You already decided sinking funds are a good idea. You sat down to build them, opened a budgeting app or a fresh spreadsheet, and the first question it asked was how many categories you wanted and where the money should actually go. That is the moment most people stall, because knowing that a fund helps is different from knowing how to set one up so it survives past the first busy month.

This walks through how to set up sinking funds step by step, with the real math, and then names the one setup choice that quietly breaks the whole thing later. If you are still deciding what a sinking fund even is, start with what a sinking fund is and come back. This article assumes you are past that and ready to build.

The steps themselves are simple. The mistake is not in the steps. It is in how many funds you try to run and where you keep the money.

How to Set Up Sinking Funds: The Five Steps

Here is the whole setup, in order. You can run it today with whatever accounts you already have.

Step one: list the known, irregular costs. Look at a full year and write down the costs that are coming but are not monthly bills. Annual vehicle registration. Insurance you pay every six or twelve months. Holiday spending. Replacing worn boots and gear before they fail. The reenlistment-leave road trip you already know you are taking. The professional license or association fee that renews once a year. You are not trying to catch every possible cost on day one. Start with the handful that have blindsided you before.

Step two: size each one. Take the cost and divide it by the number of months until it is due. That number is your per-month set-aside. A cost of $600 due once a year is $50 a month. A cost due in six months is funded twice as fast as the same cost due in twelve. The arithmetic is the same every time: cost, divided by the months of runway, equals the slice.

Step three: decide where the money lives. This is the step the app rushes you past, and it is the one that decides whether your funds hold. You have two options. Label a category inside your one checking account, or move the money into a real account of its own. They feel the same on setup day. They are not the same three months in, and the rest of this article is about why.

Step four: route the set-aside on payday. Move each slice the day you are paid, before the money has a chance to become groceries or gas. Doing it once, on payday, by hand, is the point. The moment you get paid is the moment the money is easiest to direct, because nothing else has claimed it yet.

Step five: leave it alone. Once the slice is moved, stop watching it. There is no transaction-by-transaction reconciliation and no daily check-in; the monthly Azimuth Check still handles the calibration. When the cost arrives, the money is there and you pay it. The balance is the status. The work was steps one through four, and steps one and two only happen once. Everything after that is a single transfer on payday and then nothing until the bill lands.

That last part is what separates a system that holds from one you abandon. A setup that demands attention every day loses to a busy week every time, while one that asks for a single move on payday survives a field problem, a stretch of long workdays, or a week where you barely look at your phone. The less the system needs from you between paydays, the more likely it is still running six months from now.

That is the complete setup, and following it puts you ahead of most people who mean to build sinking funds and never finish. When those attempts collapse, the cause is almost never the steps; it is setting up too many funds the wrong way.

A Worked Setup (So the Math Is Concrete)

Numbers make this real, so here is one clean pass. Treat the amounts as illustration, not prescription. Your costs and your amounts are yours to pick.

Say you name three known costs. Vehicle registration at $300, due in twelve months. An insurance premium at $720, due in twelve months. Holiday spending you want to cap at $600, due in twelve months. Divide each by twelve. That is $25, $60, and $50 a month, or $135 total set aside every month for costs that used to arrive as a wall.

Now the wrinkle the tidy step lists skip. What if a cost is not twelve months out when you start? Say the registration is due in five months, not twelve. You do not have a full year to spread it across, so you divide by the runway you actually have. Three hundred dollars over five months is $60 a month until it is paid, then it resets to the steady $25 a month for the next full cycle. Starting mid-year costs a little more up front to catch up. After the first arrival, every fund settles into its steady rate.

The method never changes. Cost, divided by the months you have left, gives you the slice. A fund due soon costs more per month than the same fund due far off, which is exactly what you would want, because the near one needs to be ready sooner. Once you have run the division for each cost, the hard thinking is done.

One more thing worth deciding up front: what to do the first time a fund empties. When registration comes due and you pay it, that fund drops back toward zero, and then it starts filling again for next year at the steady rate. You do not close it and you do not start over. A sinking fund is built to drain to zero on purpose and refill for the next cycle. Knowing that ahead of time keeps you from panicking when a fund you spent months building suddenly reads low the day after you use it. A low balance the day after a planned cost is the fund doing exactly what you built it to do.

The Setup Mistake That Breaks Sinking Funds Later

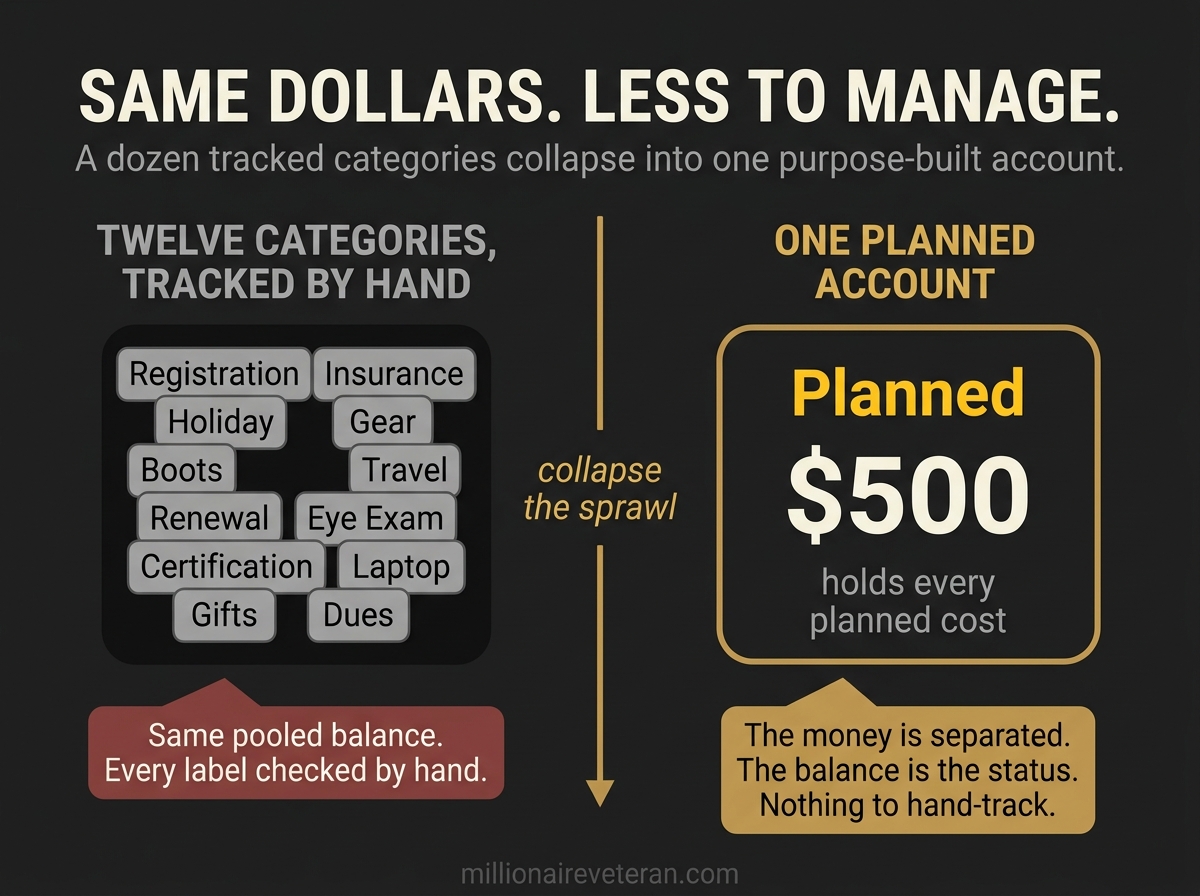

Here is where the standard advice sends you wrong. Most how-to guides tell you to make a category for each fund. So you do. Registration gets a category. Insurance gets a category. Holiday, gear, boots, travel, license renewal, the annual eye exam, a professional certification, the laptop you know will need replacing. Follow the advice honestly and you end up with ten, twelve, fifteen labeled categories, each one needing its own mental check every time you look at your money.

Two problems stack on top of each other, and together they are why sinking funds quietly fail.

The first is the maintenance load. A dozen hand-tracked categories is a dozen little accounting jobs you now own. Every time you spend, you are supposed to remember which category the money came from and update it. That is the same reconciliation chore that makes people abandon budgeting apps in the first place. Nobody quits sinking funds because the concept is wrong. They quit because keeping fifteen categories straight by hand is a part-time job they never signed up for.

The second problem is the one that hides underneath the labels. All fifteen of those categories are sitting in the same pooled balance. The money is labeled, but it is not separated. The account still shows one number, and that number includes the registration money, the holiday money, and the rent money all at once, which means the balance you see overstates what is actually free to spend. A tight week arrives, the account looks like it has room, and the labeled money gets used, because a label inside an app does not physically stop anything. That is the pooled-account problem the sinking-fund guide already covers, and it does not get better when you have fifteen labels instead of one. It gets worse.

Put both together and the lesson is blunt. Sinking funds do not fail because you have too few accounts; they fail because you are tracking too many by hand. The fix is not more discipline and it is not a better app. It is fewer places to track and real separation for the money that matters.

Collapse the Sprawl: A Few Purpose-Built Accounts

You do not need fifteen categories. You need a small number of purpose-built accounts where the money is actually separated, and you need one of them to hold all your planned, known-future costs together.

Move the sinking funds out of the labels and into a real account of their own. All of them, in one place. The registration slice, the insurance slice, the holiday slice, the gear slice, funded on the same payday, landing in the same dedicated account. You do not need a separate account for every fund. You need one account that holds the planned costs and is walled off from your day-to-day spending. Inside that account, the total grows every payday, and because it is a real account, the balance in your spending account finally tells the truth. Nothing to hand-track: no transaction-by-transaction reconciliation, just the monthly Azimuth Check handling the calibration. The bank holds the line instead of your memory.

This is separation by purpose at the bank level, and it is the principle behind what a cash flow system actually does. The Compass Method, the cash flow system taught across this site, builds the whole structure on it: money divided into a few purpose-built accounts so each balance answers one question honestly. Your sinking funds have a home inside that structure. It is called the Planned account, and it holds the known future spending that lands more than a month out, the vehicle costs, the travel, the gifts, the gear. One account, funded on a schedule, holding what used to be a dozen categories you were supposed to police by hand.

Order still matters when you fund it. The essentials that cannot wait get funded first, before anything discretionary. Once the must-pay obligations are covered, the planned set gets fed on its schedule, a slice at a time, so each fund is full when its cost lands. You are not choosing between rent and the registration money. You are covering rent, then feeding the Planned account so the registration is already handled when the month comes.

Notice what changed about the work. You still made the same setup decisions, listed the same costs, ran the same division. What you dropped was the daily accounting. The way you set up sinking funds decides everything downstream: a dozen labels give you a dozen jobs, one purpose-built account gives you a single balance to glance at. Same money, same plan, a fraction of the upkeep.

Your Next Step

You just did the hard part. Sizing the costs, picking the runway, walling the money off in one account that holds instead of fifteen labels that leak, that is the same account-level separation the whole system runs on, and you already proved you can execute it. Your planned costs now sit somewhere your spending cannot reach. The rest of your money does not.

Your essentials still share a balance with your discretionary spending. Your emergency buffer still sits close enough to raid on a tight week. Every one of those deserves the exact separation you just gave your registration money, and the method does not change. Same walls, same one-glance balances, applied to every dollar instead of only the ones you can see coming.

That is how a cash flow system beats a budget, and it is the same reasoning behind why budgets keep breaking when they lean on willpower instead of structure. You collapsed the sprawl once. Do it for the rest. Fix the cash flow first. Everything else gets easier.

Collapse the Sprawl Into One Account That Holds

The Compass Method setup inside the Millionaire Veteran free community walks you through the purpose-built account structure, including the Planned account where your sinking funds live, using your actual take-home pay and the actual costs you know are coming. The AI advisor inside the community calculates each per-payday set-aside from your real numbers, so every fund is full when its bill lands instead of guessed at. The community is free and there is nothing to buy.

About the Author

Joshua Breaux

Retired U.S. Marine

Financial Management Analyst

BS & MBA in Analytics

His family runs on the same systems he teaches here.

This content is educational and does not constitute personalized financial advice. Millionaire Veteran is not affiliated with the Thrift Savings Plan, FRTIB, or the U.S. Government. Past performance does not guarantee future results.