The Thrift Savings Plan (TSP) lets you take a hardship withdrawal while you are still in uniform or still on a federal payroll, and when a real expense is bearing down on you, that door can look like the fastest way out. This article walks through how a TSP hardship withdrawal actually works: what qualifies you, what it costs, and the alternatives worth checking before you sign the certification.

Most of what comes up when you search this falls into two piles. One is the government eligibility language, accurate and impossible to feel anything about. The other is marketing from firms that would like to move your money somewhere they can charge you to hold it. Neither pile puts a number on the thing that matters most, which is what the money you pull out would have become if you had left it alone.

So this covers both halves. The mechanics first, plainly, because you deserve a straight answer to a real question. Then the arithmetic almost everyone skips, because a decision you can run in your own head is a decision you can actually own.

None of this is a lecture about whether you should take one. The money is yours. Some hardships are real and immediate, and when they are, you want the whole picture in front of you, not a wagging finger. Let me get you that picture.

What a TSP Hardship Withdrawal Actually Is

A hardship withdrawal is one specific type of in-service withdrawal, which means you take it while you are still working for the federal government or still serving. Pin that down first, because two very different tools get called the same thing at the kitchen table.

A hardship withdrawal is not a loan. You do not pay it back. Once the money leaves your account, that balance is gone, and so is every dollar it would have earned for the rest of your career. A TSP loan is the other tool: you borrow against your own balance and repay it, with interest, to yourself. People confuse the two constantly, and the confusion is expensive, because it hides the single biggest difference between them. One leaves your retirement intact. The other does not.

This article stays on the hardship withdrawal. If you want the full map of every way money can leave a TSP, including age-based withdrawals, post-separation options, and required distributions, that lives in the complete guide to TSP withdrawal rules. Here we go deep on one door.

What Qualifies: TSP’s Five Financial-Hardship Categories

You cannot take a TSP hardship withdrawal for any reason you like. The Federal Retirement Thrift Investment Board (FRTIB) recognizes a specific set of financial hardships, and when you apply you certify, under penalty of perjury, that at least one of them applies to you.

There are five.

Recurring negative monthly cash flow. Your net income runs below your expenses, month after month, as an ongoing pattern. Not one tight month. A trend that keeps repeating.

Medical expenses. Unpaid medical costs for you or a dependent that insurance did not cover, of the kind you could deduct as a medical expense on your federal return.

Personal casualty loss. Damage, destruction, or loss of property from something sudden and unexpected: a fire, a flood, a storm, a theft.

Legal expenses for separation or divorce. Unpaid attorney fees and court costs tied specifically to separating from or divorcing your spouse.

Losses from a federally declared major disaster. Expenses and losses when the Federal Emergency Management Agency (FEMA) has declared a major disaster and your primary home or workplace sat inside the designated area.

Now notice what is missing. No home purchase. No college tuition. No funeral costs. Those sit on the IRS hardship list for private-sector 401(k) plans, and they get copied into TSP articles all the time by writers who never checked the difference. The TSP runs its own rules. Match your reason against the five above at TSP.gov before you count on any of it, because certifying a hardship that does not actually qualify is a problem you do not want.

The Mechanics: Minimum, Taxes, and the Penalty

Once you qualify, the process is simple, and the numbers start working against you right away.

You cannot withdraw less than $1,000, and you can only pull from your own contributions and what they have earned. When you apply, you certify that the hardship is genuine.

Then the money gets taxed. The traditional portion of the withdrawal counts as ordinary income for the year you take it. It stacks on top of your regular pay and gets taxed at your marginal rate. If part of your balance is Roth, the treatment shifts, and how your account splits between Roth and traditional is a structural question worth understanding on its own. Roth TSP vs Traditional TSP covers that side.

On top of income tax, if you are younger than 59½, the withdrawal usually carries a 10% early withdrawal penalty. A handful of exceptions exist, but an ordinary hardship at, say, 35 rarely lands on one of them.

One wrinkle catches people the following April. What the TSP withholds when it sends the money is not the same as what you finally owe. The plan withholds a share for federal taxes at payout, but your real bill depends on your total income for the year and the bracket it puts you in. If the withholding comes up short, the rest comes due when you file, sometimes as a surprise on top of a year that was already hard enough to prompt the withdrawal. Plan for the whole tax, not just the slice held back at the door.

One piece of good news: a hardship withdrawal no longer freezes your contributions. The old rule locked you out of contributing for six months afterward. The TSP Modernization Act ended that. You can keep funding your account the day after you withdraw. That does not make the withdrawal cheap. It only removes one of the older penalties layered on top of it.

The Real Cost Isn’t the Penalty

This is the point where most people stop doing math, right when the math starts to matter.

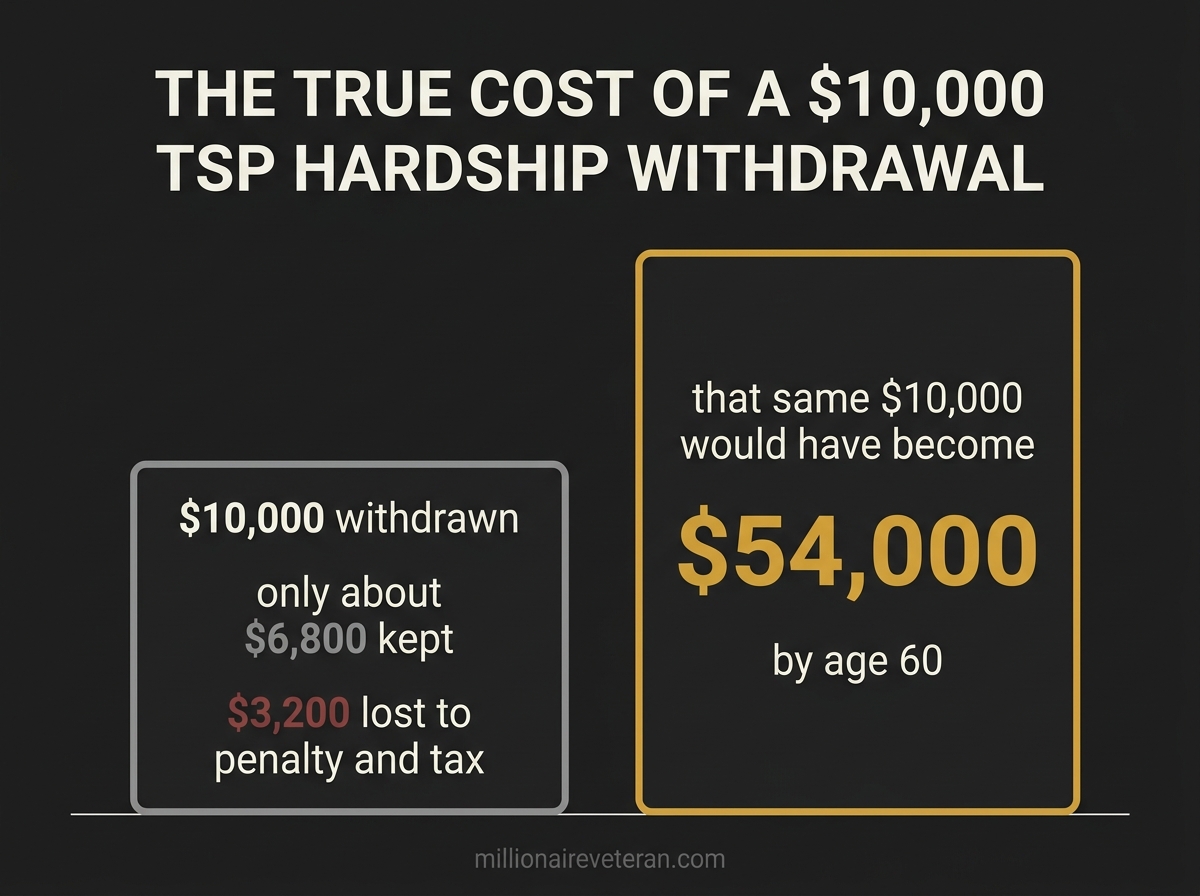

Say you take $10,000. You are 35, you land in the 22% bracket, and no penalty exception applies. The 10% penalty takes $1,000. Federal income tax at 22% takes roughly $2,200 more. You asked for $10,000, and about $6,800 actually reaches your hands.

That $3,200 in penalty and tax is the cost everyone sees. It is not the cost that counts.

The $10,000 you removed had decades of compounding still in front of it. At a 7% average annual return over 25 years, that balance would have grown to roughly $54,000 by the time you turned 60. That is the real price tag. You did not spend $10,000. You spent about $54,000 of your future self’s money to put $6,800 in your pocket today.

A hardship withdrawal doesn’t cost you what you take out; it costs you what that money would have become.

Run your own version before you decide. Your bracket is yours, your timeline is yours, and 7% is an estimate, not a promise. The shape holds regardless: the amount you keep today is a sliver of what you give up down the line. Once you have seen that gap in your own numbers, the decision looks different than it does under pressure.

There is a second cost that hides behind the first. This example is one withdrawal. People who reach for the TSP once under pressure often reach for it again, because the situation that created the first shortfall is still running. Two or three hardship withdrawals across a career, each one a “small” amount at the time, can quietly reset a retirement by six figures. The habit does more damage than any single withdrawal, and it is easier to start than to stop.

What to Try First

Because that gap runs so wide, the smart order is to exhaust the moves that leave your compounding alone before you reach for the one that ends it.

A TSP loan is the closest alternative and the one most worth understanding. You borrow from your own balance and repay it to yourself with interest. No tax event. No penalty. Once you finish repaying, the money is back in your account with its place in the market restored. The trade-offs are real. You owe the payments, and if you separate from service with a balance still outstanding, the loan can come due quickly. But a loan repaid is a fundamentally different event from a withdrawal taken, because the balance lives to keep growing. A withdrawal never gets that chance.

A funded emergency fund makes the whole question disappear. Cash set aside for exactly this kind of expense means you never have to choose between today’s crisis and tomorrow’s retirement. If you have never built one on purpose, a sinking fund is the mechanism: money parked ahead of the need, so the need never reaches your TSP. Slower to build than a withdrawal is to take, and the only one of these that leaves your retirement completely alone.

Before any of that, look hard at the cash flow itself. Recurring negative cash flow is the first hardship category for a reason, and pulling from retirement to cover it treats the symptom while the cause keeps running underneath. If more is going out than coming in on a repeating basis, a withdrawal buys you a month or two and leaves the machine that created the shortfall fully intact. Fixing what comes in and where it goes solves the problem the withdrawal only postpones.

If a withdrawal does turn out to be the only path left, the amount is still a decision. Take the smallest number that actually solves the problem, not a round figure with padding for comfort. Every extra thousand you leave in the account keeps compounding for you instead of for no one, and the difference between covering the real shortfall and taking a little extra “just in case” can be tens of thousands of dollars by the time you retire.

Sometimes none of these reach far enough, and the hardship is here right now. When that is true, you take the withdrawal knowing the full cost instead of blind to it. That is a decision made with open eyes, and with your retirement on the table, open eyes are the only way to make it.

Same Rules, Different Cost

Everything above applies identically to every TSP participant. The five categories, the $1,000 floor, the penalty, the tax treatment: the same for everyone who logs in. What changes from person to person is the structure each of you carries into the decision.

Whether a TSP hardship withdrawal is your worst option or your least-bad one depends on things you set up long before the hardship showed up. Whether you built an emergency fund. How your balance splits between Roth and traditional. How close you are to 59½. Whether a loan is the cleaner fit for your situation. Those variables sit upstream of the rules. For the structural side, Roth TSP vs Traditional TSP shows how the account’s design shapes what a withdrawal costs you, and the full withdrawal rules lay every other option out beside this one.

You cannot change the rules, but the structure you bring to them is yours to build, and the time to build it is before a hard month forces the question.

Plan Around Your Real Numbers

The Firewatch Blueprint walks through the structural framework that shows where a hardship withdrawal fits against the rest of your TSP: your contribution stack, your Roth and traditional split, your timeline to 59½, and whether an emergency fund stands between a bad month and your retirement balance. Not a withdrawal recommendation. It is the work to do before the decision is in front of you, not during it. Free. Delivered to your inbox.

About the Author

Joshua Breaux

Retired U.S. Marine

Financial Management Analyst

BS & MBA in Analytics

His family runs on the same systems he teaches here.

This content is educational and does not constitute personalized financial advice. Millionaire Veteran is not affiliated with the Thrift Savings Plan, FRTIB, or the U.S. Government. Past performance does not guarantee future results.