetry solves the problem that discretion cannot. It limits exposure during sustained declines. It avoids whipsaw by requiring structural confirmation before re-entry, not price recovery. And it runs the same way whether the operator is sitting at a desk or deployed to a FOB with intermittent connectivity and one check per week.

Five Ways a “System” Can Lie

Not every approach calling itself the best TSP investment strategy is real. Before evaluating any specific approach, you need a framework for spotting the ones that only work on paper.

Curve fitting. Tweaking rules until they perfectly match historical data. The more specific the parameters, the better the historical results look, and the more fragile the system becomes in live markets. If a system has 15 variables and a perfect track record, it wasn’t engineered. It was reverse-engineered. Those are different things.

Recency bias. Rules built on five years of a bull market. If the approach hasn’t been applied through a real crash, a real bear market, and a complete recovery, it hasn’t been tested. A system that works from 2019 to 2024 tells you almost nothing about what it does in 2008 conditions. The test is full market cycles, not recent performance.

Over-parameterization. Adding filters, indicators, and conditions until the historical results look perfect. Every parameter is a point of failure when the market does something new. Simplicity is not a limitation. It is a design choice. The fewer moving parts, the fewer things that can break.

Lookahead bias. “If you had moved on March 23, 2020…” Nobody knew March 23 was the bottom. Nobody. That date only became the bottom after the fact. Any approach that requires identifying tops or bottoms in real time is not a system. It is hindsight wearing a spreadsheet.

Execution impossibility. A system that requires daily monitoring, real-time data feeds, or constant adjustment. You are a service member. You deploy. You go to the field. You have 48-hour duty. You stand watch. If a system cannot be executed with one check per week and five minutes of your time, it does not work for your life, regardless of what the numbers on the screen say.

Five Questions to Evaluate Any TSP Investment Strategy

Once you’ve filtered out the false systems, five questions separate the real from the marginal.

How many parameters does it use?

Fewer is better. Every parameter is an assumption about market behavior. Assumptions break when conditions change. A framework you can count on one hand is one that was built for robustness, not optimization. If you need a spreadsheet to list the variables, the system was designed to impress, not to function across conditions it hasn’t seen yet.

Over how many full market cycles were the rules applied?

Not years. Cycles. A full cycle includes a sustained advance, a meaningful decline, and a complete recovery. An approach applied from 2004 through today has been run through the 2008 financial crisis, the 2020 COVID crash, the 2022 bear market, multiple corrections, and every recovery between. Same rules applied to every condition. That is the bar.

Were the rules changed at any point during the historical period?

This is the question that kills most claims. If the rules were adjusted mid-period to improve the results, what you’re looking at is not a test. It is an optimization. Same rules, start to finish, across every condition. No after-the-fact adjustments. No mid-crisis exceptions. No “we updated the model in 2015.” One rule set. Every market.

Could you execute it from deployment with one check per week?

Actual allocation moves should be rare by design. Most weeks should require zero action from you. When action is required, the alert should be specific: exactly what to do, and when. Not a chart you need to interpret. Not a dashboard you need to monitor. One check. Five minutes. If you’re on a FOB with intermittent WiFi and 20 minutes between duties, the system either works for that or it doesn’t.

Does it account for TSP-specific constraints?

The Thrift Savings Plan is not a brokerage account. It has interfund transfer processing delays. It has limited fund options. It has specific contribution rules that affect how and when money moves. A framework adapted from stock trading or forex or commodity futures will collide with these constraints. A framework engineered for TSP from the ground up does not.

Why Understanding Matters More Than the Mechanism

This is the point that every sales page for every signal service gets wrong. They sell the mechanism. The signal. The alert. The algorithm. As if the mechanism alone is enough.

It is not.

A framework you don’t understand is just another thing you’ll abandon when it feels wrong.

The signal says hold your current position during a dip. Your account is down $80,000. The headlines are saying “worst market since 2008.” Your coworkers are moving to capital preservation. Do you trust the signal?

Only if you understand why it was built the way it was. Only if you know what the framework has done in conditions like these before. Only if you have seen the data, understood the tradeoffs, and made the conscious decision that this approach matches your timeline and your risk appetite.

Borrowed conviction doesn’t survive drawdowns. That was true when we looked at the four patterns. It is equally true here. Subscribing to a signal without understanding the framework behind it is the same behavioral gap as being 100% in equities because a Reddit thread told you to. The label changed. The vulnerability didn’t.

Education is not a bonus feature on top of the framework. Education is the structural requirement that makes the framework functional. Without it, the first real drawdown turns every subscriber into a Reactive Mover, doing exactly the thing the framework was designed to prevent.

I run this in my own TSP account. Same rules, same signals, same framework. That matters because it means my retirement is subject to the same decisions yours would be. But even that is not the reason to trust it. The reason is the data, the market cycles it has been applied through, and the five questions you now have the tools to ask about any approach, mine included.

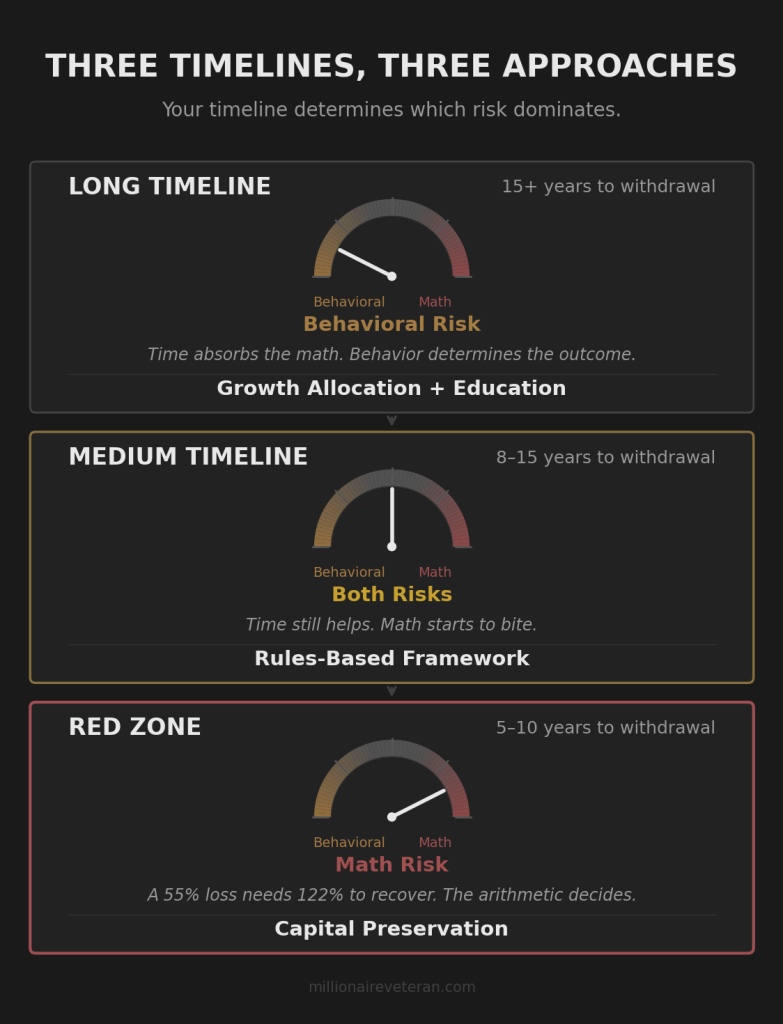

Three Timelines, Three Approaches

Not every service member needs the same thing. The right approach depends on three variables: your timeline, your risk appetite, and your behavioral honesty about how you’d respond to a real drawdown.

Long timeline: 15 or more years to withdrawal.

You have the most valuable asset in investing: time. A growth allocation, held with conviction through full market cycles, has produced positive returns over every 20-year rolling period since 1928. For you, the primary risk is behavioral. Not the crash itself, but your response to it. The crash at year 5 of a 25-year career is a footnote. The question is whether you hold through it or sell at the bottom because your conviction was borrowed.

For the long-timeline investor, education is the strategy. Understanding the drawdown math, understanding why you’re in a growth position, understanding what a 55% decline looks like on your specific balance and why your timeline absorbs it. That understanding is what builds the conviction to hold. You don’t need someone to tell you when to move. You need to understand why you don’t.

I’ve seen first-term service members get this right from the start. Clear-eyed about the drawdown data. Unshakeable because they did the math themselves, not because someone told them it would be fine.

Medium timeline: 8 to 15 years to withdrawal.

You have time, but less of it. A growth allocation still makes mathematical sense for most of this window. But a sustained drawdown at year 13 of a 15-year career is not a footnote. It is $330,000 gone from a $600,000 account, and the recovery timeline is longer than the career you have left.

For the medium-timeline investor, the question shifts from “can I hold through it?” to “should I have to?” Your time horizon could survive a deep drawdown if you held. The behavioral risk is that you won’t. A framework with a systematic mechanism for stepping aside when conditions deteriorate, one that removes the decision from the moment of maximum stress, addresses both the math risk and the behavioral risk simultaneously.

The framework gives the Default G-Funder a reason to move. It gives the Reactive Mover a reason to stay.

Short timeline: the Red Zone, 5 to 10 years before actual withdrawal age.

Math risk is the primary threat. A crash in this window takes the largest possible dollar amount from your account at the point when your remaining recovery time is the shortest it has ever been. Regardless of your behavior, regardless of your conviction, a 55% loss that requires a 122% gain to recover is arithmetic that does not care about discipline.

For the Red Zone investor, a conservative posture is not caution. It is math. The objective shifts from maximizing growth to protecting what you have built over a full career of disciplined saving.

The right approach depends on your timeline, your risk appetite, and your behavioral honesty. Most people think they can endure a drawdown until they see the real dollar amount disappear from their screen. Knowing yourself, not the calm-market version of yourself, is part of the selection.

Your framework handles allocation risk. Your account structure handles tax risk, contribution timing, and whether your balance is positioned correctly for withdrawal. Both halves matter. The allocation question is what this article addresses. The structural question is a separate analysis with its own set of decisions.

A System That Decides Before the Pressure Hits

The search for “the best TSP investment strategy” assumes there’s one answer. There isn’t. There’s an approach matched to your timeline, your risk, and your behavioral reality. And the way to evaluate whether that approach is real is the same five questions, regardless of where you find it.

Does it use a small number of parameters? Has it been applied through full market cycles, same rules the whole way? Could you execute it from deployment? Was it built for TSP?

If the answer to all five is yes, you’re looking at something worth examining closely.

If the answer to any of them is no, you’ve learned what the framework is missing before it cost you anything.

The framework works from wherever you are. An E-3 in their first enlistment building the conviction to hold through 20 years of market noise. An O-4 at year 12 who needs a mechanism that removes the emotional decision from the equation. An E-8 in the Red Zone protecting the balance they’ve built over an entire career. Each starting from a different place. Each with a framework that matches.

I’ve seen late starters close the gap. The framework doesn’t punish you for starting late. The math rewards you for starting now.

Get the Full blueprint

The Firewatch Blueprint walks through the pension gap math, all four default patterns, and the full three-strategy framework. Everything in this article, plus the complete picture.

About the Author

Joshua Breaux

Retired U.S. Marine

Financial Management Analyst

BS & MBA in Analytics

His family runs on the same systems he teaches here.

This content is educational and does not constitute personalized financial advice. Millionaire Veteran is not affiliated with the Thrift Savings Plan, FRTIB, or the U.S. Government. Past performance does not guarantee future results.