The previous article showed why the three domains need to work together. Cash flow management creates margin. Income growth adds fuel. Investing compounds both. The sequence matters because each domain depends on the one before it.

That raises the obvious question: what do you actually do first?

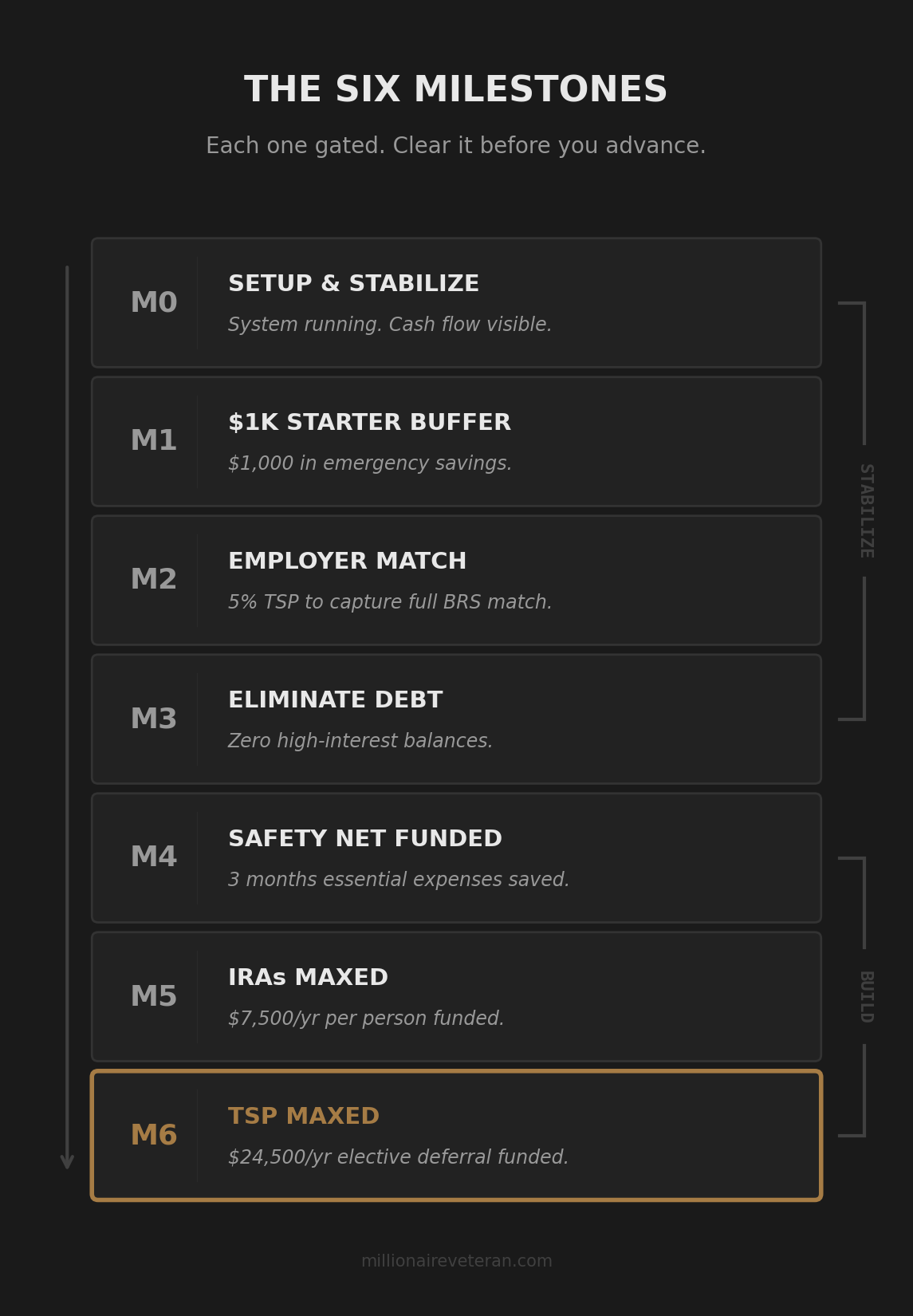

Most financial plans fail here. They give you principles without a sequence. “Save more, spend less, invest early.” True statements. Useless without an order of operations. A roadmap with six milestones solves that. Each milestone has a specific gate condition. You either meet it or you do not. There is no judgment call about whether you are ready for the next step. The gate tells you.

Why Milestones, Not Goals

A goal says “save more money.” A milestone says “$1,000 in a dedicated emergency account, and no money flows to debt payoff until that is satisfied.”

Goals are directional. Milestones are gated. The difference matters because gated milestones remove the decision fatigue that causes most financial plans to collapse. You do not wake up every morning and decide what to prioritize. The roadmap already decided. Your job is to clear the current gate.

Each milestone builds on the one before it. The sequence is not arbitrary. It follows a logic: stabilize the household, protect against emergencies, stop the bleeding from inefficient debt, build the safety net, then fund retirement accounts in order of tax advantage. Skip a milestone and the one after it becomes fragile. An emergency fund built on top of unresolved high-interest debt gets raided the first time cash flow tightens.

M0: Setup and Stabilize

The first milestone is behavioral, not financial. There is no dollar target. The gate is: your cash flow system is operational, your spending is visible, and your household is aligned on where money goes.

M0 has three gate conditions. First, complete the Diagnostic Review, which maps your actual income, debts, and recurring charges into a clear picture. Second, get the cash flow system running: accounts open, money distributing by purpose on payday, autopays routed correctly, credit card spending stopped. Third, run it for at least two pay cycles until allocations reflect reality, not optimistic estimates, and cash flow is moving in the right direction.

Every dollar of income deposits into one account, then gets distributed by purpose to dedicated accounts on payday. The system runs manually. You see exactly what is available for essentials, what is available for lifestyle spending, and what is flowing toward your next milestone.

A high-income household that funds $3,000 into savings on day one but still swipes credit cards and has no visibility into where money goes has not cleared M0. A tight-income household with $200 flowing to the next milestone after three clean pay cycles has. The system running cleanly is what clears M0, not a specific balance.

The full M0 implementation, including the Diagnostic Review workbook and the step-by-step setup process, lives inside the free community.

M1: $1,000 Starter Buffer

The first financial milestone. One thousand dollars in a separate savings account dedicated to emergencies.

The only job of this money is to keep the next surprise off a credit card. A set of tires. An urgent vet visit. A flight home for a family emergency. These things happen. Without a buffer, they restart the debt cycle. With a buffer, they are absorbed without creating new interest-bearing balances.

All milestone funding goes here until M1 is satisfied. No money flows to debt payoff, no money flows to planned spending accounts. The buffer comes first because everything after it depends on not creating new debt while you are eliminating old debt.

One thousand dollars is small enough to build in weeks on most military incomes. It is large enough to cover the most common emergencies that would otherwise go on a credit card.

M2: Capture the Employer Match

TSP contribution at 5% of base pay to capture the full BRS matching contribution. This is a payroll change, not a transfer from your cash flow system.

The BRS match provides an immediate positive return before the market does anything. For every dollar you contribute up to 5%, the government adds a dollar. There is no investment in existence that offers a guaranteed 100% return on day one. If you are not capturing this, you are leaving compensation on the table.

M2 often clears out of sequence. Many service members are already contributing 5% or more when they start the roadmap. If yours is already captured, confirm it and move on. The rule is simple: never reduce below the match, regardless of what other milestones require attention.

Why does M2 come before debt payoff? Because the match return exceeds the interest rate on any consumer debt. Even 22% credit card interest loses to a 100% match on 5% of base pay. That is why the sequence puts matching before debt elimination, even when the credit card balance feels urgent.

M3: Eliminate Inefficient Debt

This is the longest milestone for most families. Months to years depending on balances and income.

Not all debt is targeted here. Mortgages, vehicle loans with reasonable rates, federal student loans on income-driven repayment plans. Those are efficient debt. They have manageable interest rates and structured repayment. The debt targeted at M3 is the debt that is bleeding cash flow: high-interest credit cards, personal loans, predatory financing on electronics or furniture, the 18% used car loan from the lot outside the gate.

The system identifies which debts to attack using a ratio of balance to minimum payment. Debts that consume disproportionate cash flow relative to their balance get priority. The member chooses the payoff method: highest interest rate first (saves the most money) or smallest balance first (fastest behavioral win). Both work. The sequence within M3 is a personal decision.

Each debt eliminated frees its minimum payment to roll into the next target. The pace accelerates as debts clear. The first one feels slow. The third one falls faster than expected because the freed minimums are stacking. A household paying $150/month minimums across three credit cards that clears the first one now has $150 extra per month aimed at the second. When the second falls, $300 rolls into the third. The acceleration is real and visible in the account balances.

This is also the milestone where the credit card freeze from M0 pays off. No new balances forming while you attack the existing ones. The debt pile shrinks in one direction only. If new charges kept appearing, the attack list would be a treadmill instead of a countdown.

When M3 clears, the account that was funding debt payoff changes purpose. Same account, new mission. The member renames it. That rename is a milestone moment worth marking.

M4: Safety Net Funded

Real emergency fund. Three months of essential fixed expenses in a separate savings account. This is the full safety net, not the $1,000 starter buffer from M1.

After M3, the full debt payoff allocation plus all freed minimum payments become available to fund this. The pace is faster than most people expect because the monthly cash flow directed at this milestone is substantial once debt minimums are no longer consuming it.

M4 is not a goal. It is a gate. When the safety net is funded, the household has a meaningful buffer against job loss, medical events, or any disruption that temporarily reduces income. Credit cards are no longer the backup plan. The backup plan is funded and sitting in a dedicated account.

The specific target depends on the household. The default is three months of essential fixed expenses. Some families choose more based on their situation. The minimum is one month. Essential fixed expenses means the non-negotiable bills: rent, insurance, car payment, utilities. Not total monthly spending. A household spending $4,200 per month with $2,800 in essential fixed expenses has a default target of $8,400, not $12,600. That distinction makes M4 reachable faster than most people expect, especially with the freed debt minimums from M3 now flowing directly into this account.

M5: IRA(s) Maxed

Personal retirement accounts at full annual contribution. $7,500 per person in 2026. For a married service member with a spouse, that is $15,000 per year across two IRAs. Spousal IRAs are available even if the spouse has no earned income.

Why IRAs before maxing TSP? Different tax treatment, different investment options, different withdrawal rules. IRAs provide flexibility that TSP does not, including a broader range of funds and different access rules in certain situations. The details belong in the Invest Smarter series. The milestone here is straightforward: are both IRAs being funded at the annual limit?

M6: TSP Maxed

Employer retirement plan at the annual elective deferral limit. $24,500 in 2026. This is a payroll contribution increase, same mechanism as M2 but at a higher level.

After M6, all standard tax-advantaged retirement containers are at full capacity. TSP at $24,500. IRAs at $15,000 combined. Total: $39,500 per year in tax-advantaged space, plus the BRS match on top. This is the contribution target from the first article in this series fully realized.

The system shifts from building to maintaining. Allocations stabilize. The cash flow system continues running. The monthly review continues. But the primary question changes from “how do I fund the next milestone?” to “how do I sustain what I have built and what do I do with the margin that is now available?” That margin, the cash flow that was previously consumed by debt payments and milestone funding, becomes room. Additional investing beyond tax-advantaged accounts, planned spending that was deferred, or simply a wider lifestyle allocation that reflects the life you built the system to protect.

The Three Rules

These run alongside every milestone, not after them.

Earn More does not wait. The Diagnostic Review at M0 reveals the gap between current income and full contribution capacity. If that gap is wider than what cutting can close, building a transferable skill starts immediately. Not a business launch. Learning. The gap signal at M0 is the trigger. The Earn More series covers where the ceiling sits and what the options look like.

Protect the life you are building. The cash flow system always includes lifestyle spending. Dining out, travel, making memories with the people you care about. If funding the next milestone requires eliminating everything that makes life worth living, that is not discipline. That is a signal to earn more. The system is designed to be sustained over years, not endured for weeks.

When life changes, find your new position. Deployment. Promotion. New child. Disability rating. Major income change. Any of these changes your numbers. Re-run the Diagnostic Review. Recalculate allocations. The roadmap is designed to be re-entered, not restarted. You reposition. You do not go back to zero.

The Household Conversation

The system works when both people in the household understand how money moves. If one person runs the Payday Ritual and the other swipes a card without checking the Lifestyle balance, the accounts stop telling the truth. The system does not require both people to be financial experts. It requires both people to know which account to spend from and what happens when one of them reaches zero.

That conversation is part of M0. Not a lecture. Not a negotiation. A shared understanding of the structure and why it exists. The free community includes resources for how to have that conversation in a way that does not start a fight.

What Comes Next

You have the full picture. The compounding engine. Your position on the spectrum. The three domains and why they work together. And now the six milestones that sequence the whole thing into a concrete plan.

The next step is M0. Every milestone after it depends on having the cash flow system running and the real numbers visible. That is where the community picks up.

Start M0 With Your Real Numbers

The Diagnostic Review inside the free Millionaire Veteran community takes your actual income, debts, and spending and maps them to this roadmap. It shows you which milestone you are at, what gate you need to clear next, and what your specific allocations should look like.

The blog taught the system. The community puts you in it.

About the Author

Joshua Breaux

Retired U.S. Marine

Financial Management Analyst

BS & MBA in Analytics

His family runs on the same systems he teaches here.

This content is educational and does not constitute personalized financial advice. Millionaire Veteran is not affiliated with the Thrift Savings Plan, FRTIB, or the U.S. Government. Past performance does not guarantee future results.