Most people researching Coast FIRE vs Barista FIRE are trying to answer one question: can I stop grinding at a full-time career before I am fully financially independent, and if so, how. The two strategies answer that question differently. Coast FIRE means you have invested enough that you can stop contributing and let compounding finish the job while you keep covering your living expenses. Barista FIRE means you downshift to part-time work that covers most of your living expenses, and for a lot of civilians, keeps their health insurance, while the invested balance is left alone to grow.

That distinction is the whole comparison. And almost every article that walks you through it is written for a civilian situation. The single biggest reason civilians choose Barista FIRE is one the military retirement path already handles before you ever sit down to do the math.

I am writing this as a retired Marine who has run these numbers for my own household and walked through them with other military families inside the Millionaire Veteran community. The framework below is general. The dollar figures are illustrative. Check your own pension projection from DFAS, your own VA disability if it applies, and your actual TSP and IRA balances before you treat any of this as a plan rather than a way to think.

Coast FIRE in One Paragraph, Then the Real Comparison

Coast FIRE is the point where your invested balance is large enough that, with no further contributions, compounding alone grows it to your full retirement number by the time you actually retire. You still cover your current living expenses from some income source. You just stop feeding the retirement account. The full definition, the reverse-compounding math, and a worked military example all live in what Coast FIRE actually is, so I am not going to re-derive it here.

The reason Coast FIRE and Barista FIRE get confused is that both involve easing off aggressive saving. The difference is what covers your living expenses while the balance compounds. Coast FIRE assumes you keep earning enough to live on, usually from the same career, and simply stop adding to investments. Barista FIRE assumes you walk away from the full-time career earlier and replace it with lighter work that pays the bills. One is a milestone you reach. The other is a way of structuring your work life around a portfolio you no longer need to feed.

What Barista FIRE Actually Is

Barista FIRE describes a position where you have enough invested to step off the full-time career track, but not enough to stop working entirely. You take a part-time or lower-stress job that covers most of your living expenses. The portfolio stays untouched and keeps compounding toward the full FI number. You are not retired. You are not still climbing. You are coasting on the strength of what you already built, with a smaller job filling the gap.

The name comes from a specific archetype: a part-time job, often retail or service work, that offers health benefits to part-time employees. That detail is not incidental. For a civilian, Barista FIRE does two jobs at once.

The first job is income. The part-time work covers living expenses so you do not have to start drawing down the portfolio years before you planned to. Selling investments early carries a particular danger when it happens during a market decline. A portfolio that drops 30% and then has to fund withdrawals on top of the loss may never recover the same way one left alone would. That is sequence-of-returns risk, and a bad sequence early in retirement can sink a portfolio that would have survived the exact same returns in a different order. The part-time paycheck exists in large part to keep the household from selling into a downturn.

The second job is health insurance. For anyone below Medicare age who has left a full-time employer, coverage on the individual marketplace can cost more than a mortgage payment, and the cost is hard to predict years out. A part-time job that comes with benefits solves that. This is the quiet engine under a large share of civilian Barista FIRE plans, and it is the piece that most comparison articles underweight.

There is a behavioral layer worth naming too. Plenty of people technically hit a number that says they could stop, and they still cannot make themselves do it. The income floor and the structure of a part-time job give them permission to step back without feeling like they jumped off a cliff. Hitting the number and accepting that you hit it turn out to be two different things, and the lighter job is often the bridge between them.

The Civilian Comparison: Coast FIRE vs Barista FIRE

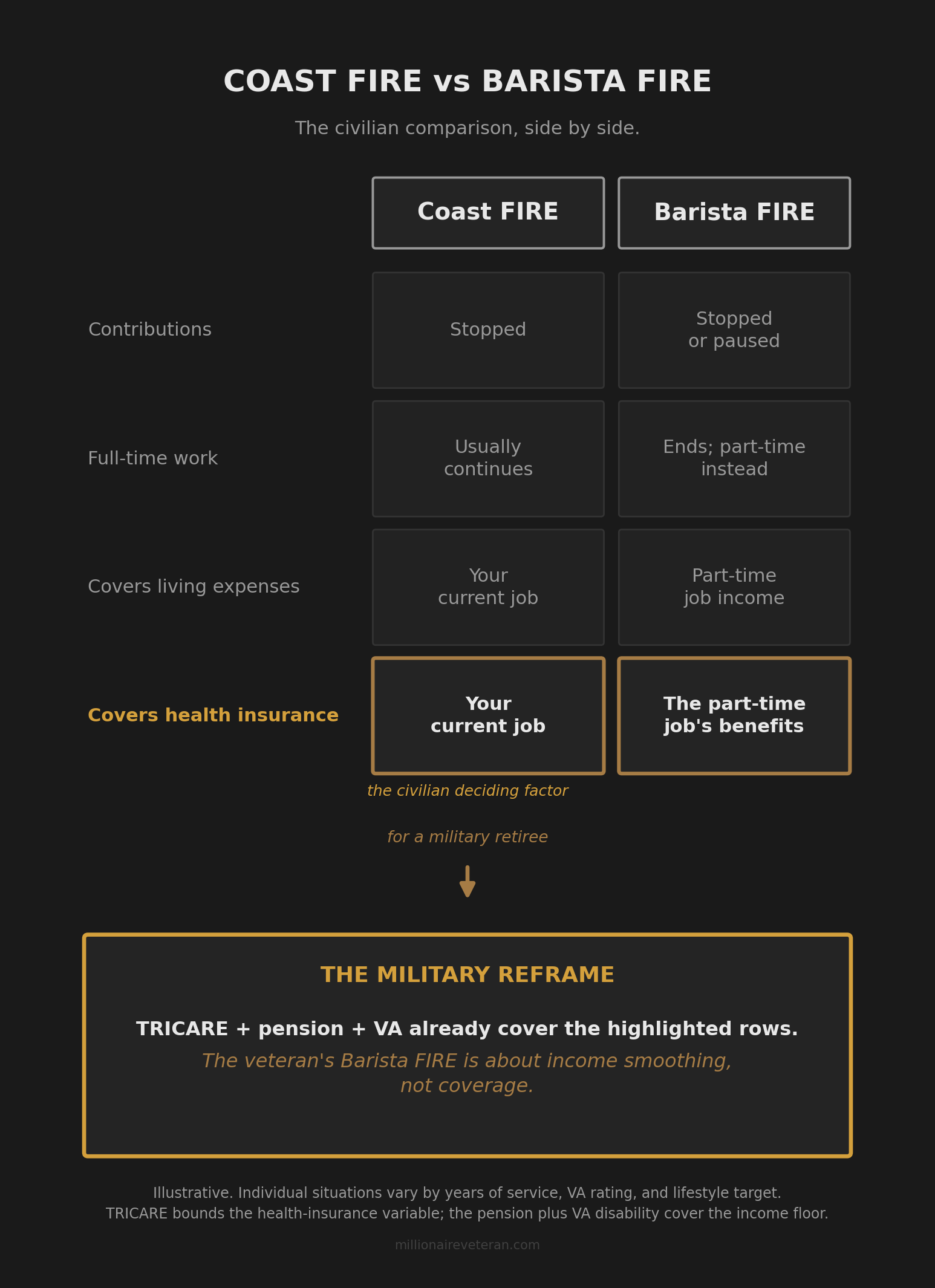

Set side by side, the two strategies sort out cleanly for a civilian. With Coast FIRE, contributions stop and the full-time job usually continues while compounding closes the rest of the distance. With Barista FIRE, the full-time career ends earlier and part-time work covers living expenses and benefits while the portfolio keeps growing. The full mechanics of each, including the worked math, live in what Coast FIRE actually is, so the point here is the choice between them, not the derivation.

For a civilian, that choice usually comes down to one factor more than any other. The math on the portfolio might say either strategy works. Either path can reach the same finish line on paper, because in both cases the balance is left alone to compound and the only real variable is what pays the bills in the meantime. The deciding factor is rarely the spreadsheet. It is the health-insurance gap before Medicare, and that gap is what pushes people toward the part-time job that comes with a benefits package even when the portfolio would have carried them either way. That is the hidden hinge under most civilian Coast-vs-Barista decisions, and it is exactly the hinge that military retirement removes.

The Military Reframe: TRICARE Changes the Barista Calculus

Look back at the two jobs Barista FIRE does for a civilian: cover living expenses without draining the portfolio, and bridge the health-insurance gap. Now look at what a service member walks away with after a twenty-year retirement.

There is a pension, paid for life and adjusted for inflation. Where it applies, there is VA disability, tax-free and paid for life on top of the pension. And there is TRICARE, which bounds the cost of healthcare in retirement to a small fraction of what the individual marketplace charges. The pension and VA disability cover the income floor in depth, which is the whole argument of the Coast FIRE article and not something I will re-run here. The piece that matters for this comparison is what that floor does to the reason a part-time job would exist at all.

Here is the difference in one line: civilian Barista FIRE buys health insurance; the military version buys income smoothing, because TRICARE already bought the coverage.

A civilian taking a barista job is often buying coverage first and income second. A military retiree already has coverage handled by TRICARE and a baseline income handled by the pension and VA floor. So the veteran who thinks about part-time work after retiring at twenty years is not solving for health insurance and is not solving for a basic income floor. Both of those are already in place. What is left is the gap between that floor and the lifestyle they actually want, and whether to fill it with part-time income.

That makes the part-time job optional rather than load-bearing. For a civilian, the barista job can be the thing holding the whole plan together. Lose it, and the coverage disappears and the portfolio drawdown starts early. For a military retiree, the same job is a margin choice: a way to top up income and add structure without touching the TSP and IRA balances ahead of schedule. The retiree can take that job, leave it, change it, or skip it entirely, and the floor underneath the household does not move. That freedom is the actual prize, and it is easy to miss when you are reading a comparison built for someone who has neither the pension nor the coverage already in hand. Same strategy on the surface. Completely different stakes underneath.

Which One Fits a Military Situation

The honest answer for most service members who retire at twenty years is that the pension, the VA floor where it applies, and TRICARE put them closer to a Coast FIRE position than to a Barista FIRE necessity. The two jobs that drive civilian Barista FIRE, income floor and coverage, are already partly solved by the structure of military retirement. What remains is the gap between the floor and the life you want.

There are three broad ways to handle that gap, and the right one depends entirely on your numbers. You can let an accumulated balance coast, leaning on compounding to close the distance to your full FI number over time. You can smooth income with part-time work, the veteran version of Barista FIRE, topping up the gap without drawing down investments early. Or you can run a combination, coasting on the balance while doing some part-time work for a few years to add margin and structure to the transition out of a full career. None of the three is the obviously correct answer, and the one that fits is the one your own numbers point to once you actually put them on paper instead of guessing at them.

This article names the categories. It does not pick one for you, and it does not hand you a target number, because that depends on your pension projection, your VA situation, your accumulated balances, your lifestyle target, and the return assumptions you want to use. Two people who both retired as an E-7 with twenty years can land in completely different positions depending on what they accumulated along the way and how much lifestyle they want to fund. Where any of these positions sits on the larger path is laid out in the FI Spectrum, the five stages from financial survival to full independence. Coast FIRE is Stage 4 on that spectrum. Barista FIRE, for a veteran, is one of the ways you can choose to live while you are standing in that stage.

Your Next Step

The Coast-vs-Barista question turns out to be a different question once coverage and a baseline income are already handled. For a civilian, it is largely a health-insurance decision wearing a retirement costume. For a military retiree, it is a cleaner choice about lifestyle, margin, and how hard you want to keep working when you no longer have to.

Until you know which stage you are standing at, Coast FIRE and Barista FIRE are two good ideas without an address. They only become a real decision once you can see your floor, your gap, and the stage you are actually in, which is exactly what the FI Spectrum lays out across all five stages from financial survival to full independence.

Your Coverage Is Handled. Now Find Your Gap.

Millionaire Veteran is a free community where military families put their real numbers on the Azimuth Roadmap: rank and years of service, take-home, contributions, and current TSP and IRA balances. The Diagnostic Review shows which FI Spectrum stage you are actually in and the next milestone to clear, and it is a placement, not a Coast FIRE calculator or a fund prescription. The Compass Method then routes the cash flow so the contributions actually leave the paycheck on payday, every payday.

About the Author

Joshua Breaux

Retired U.S. Marine

Financial Management Analyst

BS & MBA in Analytics

His family runs on the same systems he teaches here.

This content is educational and does not constitute personalized financial advice. Millionaire Veteran is not affiliated with the Thrift Savings Plan, FRTIB, or the U.S. Government. Past performance does not guarantee future results.