The first time I sat down to actually run Dave Ramsey’s zero-based budget, I built a clean monthly plan, assigned every dollar a job, and felt good about it. Then real life started.

By day six I had a stack of transactions I had not categorized. By day twelve the plan and my actual spending were two different documents. By the end of the month I rebuilt from scratch and told myself I would do better next time. I did not.

The method was not the problem. I was, and I was not. Ramsey nailed the principle. Every dollar should have a job. What he built around that principle is a backward-looking system that asks you to spend money, then categorize the transaction, then reconcile to the plan at month-end, then rebuild the plan for the next month. For one type of reader, that loop works beautifully. For most people who search “dave ramsey zero based budget” looking for a method that will finally hold, it does not.

This article is for two readers: the one who has never tried zero-based budgeting and is evaluating it, and the one who tried it and watched it quietly break. Both deserve an honest picture of who the method serves and what to do if you are not that person.

What Dave Ramsey Got Right About Zero-Based Budgeting

Ramsey’s principle is simple and correct: every dollar has a job. Income, minus expenses, minus savings, minus debt payoff, equals zero. No money sits unassigned. Nothing drifts into discretionary spending because no one bothered to direct it.

That principle is the foundation of every working cash flow system on the planet. The dave ramsey zero based budget version operationalizes it through a monthly plan. You build the plan before the month starts. You list income at the top. You list every category of spending below it. You assign dollars until you hit zero. Then you track. Every grocery run, every gas fill-up, every coffee, every Amazon order. You categorize each transaction against the plan. At month-end you reconcile, see where you drifted, and rebuild the plan for next month with what you learned.

The discipline this builds is real. People who run zero-based budgeting consistently develop a fluent relationship with their money. They know what they spent on dining last month. They know which categories blew out. They know which obligations are fixed and which are variable. That awareness is the byproduct of doing the work, and it is genuinely valuable.

Ramsey’s other contribution, which gets less credit, is naming the failure mode of the alternative. Most households who do not have a system at all run on what he would call cash chaos: one checking account, no plan, the balance is whatever it is, and at the end of the month nobody can explain where the money went. Zero-based budgeting replaces that with structure. Every dollar accounted for, on purpose, before it moves.

For the right reader, that structure is enough.

Who Zero-Based Budgeting Actually Works For

Zero-based budgeting works for the meticulous reader. The one who genuinely enjoys sitting down each evening with a notebook or an app and reconciling the day’s transactions. The household where one person opens the budget every night and works through it without resenting the work.

That reader exists, and Ramsey deserves credit for surfacing the personality type. Most personal finance content pretends every reader is the same. Ramsey’s method self-selects. If you finish the first month of the dave ramsey zero based budget still showing up to reconcile, you are the type the method serves. If you do not, you are not, and the failure is not your discipline. It is a mismatch between you and the mechanism.

There is no shame in not being that personality type. The meticulous daily reconciler is a small fraction of the population. The rest of us run on a different cognitive budget. We will sit down and do five minutes of routing on payday. We will not sit down and do five minutes of categorization every night for thirty nights in a row. The intent is there. The follow-through is not. Not because of weakness. Because the mechanism is asking for the wrong kind of attention at the wrong cadence.

If you have tried zero-based budgeting and watched it slip, the diagnosis is usually that simple. The method was not built for the cognitive budget you actually have.

Where Zero-Based Budgeting Hits the Wall: It Looks Backward

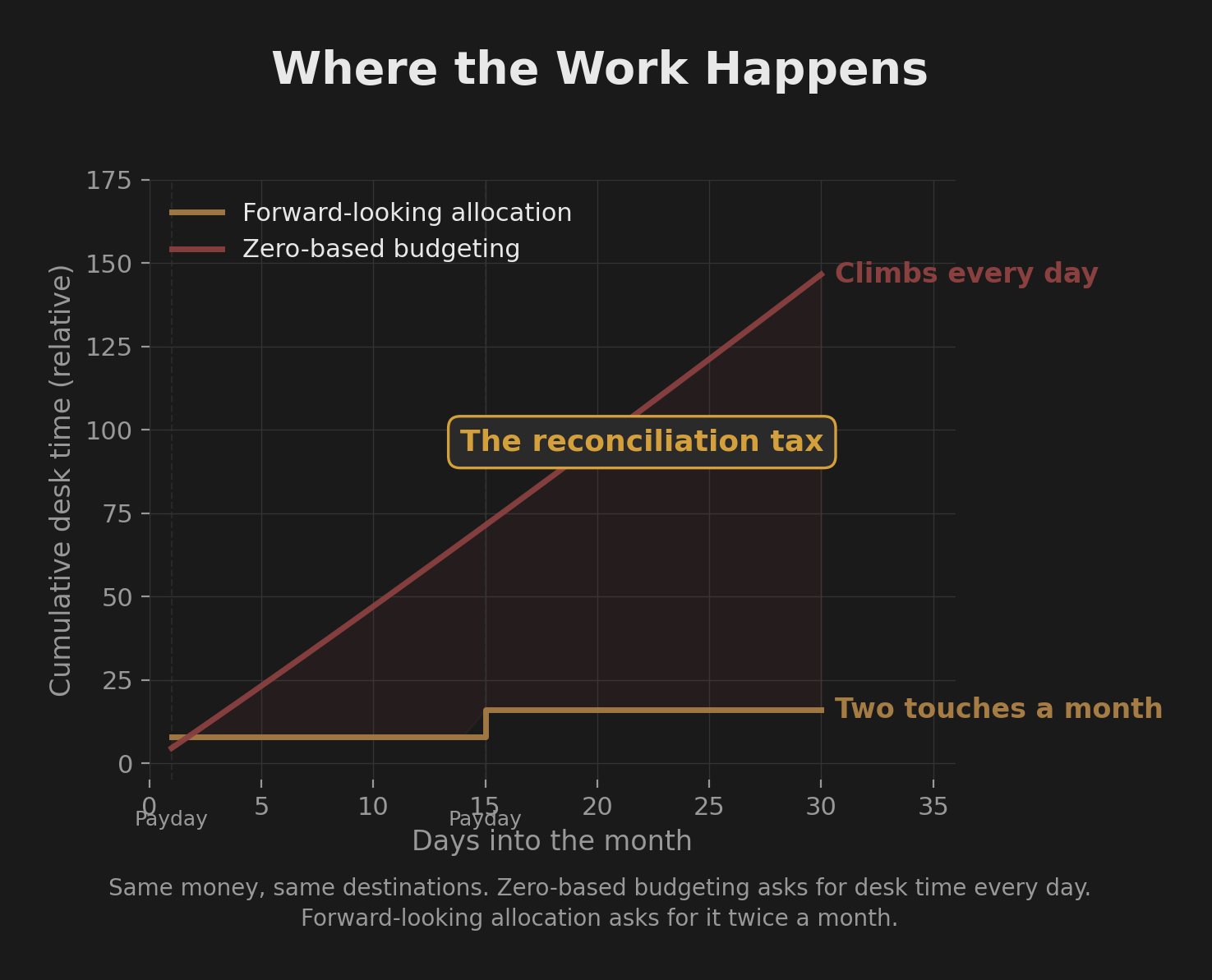

Zero-based budgeting is backward-looking. The work happens after the money moves. You spend first. You categorize the transaction after. You reconcile to plan at month-end. You rebuild the plan for next month based on what already happened.

The plan is a statement of intent. The categorized transactions are a record of behavior. The gap between them is what the method exists to close. Closing that gap requires daily attention because the gap grows every day. Skip a day and you have a backlog. Skip a week and the backlog is large enough that catching up feels like a chore. Skip two weeks and you stop opening the app.

This is not a discipline failure. It is the natural consequence of a method that requires you to do the work after the money is already gone. The reconciliation tax compounds. The longer you wait, the bigger the catch-up.

Zero-based budgeting looks backward; the Compass Method looks forward.

The bigger structural difference sits underneath that. Under zero-based budgeting, the money never actually moves. It stays in one checking account. The “categories” live on a spreadsheet or inside an app. The dollars assigned to groceries and the dollars assigned to the car payment are sitting in the same pile, and the only thing keeping them separate is the line item on the screen and your willpower at the point of purchase. The Compass Method, which I will get to in a minute, moves the work to the front of the cycle and moves the money to actual separate bank accounts. Real transfers. Real account balances. The decision happens at payday, on the 1st and the 15th, in a few minutes of routing, and then the separation is enforced by the bank instead of by you. No categorization. No reconciliation. No month-end rebuild.

The Military Reality: You Are Not at a Desk Every Day

Service members are not always at a desk daily. Training exercises run twelve to sixteen hour days for weeks at a stretch. TDY rotations strip you out of your routine for two to six weeks at a time, sometimes with limited or no connectivity. Field problems put you in the woods with no phone signal. Watch standing breaks your schedule into shift cycles that do not accommodate evening desk work. Deployment makes daily reconciliation impossible for months on end.

Whoever is managing the household during these stretches absorbs the operational load alone, whether that is a spouse, a roommate, a parent helping out, or no one at all. Every household decision that would normally be shared collapses onto one person, or onto nobody, while the rest of life keeps moving. Asking that same person to also reconcile transactions every evening is asking too much, and the budget app dies first.

None of this is about military pay being unpredictable. Base pay is structurally stable. Base pay, BAH, and BAS cycle through the 1st and the 15th on a fixed schedule. The semi-monthly cadence is one of the most reliable income streams in the American economy. The problem is not the money coming in. The problem is the time and attention going out.

Zero-based budgeting was designed for a household that can be at a desk every night. Military life frequently makes that impossible. So does shift work, traveling work, parenting through a hard season, caregiving, and a hundred other circumstances where evening desk time is not realistic. The failure mode is universal. Military families happen to be a group that hits it hard, often, and early.

If you have tried zero-based budgeting on top of a training schedule, a TDY rotation, or a deployment cycle and watched it fall apart, the method was not built for the life you are living. It is a design constraint, not a character question.

The Forward-Looking Alternative

The fix is not to try harder. The fix is to move the assignment decision earlier and to make the assignment physical.

Forward-looking allocation works like this. Income arrives in one Income account. On payday, you transfer pre-calculated amounts to a small number of purpose-specific accounts at your bank. Each transfer is a percentage of the deposit, set in advance. The work is a few minutes, twice a month, on the 1st and the 15th, and then you stop touching it until the next payday.

Once the routing is done, the account balances tell the truth. The Lifestyle account at $73? That is what you have left for discretionary spending until the next payday. No app to check. No mental math. No categorization. The balance is the answer.

This is bank-account-level separation. Not categories on paper. Not envelopes labeled with marker. Not buckets inside a single checking account. Actual separate accounts at the bank, each holding only the money that belongs to that purpose. The structural decision lives at the account level instead of on a spreadsheet, which means the decision is made once, in advance, and then enforced by the structure itself rather than re-litigated at every transaction.

This is the Compass Method. The principle Ramsey defended, that every dollar should have a job, is preserved. What changed is the mechanism. The job assignment happens at payday, in advance, at the bank, instead of at month-end, in arrears, on a spreadsheet.

Architecture, not discipline. That is the deeper move. Most people who quit zero-based budgeting blame themselves. The honest diagnosis is that they were running a backward-looking method against a forward-looking life. Once the mechanism inverts, the discipline problem disappears, because the discipline requirement disappears. You are no longer asked to do work the system should be doing for you. The structure does it.

Worth naming what this is not. It is not automated allocation. The transfers happen by hand on payday, because the act of moving the money is the habit that makes the system work. It is not a single-account budget with category labels. The accounts are real and separate, each with its own balance, each tied to a specific purpose. It is not “set and forget.” A monthly review keeps the routing calibrated as life changes. What it removes is the daily reconciliation tax. What it preserves is the every-dollar-a-job principle Ramsey spent his career defending.

For the full version of this thesis, with how it applies across every budgeting method, not just zero-based budgeting, see How to Stop Living Paycheck to Paycheck on Military Pay. It lays out the architecture-not-discipline frame across the entire category. For the mechanics of what a cash flow system actually does, see what a cash flow system actually does.

Your Next Step

If you have never tried a budget and you are evaluating zero-based budgeting because Ramsey is the trusted name in personal finance, ask yourself one question first. Are you the meticulous daily reconciler? If yes, the dave ramsey zero based budget will serve you well. If no, do not pick it just because it is the famous option. Start with the forward-looking version instead.

If you have already tried zero-based budgeting and watched it fall off, the mechanism was the issue, not your discipline. The forward-looking alternative is what you were looking for the whole time. The earlier section of this article linked to the full architecture-not-discipline thesis and the mechanics walk-through. Read whichever fits where you are.

Fix the cash flow first. Everything else gets easier.

Build the Forward-Looking Version With Your Real Numbers

The Diagnostic Review inside the Millionaire Veteran community walks you through your actual income and obligations and calibrates the routing percentages with your real numbers. Not a template. Not a worksheet you will fill out and abandon. An AI advisor that builds the structure with you, in conversation, using your inputs. The community is free.

About the Author

Joshua Breaux

Retired U.S. Marine

Financial Management Analyst

BS & MBA in Analytics

His family runs on the same systems he teaches here.

This content is educational and does not constitute personalized financial advice. Millionaire Veteran is not affiliated with the Thrift Savings Plan, FRTIB, or the U.S. Government. Past performance does not guarantee future results.